Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

When will the dragon roar again?

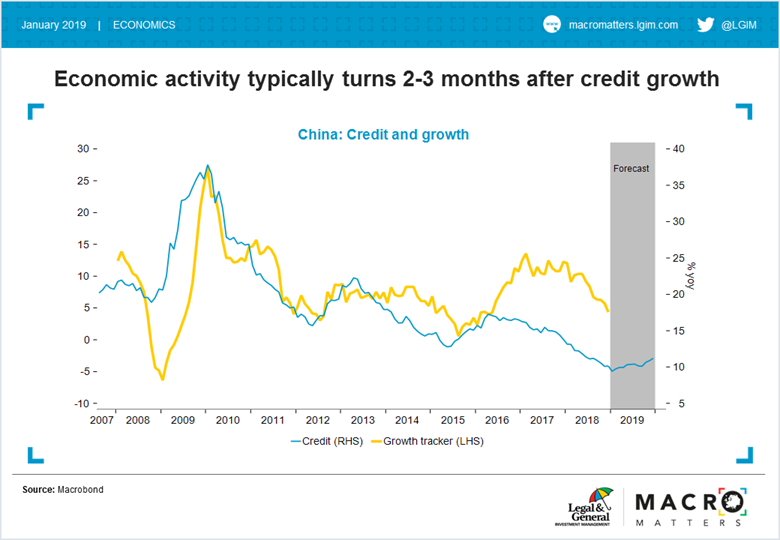

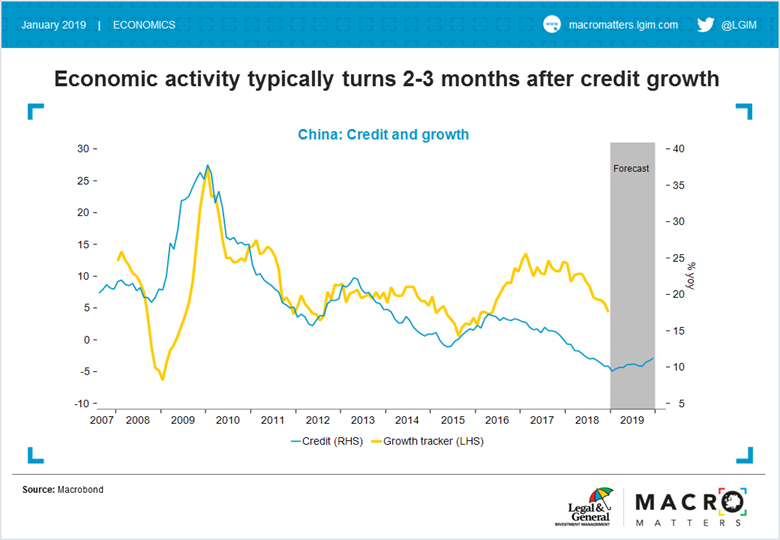

Considering if and when China’s economy will bottom out this year is one of the most pertinent questions for investors. Credit growth has historically been the best leading indicator for Chinese activity, so what is it saying this time around?

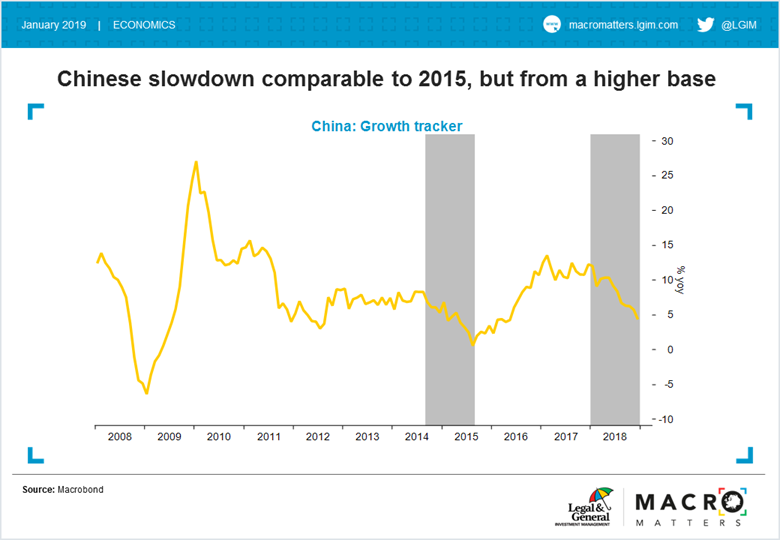

It's widely accepted that China's economy is slowing rapidly. Car sales are falling like a stone, manufacturing is contracting and industrial profits are down year-on-year, for the first time since the country's economic slump in 2015. Drawing on a wider set of unofficial data, our growth tracker implies a slowdown that is comparable to 2015, but coming from a higher base.

The government has responded with broad-based easing measures, including tax cuts, reserve ratio requirement cuts, and window guidance to induce more bank lending. The measures have been significant, but probably not as weighty as in 2015. Also, given the new focus on financial stability, the government has abstained from loosening shadow bank regulation — a mainstay of previous stimulus packages.

So will the economy bottom out in response to the stimulus? And if so, when? To try to answer these questions, we need to look at credit growth. Historically, turning points in credit growth have preceded turning points in economic activity by 2-3 months.

In forecasting the stock of credit we've made a few assumptions. We've assumed that banks extend the same amount of new loans as they did in 2018 and that corporates issue the same amount of bonds. In light of the easing measures, this is a rather conservative assumption. In addition, we've assumed that the stock of shadow credit remains constant as the government safeguards the deleveraging progress to date but doesn‘t push it further. We've also distributed the increased quota for local government bond issuance equally over 2019.

This scenario would lead to credit growth bottoming out now (in January). Over the course of 2019, credit growth would then accelerate by 1.8 percentage points compared to an acceleration of 4.5 percentage points in 2015. However, our assumptions are conservative, and the current downturn is shallower than the one in 2015. Given the usual time lags, we believe that Chinese economic activity should rebound in April or May, and with it global asset prices.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.