Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Solutions chart update: Long gilts

From Leith Hill to Box Hill - still hard going but smoother and less steep.

If you’ve ever ridden up Box Hill in Surrey (once voted the most popular hill climb in the world) then you’ll know that it’s not easy but the road is smooth and not too steep. Leith Hill, however, is the highest point in the Southeast of England, has regular changes in gradient, ends in an off-road section and is very steep. It is a difficult road to climb!

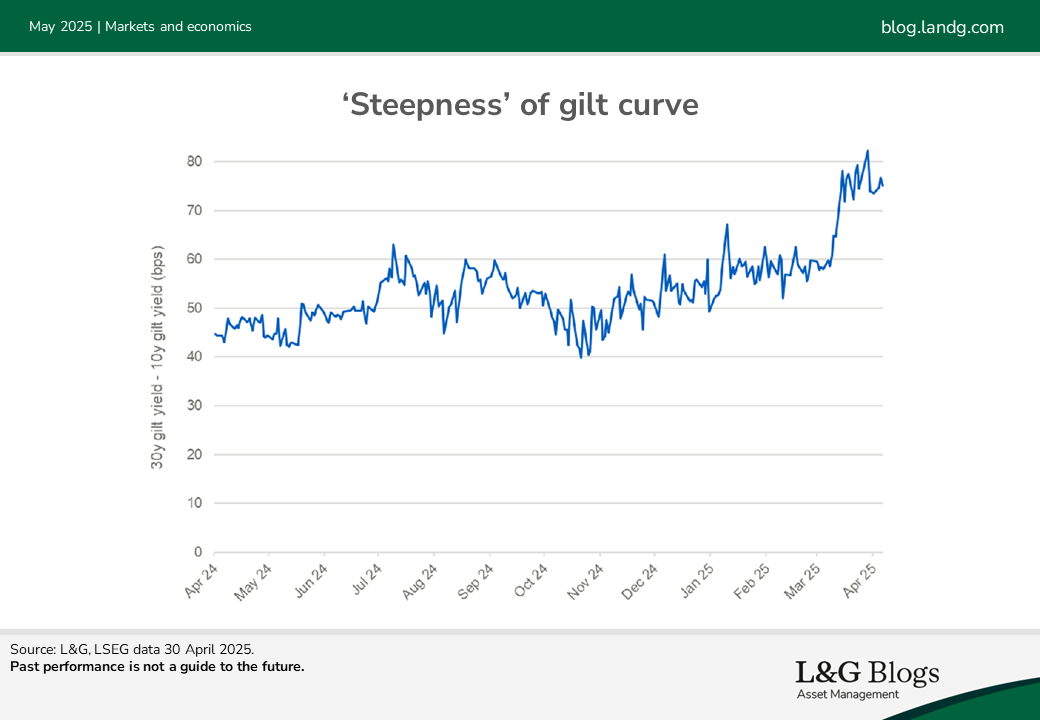

Speaking of steep ascents, the steepness of the gilt curve has been in flux recently. Long gilts had a tough April with 30-years gilts yields increasing by over 20bps versus 10-year gilt yields at one point and in relatively short order, as shown in our chart below.

This change in the shape of the yield curve is often known as ‘steepening’ (the curve is ‘steeper’ because the 30-year gilt yield is now relatively higher (still) than the 10-year gilt yield).

Gilts were not alone in these moves which came following President Trump’s Liberation Day. The steepening of curves was a global phenomenon. Indeed, other factors impacting the gilt market are to a varying extent common themes globally. Taking long gilts specifically, the general market narrative is that supply is higher and demand lower (from pension funds and central banks in particular) versus history. This can manifest itself in a steeper curve.

Investor feedback to the UK Debt Management Office (DMO) has noted this changing dynamic in the market for long gilts. The DMO has responded to this feedback, first in the 26 March Spring Statement, and then more surprisingly in the 23 April remit revision.

The April remit is typically a housekeeping exercise only with minor tweaks made once full fiscal year data is available to feed into the gilt remit. The major changes are reserved for March (in the absence of unexpected events). However, following the additional £5bn funding requirement announced in April (from £300bn to £305bn) the DMO took the opportunity to:

- Fund the increase in T-bills (not gilts)

- Reduce funding in long gilts[1] by £10bn

- Increase its unallocated portion (used to respond flexibly to market dynamics)

By reducing long gilt funding by c.£10bn, the result was a further reduction in the % long gilt weighting from 13% down to 10%. The March figure of 13% was already a lower target on previous years. In addition, during the April volatility the Bank of England took the opportunity to switch a long gilt sale to a short gilt sale instead (reflecting what was happening in markets).

This latest action by the DMO (and arguably the complementary action by the Bank of England) resulted in some unwind in the steepening of the curve from levels around 80bps back to c.75bps (as can be seen in the above chart). Importantly there is therefore a local ‘cap’ on the steepness of the curve and the market has certainly noted that the DMO and Bank of England look more willing to adapt to market moves in a timely fashion.

And so it is for the DMO as they attempt to navigate the ‘Box Hill’ gilt remit instead of a ‘Leith Hill’ one! It won’t be easy, but the recent changes suggest that for now they could be on a smoother and steadier road.

[1] Which the DMO defines as gilts with a maturity greater than 15 years

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.