Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Where next for European equities?

Fiscal developments have galvanised the region’s markets, but shareholder returns remain anything but certain.

The article below is an extract from our Q2 2025 Asset Allocation outlook.

The prospects for European equities appeared particularly poor after the election of Donald Trump.

His assertive policy platform encompassing tariffs, a distinctly more sceptical approach to US security commitments to NATO, and vocal support for the leading American tech firms all appeared to pose profound challenges for European equities.

That left the region very cheap, especially when compared with the US, and deeply unloved by global investors. It seemed the election marked a new and reinvigorated phase of American exceptionalism, with assertive policy supercharging the case to be overweight US equities, and little else.

There was no alternative

It should be said, though, that the persistent outperformance of US equities over the past 15 years was as much about a lack of compelling alternative narratives as it was about the particular merits of the US market.

For much of the past decade, Europe has seen a mix of austerity, populism and war in Ukraine sap investor appetite. China has seen an equally lost decade as it has struggled under the weight of a persistent deflation of its housing and construction sector after years of overbuilding.

Investors expected, and were positioned for, more of the same, with momentum trades dominating as investors found little reason to do anything other than what had worked in recent years.

A shock to the system

Perhaps we should all have been more mindful of President Trump’s self-professed status as a disruptor. In Europe’s case, it’s probably better to describe him as a defibrillator, shocking the region’s politicians into the kind of decisive actions which seem beyond them in more normal, less challenging times.

Central to this has been Germany’s decision to ease the rules surrounding its debt brake and to boost infrastructure spending, steps that together could lift spending by €1 trillion over the next 10 years, equivalent to c.23% of GDP.[1]

China, conscious of the challenge US tariffs could create for its export-driven growth model, has pursued increasingly assertive domestic stimulus policies aimed at reinvigorating consumption at home, rather than relying on it from abroad. These developments have seen alternative narratives for investors explode into life, and left the only thing exceptional about US equities being their extended valuations relative to the rest of the world.

Can Europe walk the walk?

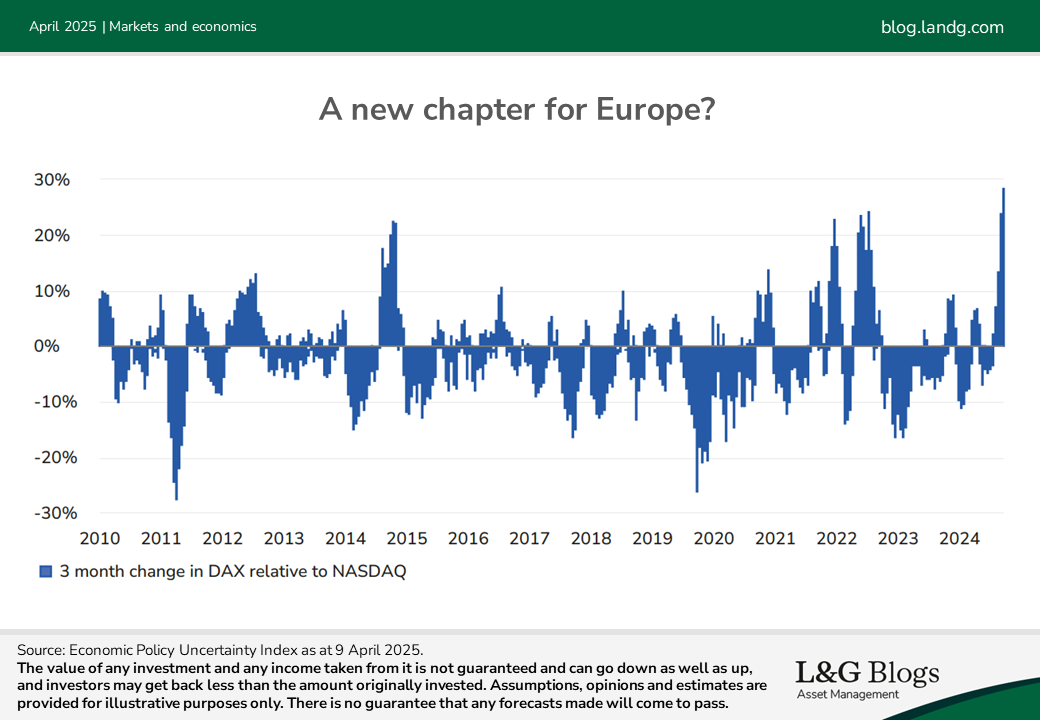

So, where are we now? This is an environment in which narratives, and investors, move fast. Since December, the DAX has outperformed the Nasdaq by around 20%, Germany’s valuation discount has closed by around 15 percentage points[2], and survey data[3] suggest one of the largest net overweights in European equities seen in the past decade.

Even more strikingly, Rheinmetall*, Germany’s leading defence firm, is now up over 2,700% over the past five years, making Nvidia*’s 1,900% gain over the same period appear quite pedestrian[4].

That puts European equities in a rare position where expectations are high, and ultimately earnings need to deliver.

Year to date, even as European equities have rallied 15%, 2025 earnings-per-share expectations have drifted lower.[5] What has underpinned the US equity market in the past 15 years has been extraordinary profit delivery. This has been helped, it should be said, by substantial buybacks and tax cuts.

Yes, Europe’s fiscal backdrop has changed markedly to one much more conducive of growth, but translating that into returns to shareholders will be far from straightforward.

The article above is an extract from our Q2 2025 Asset Allocation outlook.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

[1] Bloomberg as at 8 April 2025.

[2] ibid.

[3] Source: Bank of America’s Fund Manager Survey.

[4] Source: Bloomberg as at 20 March 2025.

[5] ibid.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.