Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

President Trump’s first couple of weeks: economic implications

The White House’s policy agenda has been in overdrive since inauguration. Consensus expects the agenda to support US growth. We see significant downside risks to this view.

Second time round, President Trump has appeared more prepared for office and has been busy signing a broad range of Executive Orders. Below, in part one of our two-part blog series on the potential implications of President Trump’s policy agenda, we look at developments across his four main policy levers: tariffs, fiscal policy, immigration and deregulation.

Tariffs

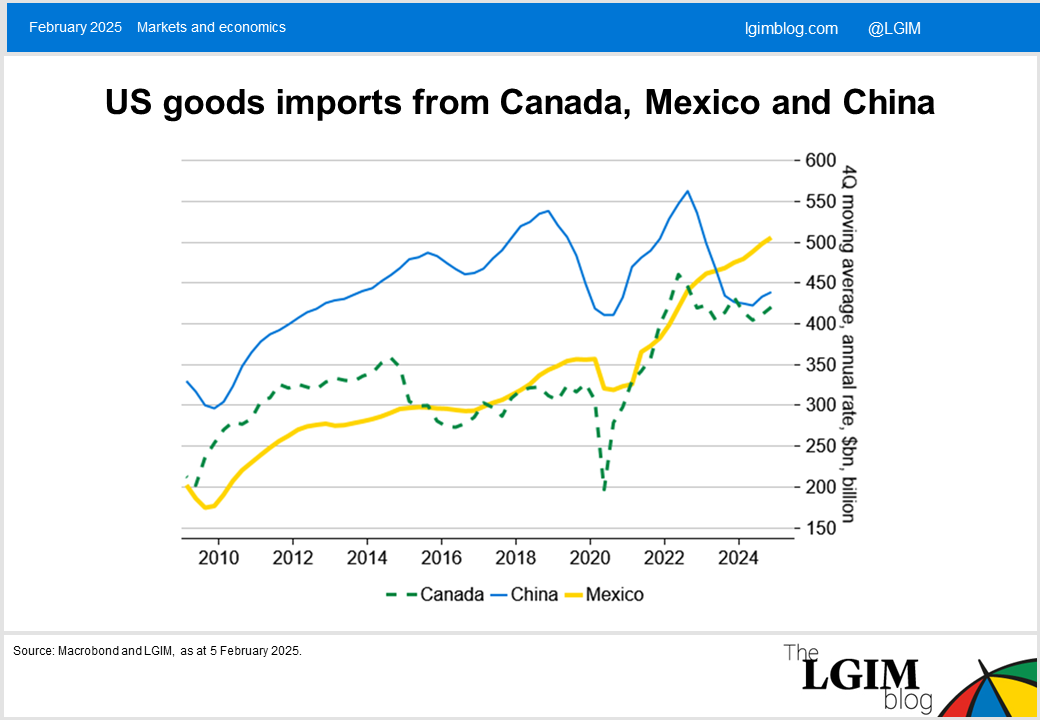

There was surprise that Mexico and Canada were the first to experience the threat of tariffs. At the last minute, these 25% tariffs were avoided, at least for the next month, in exchange for some minor concessions on policing their borders. China does not appear to have found an off-ramp and is facing an additional 10% tariff on all goods, but some deal on fentanyl could yet be agreed. However, this is only the first salvo in the trade war.

President Trump seems likely to continue to threaten tariffs as a negotiating tool. However, we believe there should be more focus on the structural approach to tariffs contained in America First Trade Policy – The White House. This is a comprehensive list of trade investigations which will be divided up between the Commerce Department, US Trade Representative and US Treasury.

The vast majority of reports are due by 1 April. Once the channels for executive action have been identified, there will probably be further consultations with business before the main tariffs are introduced and these could be deployed in stages and on products and countries.

These tariffs will be linked to reducing the US trade deficit, addressing unfair trade practices, increasing national security and raising revenue. It will be harder for countries to offer concessions. These tariffs risk retaliation and a broader global trade war.

Fiscal policy

The biggest policy agenda item is extending first-era Trump tax cuts before they expire at the end of this year. Congress is still to decide on the procedural process, but there is a heavy consensus this will get done. The big questions are whether there will be any additional tax cuts, since a mere extension would not be a stimulus, and how much of the extension or new tax cuts will be paid for with spending cuts or rolling back of the Inflation Reduction Act?

Government spending has been highly supportive for growth in recent years. Spending growth is set to slow, in our view, but how rapidly? Early indications are that the Department of Government Efficiency run by Elon Musk might prove more effective than initially expected. There was a chaotic attempt to freeze parts of Federal spending and this was quickly challenged in the courts. There is a Federal employee hiring freeze and employees have been encouraged to resign. Almost all of US foreign aid has been frozen for 90 days. We expect more attempts to impound funds legally authorised by Congress.

Immigration

The high-profile raids are attention grabbing. Still, it is not clear how much the pace of deportation has picked up under President Trump. However, border encounters were already falling sharply late last year and significant action has now been taken to virtually stop the inflows. We would not be surprised if the amount of payroll growth required to stabilise the unemployment rate falls to only 50k a month later this year if net immigration falls to zero.

Deregulation

This channel is hard to quantify. Most economists see deregulation as positive for growth, at least in the short run. We think the declaration of a national energy emergency could fail to deliver a significant boost to energy production. However, the relaxation of banking rules could free up capacity for increased lending.

Overall economic impact

The starting point is that we believe the US is showing the attributes of a soft landing. Growth has been strong, inflation appears on track to return to target and the labour market has cooled and now appears to be stabilising at equilibrium.

Consensus seems to believe the policies above roughly net off, leaving growth around 2% through 2025 and beyond. The US is seen as uniquely placed and supported by the Trump administration in energy production, technology, fiscal support and dynamism with an increasing expectation that productivity growth is in the process of stepping up

Corporate earnings have been strong and US businesses are generally sounding positive about the future, though some note tariff concerns.

We see significant downside risks to the US economy in 2025 because there is so much optimism around US growth. We worry that fiscal policy could underwhelm and immigration restraint and tariffs will act as negative supply shocks to a greater extent than consensus expects.

In part two of this blog series, we’ll discuss the potential market implications of President Trump’s policy agenda.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.