Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Can bicycle lessons offer investment clues?

In his recent post, James concludes that central bankers, like his bicycle lessons for his son Michael, appear to have stabilised the cycle. If this is right, what could it mean for markets?

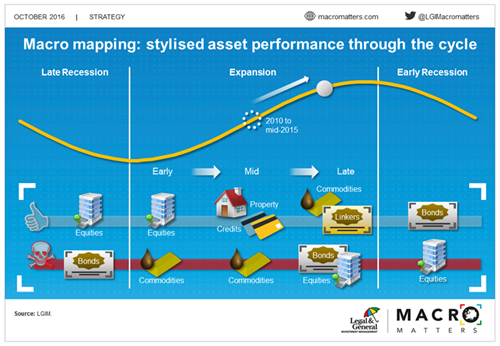

As mentioned in Stabilising the Cycle, getting the economic cycle right is the key call for asset allocators. So how do we aim to do that? In a nutshell, we divide the cycle into phases, based on what we call our ‘Macro Mapping’.

This proprietary research maps asset class risks and potential returns in different parts of the economic cycle. For instance, the research shows that equity returns have historically been sensitive to growth, but relatively insensitive to inflation.

We have been firmly mid-cycle from 2010 until mid-2015. With economic growth not too hot and not too cold, it’s been what most investors call a ‘Goldilocks scenario’, with the chances of a recession-induced bear market generally low.

Late-cycle economies, meanwhile, can be characterised by tight capacity, unbalanced growth, excessive credit expansion, tight monetary policy and worrying inflation pressures. So far we see none of that. This has been a good environment to take equity risk. And the fact that the cycle is somehow stabilising is – all else equal – good news, as it prolongs the length of the cycle.

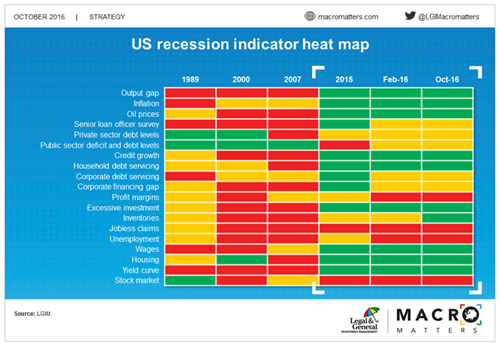

Our Head of Economics, Tim Drayson, recently updated our recession scorecard and it shows a stable picture, with only limited warning signs. The most worrying signs of overheating are in the labour market and corporate profit margins. However, to paraphrase Yellen in her recent press conference, "the economy has room to run", especially in housing, investments, inventories and inflation.

Yet despite the stabilising cycle and the limited warning signs, we remain somewhat cautious on equities for four principal reasons:

- We are gradually approaching late cycle dynamics

- The earnings upside for equities appears limited

- Systemic risk is elevated

- The prospect of rate hikes is hanging over markets

The rise in yields has been particularly notable recently. Higher nominal yields have been accompanied by an uptick in inflation expectations, which have kept real yields reasonably stable. This is probably the best form of yield pick-up for equity markets, yet so far equity markets have gone sideways. A rise in real yields, when nominal yields rise faster than inflation expectations, might be more difficult for market to swallow.

So it turns out Michael’s bike lessons can teach us a lot about markets. They show us that cycles can either move forward or crash to the ground. When it comes to asset allocation, it’s important to maintain the right balance between the two, and trust someone with experience.

For Michael, at least, with decades of cycle experience, that someone is James.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.