Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

US stimulus negotiations: time to deliver?

Recent news on COVID-19 vaccines has generally been positive, fostering the very broad positive sentiment towards risk assets, but we shouldn’t forget that the immediate economic outlook remains challenging.

Europe is already in a renewed contraction, following a significant increase in lockdown measures to bring the virus under control. US economic data have held up well so far because restrictions had been relatively limited, but stricter policies are starting to be deployed from New York to California amid still rising COVID-19 cases following the Thanksgiving holiday.

These deteriorating virus dynamics are coinciding with a crucial period in the negotiations over fiscal stimulus in the US. Treasury secretary Steven Mnuchin has stepped in with a fresh proposal which now has the support of Senate Republican leader Mitch McConnell. This brings both sides into alignment on the size of the package at around $900 billion, with only the details still to be finalised.

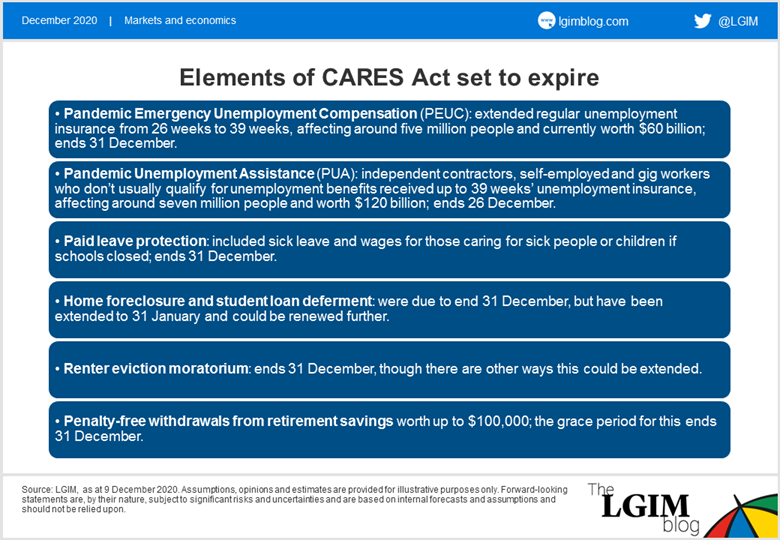

Amid the ongoing toll from the virus, both sides are coming under greater pressure to pass a bill. The fiscal headwinds to the US economy are set to intensify as more elements of the Coronavirus Aid, Relief, and Economic Security (CARES) Act are scheduled to expire in the coming weeks (see detail in the slide below). The disappointing November payrolls report added to the anxiety.

Despite this urgency, it is not certain a compromise can be reached in time for Christmas. Failure to reach an agreement risks an outright contraction in activity over the festive period, a negative GDP print for the first quarter of 2021, and so a double-dip recession.

Our outlook for 2021 is still positive, and markets might well look through any economic weakness as temporary, but given the gap between exuberant sentiment and the potential for short-term disappointment, we are tactically neutral at the moment. We will not chase the rally at this point, preferring to take our risk in relative-value trades.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.