Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Is India the new China? Evidence on friend-shoring

Global companies are increasingly weighing geopolitical risk as they invest in China. Does India stand to benefit?

In this series of articles, we are exploring whether India might match China’s past growth experience in the coming decades.

In the first blog, we explored India’s fast-growing IT and service sectors and the role they might play in the country’s development.

Here, we consider ‘friend-shoring’ – i.e. the adjusting of global companies’ production and supply chains to favour India given growing geopolitical tension between China and the West. It’s a compelling narrative, but what is the evidence?

Making the move

There have recently been several high-profile reports of companies expanding their production capacity in India. Apple plans to shift 25% of its iPhone production to India by 2025, a marked increase from its current 6%[1]. Samsung plans to invest $356bn over 5 years and create 80,000 jobs in the semiconductor and biopharma sector[2]. Vedanta and Foxconn have announced that they will invest $19.5bn in a semiconductor and display plant[3], while Lockheed Martin and Tata have signed a deal to produce F-16 fighter jets in India[4].

It is obvious from these few examples that friend-shoring is more an issue in sensitive industries like semiconductors, defence, and electronics– less so for trainers and toys.

While these investments are yet to happen, the friend-shoring narrative has been a mainstay of sell-side reports for years. Recall that the Sino-US relationship has been deteriorating since the election of Donald Trump in late 2016.

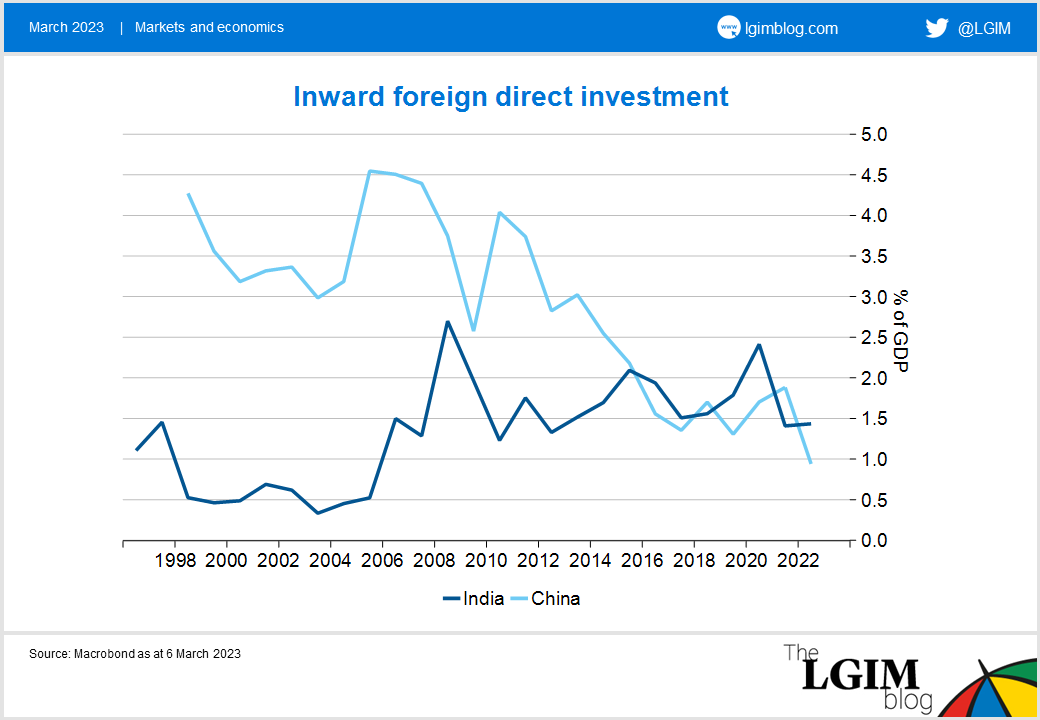

Foreign direct investment (FDI) into India has exceeded that into China in five of the past seven years, but that was due to a decline in Chinese FDI that started around the global financial crisis. India’s inward FDI has been stable at 1.5-2% of GDP since 2006, as we can see below.

So: little evidence of friend-shoring here.

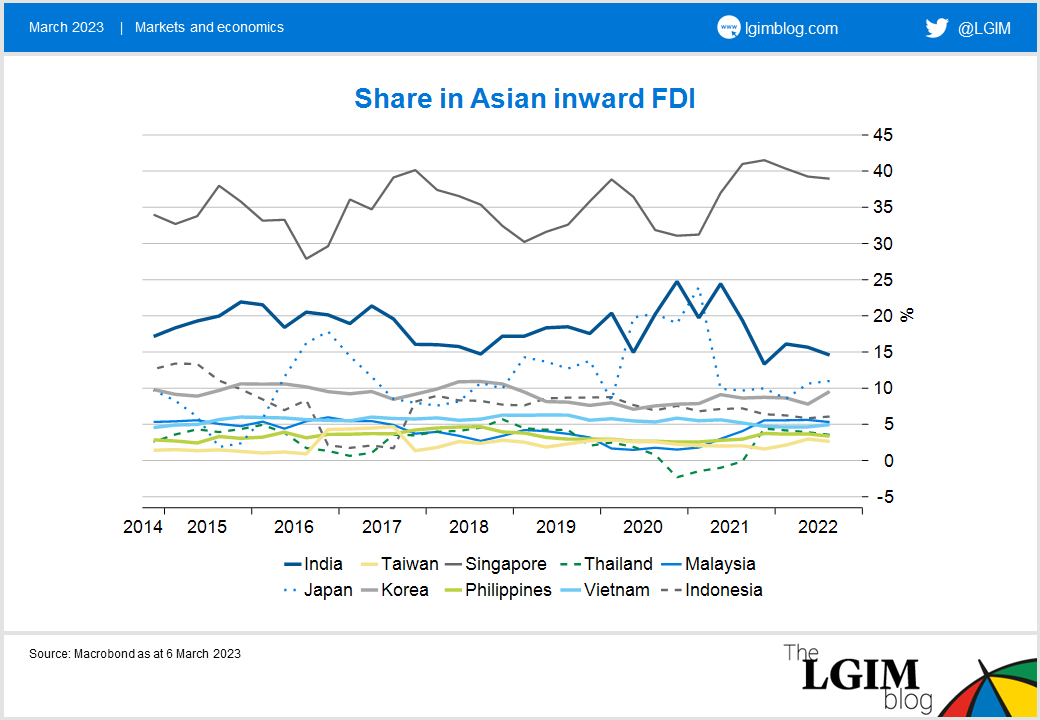

Of course, India might still have outperformed peers, if FDI was depressed across the world, for example owing to COVID. This does not seem to be the case: India’s share in Asian inward FDI has been stable at best:

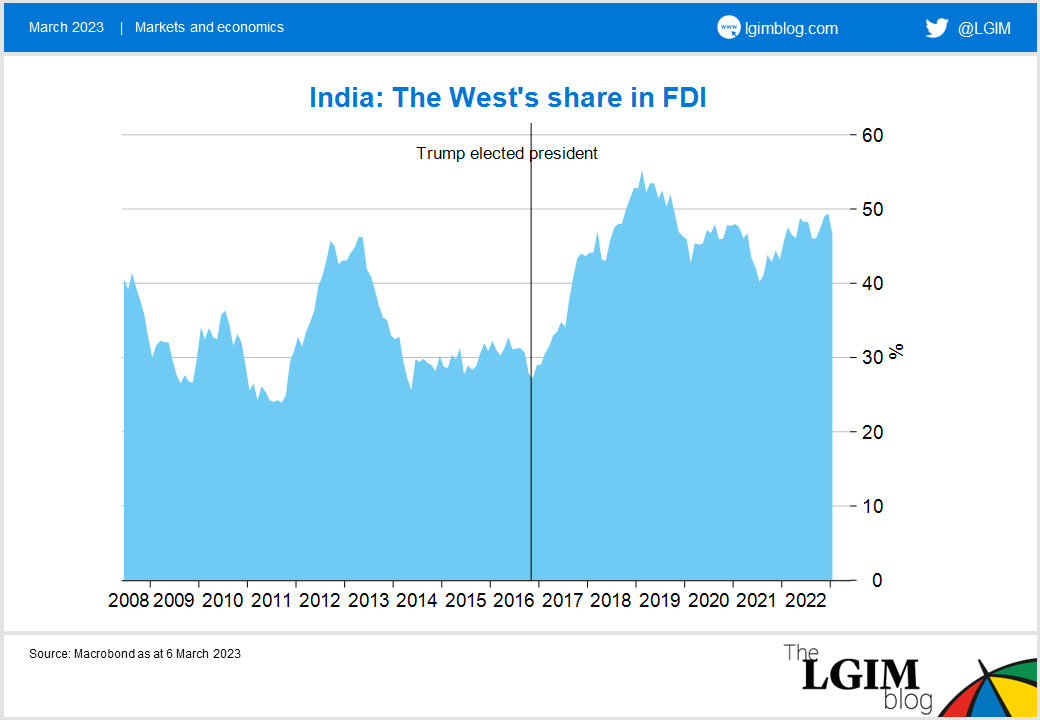

If we break down India’s inward FDI by origin, we find some evidence for friend-shoring.

Western promises?

Specifically, the share of FDI emanating from Western countries jumped from 30% to 50% after the election of Donald Trump. However, with overall FDI stable as a share of GDP, this additional investment from the West must have come at the detriment of other countries.

The macroeconomic evidence above is consistent with surveys conducted by the American Chamber of Commerce in Shanghai among some 312 members in 2022.

Only 17% of companies had considered moving operations or footprint out of China over the next three years. Earlier reports suggested that among those companies that considered shifting their activities, they were more likely to favour Southeast Asia than India.

It is important to note that the analysis here is backward-looking. The COVID-related lockdowns in China provided further proof of the advantages of supply chain diversification.

It can also be argued that Russia’s invasion of Ukraine added another point of friction to an already tense Sino-US relationship. However, at this stage friend-shoring is more of a leap of faith than a reality.

[1] https://www.reuters.com/technology/apple-targeting-raise-india-production-share-25-minister-2023-01-23/

[2] https://www.reuters.com/markets/europe/samsung-invest-356-bln-over-five-years-strategic-sectors-2022-05-24

[3] https://www.reuters.com/world/india/vedanta-foxconn-sign-mou-with-modis-home-state-20-bln-chip-foray-2022-09-13/

[4] https://www.reuters.com/article/airshow-paris-india-idUSL3N1JG3MT

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.