Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Top 7 things to know about equities when bond yields rise

Having worked as an equity strategist for well over a decade, I’ve lost count of the number of times I’ve had the debate on ‘what happens to equities when bond yields go up?’. And for most of that time bond yields were in the ice age and falling! To cut down on some future deja-vu, here's my Top 7 list of things to consider about equities when bond yields go up.

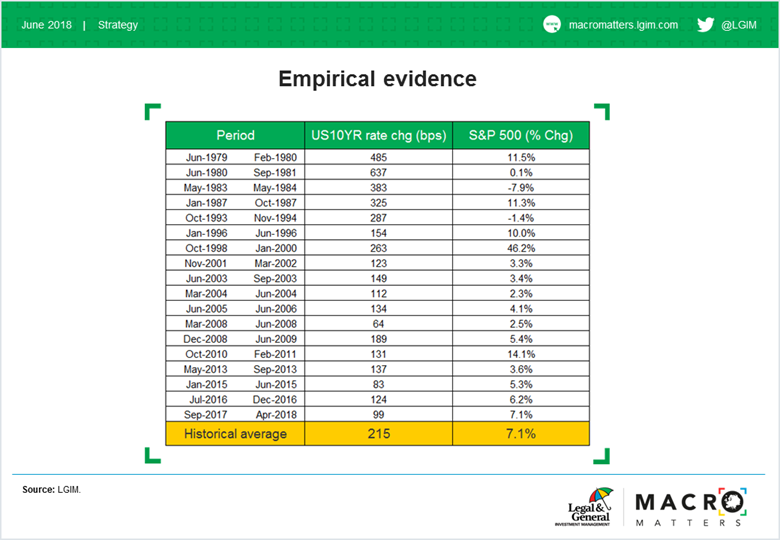

1. There is strong empirical evidence that equities can go up with rising yields

Looking back at the last four decades, we find 16 periods where Treasury yields went up sharply. In 14 of those episodes the S&P went up, on average, by more than 7%.

2. The driver of yield matters

More important than the direction of yields is why yields are moving. If yields are up because markets are pricing in stronger growth or declining deflation risk, then it’s normally good news for equities. If it’s hyperinflation worries, then it’s bad news.

3. The speed of yield adjustment matters

Equities usually cope well with a slow rise in yields, but sharp yield moves, in either direction, are typically more problematic. Yield spikes raise the risk of dislocation in bond markets spilling over into other markets or economy. As yields stabilise, equities typically recover.

4. The level of yields matters

Price-earnings (PE) ratios have generally been highest with 10-year Treasury yields at 5-7%.

Rising bond yields have become bad news for equities at 5-6%. However, there are some signs it could be earlier this time.

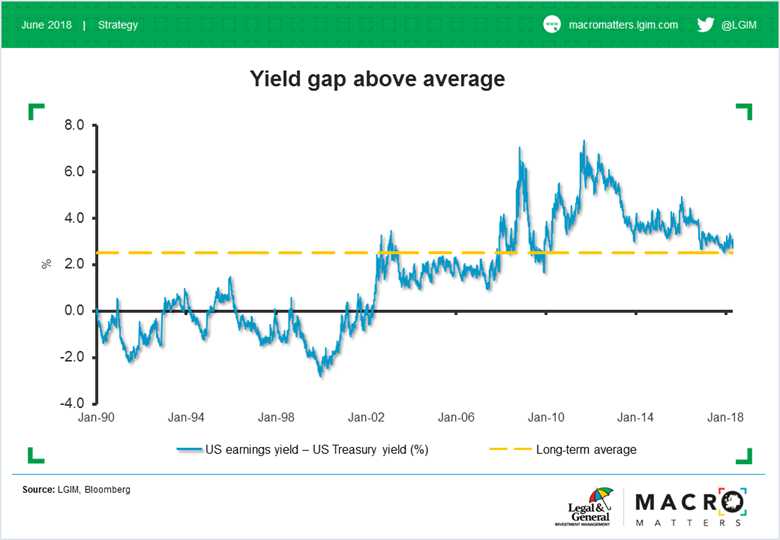

5. Equities have a valuation buffer against higher yields

Equities usually yield more than bonds. The yield gap is currently above average, as is the equity risk premium (ERP), which is the return premium that investors typically demand for holding equities over bonds. The yield gap and ERP have generally increased with falling bond yields. Both should, and have, contracted with rising yields. Treasury yields around 3.6% would take the yield gap back to its long-term average.

6. A small drag on earnings

Higher bond yields hit earnings via higher interest expenses and lower GDP growth. We estimate that a 0.5% rise in corporate bond yield takes ~2% off S&P 500 earning per share (EPS).

7. A small drag on buybacks

The incentive for buying back your own shares erodes with higher corporate bond yields. Buybacks stop being earnings accretive when bond yields rise above the earnings yield (currently ~5.8%). Buybacks have been a steady 1.5-2% boost to S&P EPS growth.

So can we condense all this even further into a conclusion? I would expect equities to continue going up with gradually rising bond yields, although the trade-off starts to get more complicated when Treasury yields reach the 3.5% to 4% range.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.