Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

US tariffs: what happens next?

In a dramatic reversal of policy, President Trump has paused reciprocal tariffs. But uncertainty and the effective tariff rate remain high and the US is still likely heading for recession.

The article below is an extract from our Q2 2025 Asset Allocation outlook.

President Trump’s 2 April Liberation Day shocked economists and markets by delivering large universal tariffs based on trade deficits rather than a more gradual and targeted approach to address US perceptions of unfair trade practices.

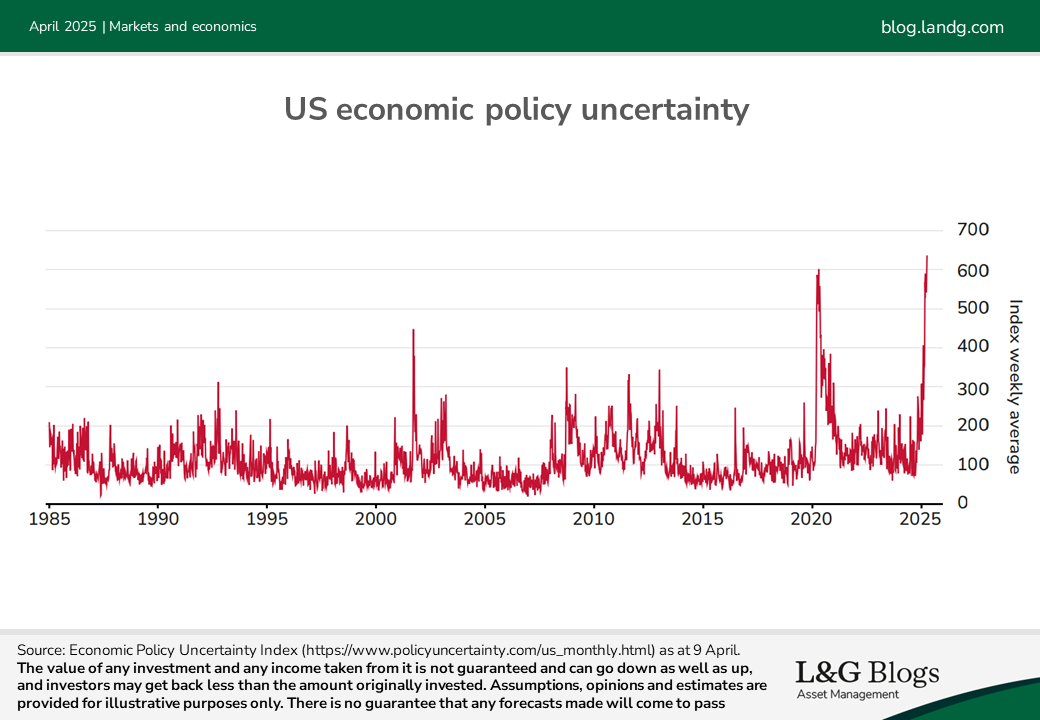

Economists responded with significant cuts to their forecasts, with many forecasting recession. A combination of factors, including market pressures, persuaded President Trump to pause the reciprocal tariffs for 90 days one week later. But 10% universal tariffs were still kept in place, and tariffs on China rose to at least 145%. The other tariffs introduced so far this remain. Policy reversal has probably reduced some of the risks of a more serious crisis, but betting markets are still suggesting a greater than 50% chance of a US recession this year.[1]

The huge tariffs on China mean these changes do not reduce the overall tariff rate based on current trade flows, though we expect a collapse in imports into the US from China if not quickly scaled back. This will reduce the effective tariff rate, but still leave it higher than most were expecting before Liberation Day. Furthermore, by entering into negotiations for 90 days, uncertainty is likely to remain high. It remains to be seen how quickly deals can be struck, but 10% tariffs now appear to be the floor.

Negative feedback loops

While the gap between our long-held view and consensus is in the process of closing, we still worry about the fat tail of a deeper recession. This is a negative supply shock, alongside a policy of maximum trade uncertainty as every traded product and country is in scope and there is little visibility on where the tariffs will settle. The downside risk is further tariffs emerge in the weeks ahead, leading to retaliation and trade war escalation, amplified by negative feedback loops from persistent uncertainty, wealth effects and a tightening in financial conditions.

We expect this to have a chilling impact on US GDP. Business investment related to trade and new supply chains is likely to be placed on hold. Recent confidence surveys have begun to falter, and we expect a further deterioration.

But to the extent this is still perceived as a negotiating tactic, the most adverse economic effects won’t be seen until after the tariffs have been in place for a while. So the deterioration in the economic data might not be fully apparent until the summer. The extent to which this reduces the US goods trade deficit is unclear. If the US goes into recession (the opposite intention of the policy) that would reduce imports and the trade deficit.

A more benign path

President Trump has shown some sensitivity to a deteriorating stock and bond market, and likely will be paying attention to polling numbers. At some point, this could trigger a combination of removing the Mexico and Canada tariffs, better engagement with the rest of the world and a lower level of tariffs. This sets up the prospect for more balanced bilateral negotiations (including a quick renegotiation of the United States-Mexico-Canada Agreement). The Fed is in a tight spot from political pressure and tariff-induced inflation, which could push the core PCE deflator above 4% later this year, but rate cuts provide a backstop against a sharp rise in unemployment.. Congress is still debating fiscal policy.

Signs of economic weakness and tariff revenues could encourage tax cuts beyond merely extending those due to expire. But ultimately any relief is likely to be modest. An effective tariff rate of-15-20% seems likely to persist all year. This is because reducing the trade deficit in an attempt to boost US manufacturing appears to be one of the key strategic objectives.

In the near term, retaliation could come not only from governments, but directly from consumers via a broader boycotting of US products and brands. We have seen a strong anti-America reaction in Canada and signs that tourism to the US is falling sharply. In any case, some damage is already done and uncertainty over tariffs and their impact is likely to remain high.

The article above is an extract from our Q2 2025 Asset Allocation outlook.

[1] Polymarket as at 8 April 2025.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.