Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

When vacancies vanish: UK and French unemployment at a turning point?

If economic growth remains weak, we expect unemployment in these countries to rise more than in their peers.

A combination of negative supply shocks – to labour, following the pandemic, and to energy, following the Russia-Ukraine war – and aggressive fiscal stimulus has caused demand to outstrip supply in recent years, pushing up inflation.

Things are now cooling, but from extreme temperatures. The excess of US vacancies to unemployment was similar to that during previous wars according to a recent ‘Jackson Hole’ academic paper.

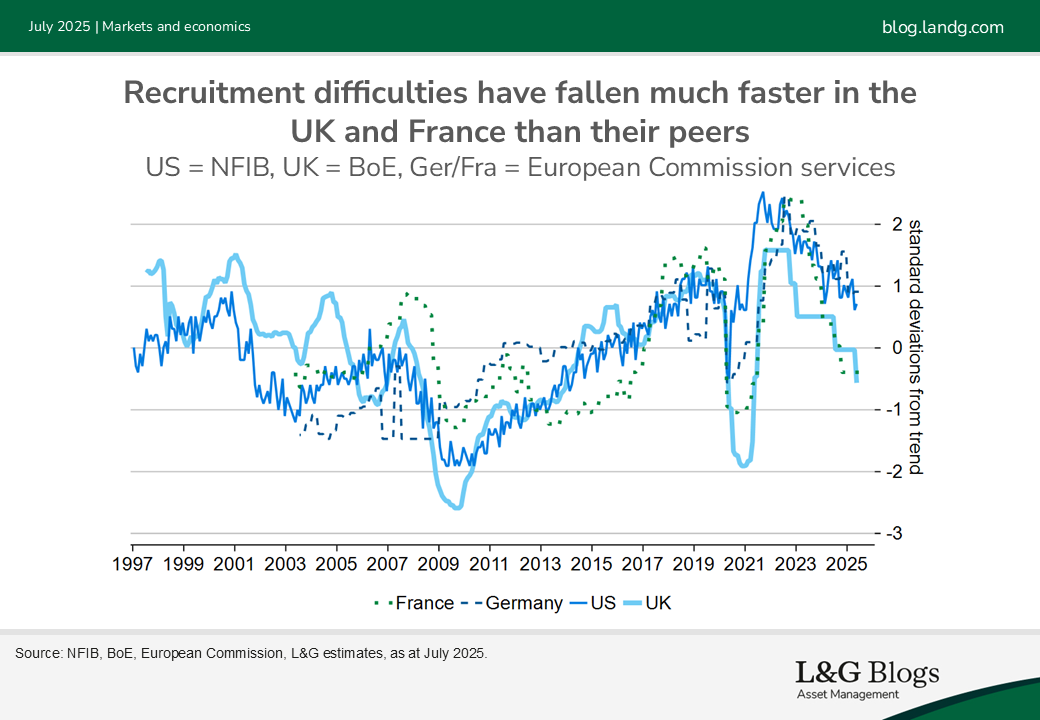

But there are important cross-country differences. Recruitment difficulties and vacancies still seem historically high in the US and Germany, but are noticeably weaker in the UK and France.

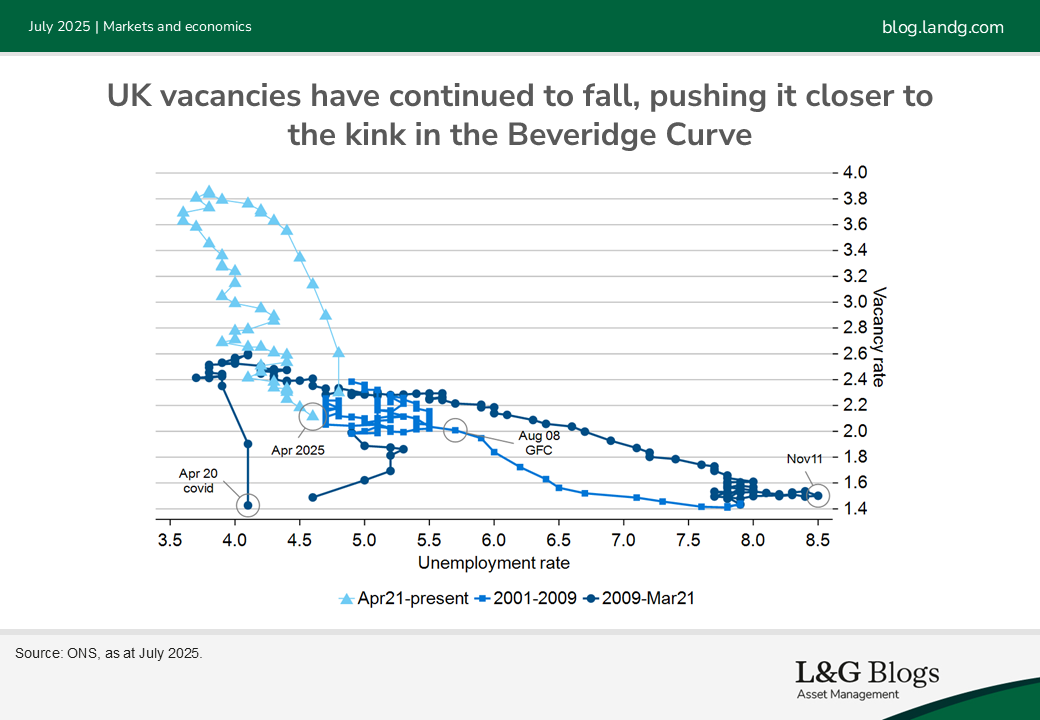

Why does this matter? Because of the so-called “Kinked Beveridge curve”, which plots unemployment on the X-axis vs unfilled job vacancies on the Y-axis. This suggests that at extreme levels of demand, it becomes difficult to reduce unemployment any further and instead vacancies surge (the Beveridge curve steepens).

At this point, inflation should rise and monetary policy be tightened. Eventually, the economy should cool and those excess vacancies disappear. But there should then come a point when labour demand is so weak that instead of just cutting vacancies, firms shed existing roles. Unemployment would then rise, making the Beveridge curve flatter.

We can debate how comparable today’s vacancy and recruitment difficulty data are to the past. The BoE has argued that the cost of advertising has fallen, so the equilibrium number of vacancies should be higher than before (making today’s weakness even more dangerous). But there’s also uncertainty as to the size of the labour force, given low sample response rates. We can all agree that weaker momentum in the UK and French economies puts those countries closer to the inflection point than their peers.

So if growth remains weak, due to fiscal tightening and global trade-war uncertainty, unemployment is more likely to rise in the UK and France given their weaker starting points. We tested this hypothesis in a panel of 11 euro-area economies post energy crisis. We found evidence that for a given rate of economic growth, unemployment was more likely to rise in countries that had normal versus extreme recruitment difficulties a year earlier.

The implications for interest rates could differ. Rising unemployment should push down UK yields, in our view, but cause French spreads versus German bunds to widen. The Bank of England softened its language in the latest minutes following five consecutive months of falling PAYE employment. However, rising unemployment and weak growth make it harder for France to meet its budget goals, risking new parliamentary elections in the autumn.

Our portfolios don’t currently have an underweight on OATS, French government debt, or an overweight on gilts, their UK counterpart. But we continue to look for investment opportunities as political risk develops and market positioning shifts.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.