Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Bubbles are rare, especially just out of a recession

There is a lot of bubble talk at the moment. A fellow scholar of market bubbles, Jeremy Grantham, begins his new outlook: “The long, long bull market since 2009 has finally matured into a fully-fledged epic bubble.”

When Mr Grantham speaks we ought to listen, as he is a great student of the history of bubbles and has a good track record in predicting the moments when they burst.

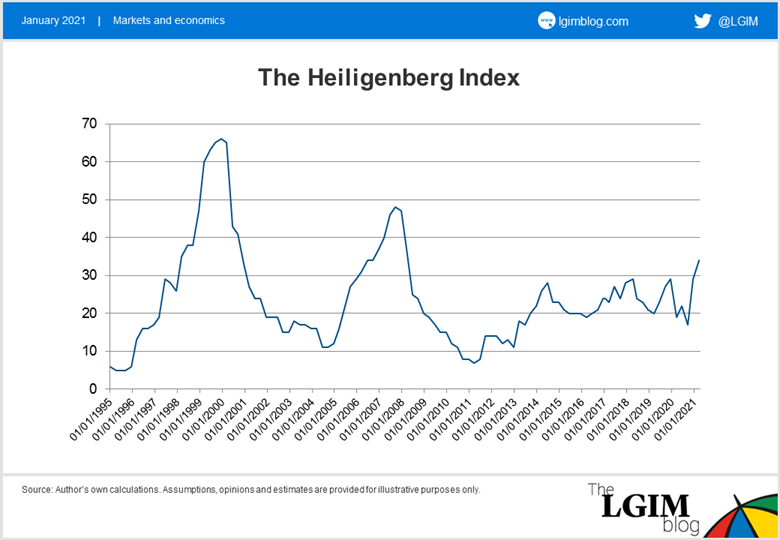

I think Jeremy may be right but, as he concedes, the market could run a lot further. The Heiligenberg Index is my own proprietary bubble gauge, based on indicators I have gathered over my 30-year career. The index is designed to give us an early warning when a bubble is occurring in equity markets.

My latest update, portrayed in the chart below, shows that the probability the market is forming a bubble has indeed been rising. In fact, it is now the highest it has been since 2008.

What has led the index higher? I would highlight a few recent trends.

First, we have seen an increase in capital raising through IPOs and SPACs. Quite a few of these IPOs and SPACs echo the tech bubble of the late 1990s, when newly listed stocks had unbelievable returns in their first days on the public market.

A second and related point is that the involvement of US retail investors is going through the roof! For instance, two of the largest trading days by share volume of all time in the US occurred in the past two weeks. According to Goldman Sachs, volumes executed on the broker-operated venues favoured by retail investors in December exceeded that of the NYSE for the first time on record.

For better or for burst?

There are clearly two sides to this debate: the market is definitely reminiscent of a bubble forming, but it could easily still get much stronger from here. So with all due respect to Mr Grantham, I think he is premature in calling a bubble right now.

We are just emerging from the COVID-driven economic recession. This means many macroeconomic indicators have improved, output gaps are wide and monetary policy is extremely accommodative.

Though this environment can be a good one for breeding bubbles, I believe it is too early to position portfolios for a burst. There is plenty of money on the sidelines invested in deposits and money-market funds, the consumer savings rate is high, there is spare capacity to be absorbed, and yet another fiscal package is on the horizon. So there is plenty of firepower left and no real catalyst to stop it.

What does this mean for markets? My own thoughts: small-caps should outperform large-caps (which is already happening); it is bullish for technology and other themes popular with retail investors; it is, all else equal, bullish for the US over Europe as this retail effect is mainly visible in America; and equity volatility should remain elevated as there is a structural retail bid for call options.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.