Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Home schooling

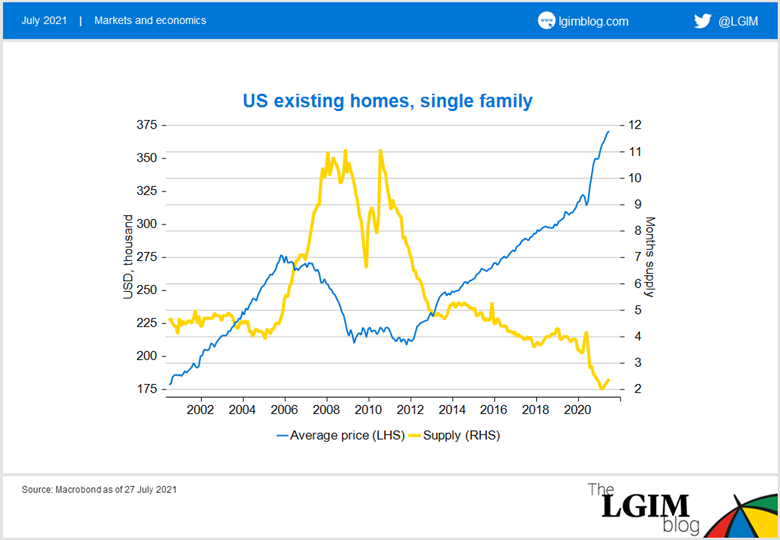

US home sales have disappointed in recent months and one sub-question in the Conference Board consumer confidence data has a weak reading on plans to buy a new home within six months.

This has led to suggestions housing is an early warning that US growth momentum is faltering now the stimulus payments and boost to growth from reopening are behind us. Concerns around the spread of the Delta variant are adding to these fears.

On closer inspection, however, housing fundamentals appear remarkably strong. Prices are surging and inventories appear extremely low. It is this combination that is likely to be frustrating potential buyers, rather than a gloomy view about the future. Overall, plans to buy a home are still high; it is just that people are unusually uncertain as to whether to buy a newly built or existing home.

We would therefore caution against focusing solely on new-home buying intentions. Homebuilders remain very optimistic and their equity prices currently reflect excellent earnings prospects (despite industry cost pressures).

Solid household fundamentals

The decline in household mortgage debt as a share of income in the US has continued through the pandemic (as income has risen). Debt is no higher now than in the mid-1990s.

With prices rising, the equity share in housing has returned to the levels last seen in the 1970s and 1980s. Yet the interest rate environment is totally different today with mortgage rates, aided by the Federal Reserve’s asset purchases, less than half the levels prevailing in the decade leading up to the financial crisis. This leaves mortgage debt servicing costs at historic lows. Even with elevated house prices, housing affordability looks reasonable based on the monthly repayments as a share of income.

Furthermore, the pandemic has led to a structural increase in housing demand. There has been a dramatic shift away from the high-cost large metro areas to parts of the country with greater space. With employment still to fully recover, I believe this demand has further to go.

Growth probably has peaked, but this was almost inevitable given the recent torrid pace. In the near term, the Delta variant may delay some of the handover in economic growth from goods consumption to services, but as virus worries fade, growth should remain well above trend through next year.

As part of the increasing pressure on resource utilisation, we expect residential investment to contribute positively to growth over the next few quarters.

In fact, the bigger worry is that today’s exceptionally low mortgage rates lead to a significant overshoot of house prices and construction over the next few quarters. If the US economy begins to overheat later in 2022 and into 2023, eventually leading to a sharp rise in interest rates, the housing market could be setting up to amplify the next downturn.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.