Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Down but not out: the ECB and the euro corporate bond market

How significant could the ECB's winding down of its euro corporate bond purchases be on the overall market?

The European Central Bank (ECB) has been a major investor in the euro credit market through the years of quantitative easing. At its peak in November 2022, it owned €345 billion corporate bonds, via its Corporate Sector Purchase Programme (CSPP).

But as such a major investor, and for such a long time, we’ve often wondered what might happen to demand in the euro credit market when the ECB eventually stopped buying euro corporate bonds? And, by extension, what might happen if the central bank began quantitative tightening and actively sold its bond holdings in the market?

Stepping back

From February 2023, the ECB pivoted from full reinvestment of principal repayments and coupons to only partial reinvestment, before winding purchases down to zero from July this year. As a result, the monthly change in the ECB’s CSPP holdings will now be in negative territory, thereby creating a steady, effective outflow from the largest euro corporate bond investor.

Standing in

In practice, euro credit liquidity and spreads have displayed little weakness in response to the ECB’s termination of reinvestments. We believe this has been due, in part, to the timing of increased net inflows into the asset class from around mid-May. Higher yields, following the ECB’s interest rate hiking cycle, have attracted investors to reallocate to euro credit and appear to be acting as a substitute source of demand for the market.

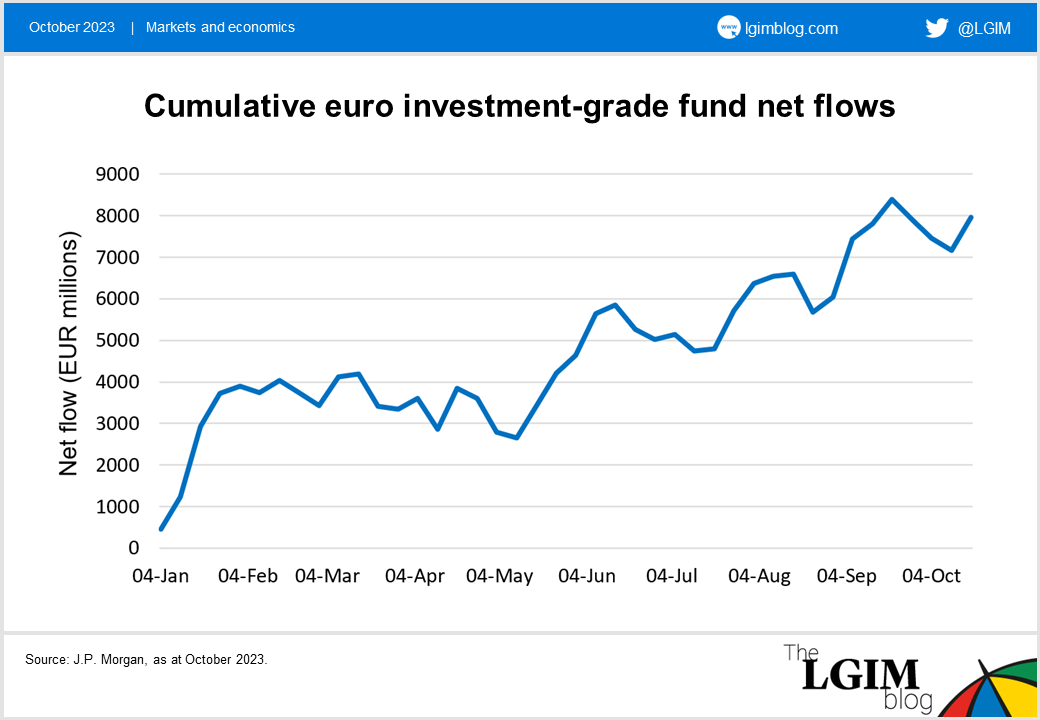

Total net inflows this year so far have amounted to around €8 billion, with almost €5 billion of that flowing in since mid-May (see chart below). Our concern now is around the sustainability of these net inflows and whether a slowdown (or even a reversal) of these would lead to the, so far, unrealised weakness of a market without the ECB as a buyer.

Standing down

For a while, euro corporate bond yields seemed to stabilise around the 4-4.5% range, with spread moves and underlying rates moves largely offsetting one another, although the current yield is slightly higher at around 4.6%[1]. Widespread weakness in the eurozone economy may drive credit spreads wider in our view, but not necessarily improve the attractiveness to new investors, particularly with the absence of the ECB to help dampen the move.

The CSPP holdings breakdown indicates that BBB rated non-financial issuers, particularly in France and Germany, have been the biggest beneficiaries of the programme and have, therefore, been trading tighter than they might otherwise have been. We believe that decompression in this market segment could play out over time, leading to an improvement in the attractiveness of spreads in these issuers.

Standstill

We don’t expect that the ECB will start actively selling its corporate bond holdings in the foreseeable future, despite the possibility. However, if it did, we believe the market effect of this negative demand could be exacerbated. At the same time, we don’t believe it’s likely that the ECB will radically change its course anytime soon and start buying bonds again to support a market sell-off, but policy surprises aren’t unheard of, so never say never…

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.