Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Emerging markets: the risk of sudden stops

Understanding capital flows is crucial for emerging market investors. Which countries could be most vulnerable?

Emerging markets typically have lower capital stocks per worker than advanced economies. This can potentially make them attractive for global investors in search of higher rates of return. However, ever so often foreign investors get cold feet, resulting in bank-run like crises in emerging markets. We believe that avoiding those sudden stops in capital flows is key for investors.

Sudden stops – defined here as a contraction in a country’s capital account by 5% of GDP or more – can be offset by drawing down foreign exchange reserves. However, if that is not an option, they tend to be painful. Domestic demand contracts by 5% on average but contractions of 10% and 20% were observed in Turkey in 2001 and Thailand in 1997. Growth stalls in the typical sudden stop and GDP contractions of more than 5% are not uncommon.

The economic pain can be mirrored in asset prices. History has shown that equity markets can fall by 25% in the typical sudden stop, while bond spreads can potentially rise by 500bps for investment grade sovereigns and more than 1000bps for speculative ones. Exchange rate moves of 15% are common, with moves of 35% possible when currency pegs break.

What are the determinants of sudden stops? We find current account deficits, external debt, other foreign liabilities, government debt, exchange rates (relative to moving average) and terms of trade to be significantly higher in years preceding a sudden stop. A country is also more likely to experience a sudden stop in years where we observe a general retrenchment of global capital flows.[1]

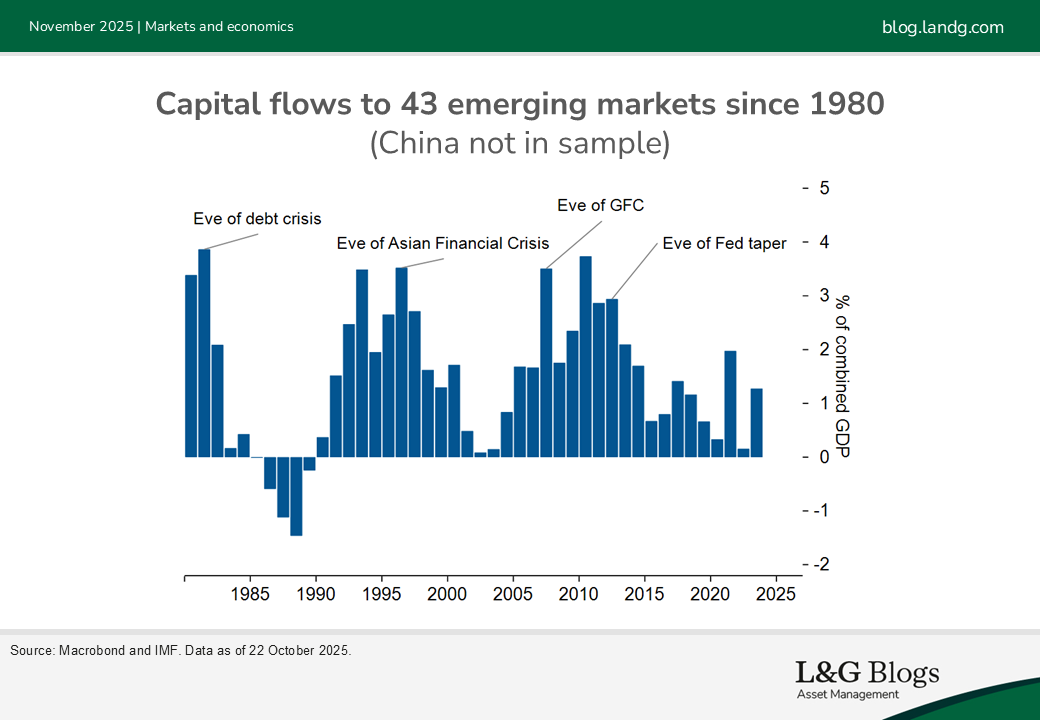

A casual look at some of those variables already provides a measure of re-assurance. For example, capital flows into emerging markets have been modest over the past decade, which could make a retrenchment less likely. Similarly, the median emerging market has run current account surpluses in the past few quarters. Not all variables give the ‘all clear’, though. For instance, the median stock of external debt remains close to all-time highs.

To arrive at a more rigorous judgement, we can seek to calculate the probability of a sudden stop for individual emerging markets using a Bayesian approach. This approach departs from the unconditional probability of a sudden stop – the number of sudden stop observations divided by all observations in our sample of 67 countries over 55 years.

It then updates this probability based on the reading of the above determinants for a given country.[2] Readings are judged against a threshold that aims to minimise the sum of false alarms and missed sudden stops. If readings are above the threshold, the probability of a sudden stop increases and vice versa.

We estimate the unconditional probability of a sudden stop next year to be a relatively low 7%. For comparison, we estimate that the unconditional probability of the US entering recession next year is around 15%. If all the determinants clear the threshold for a given country, the sudden stop probability falls to about zero. If all determinants breach the threshold, the probability of a sudden stop rises to 60%.[3]

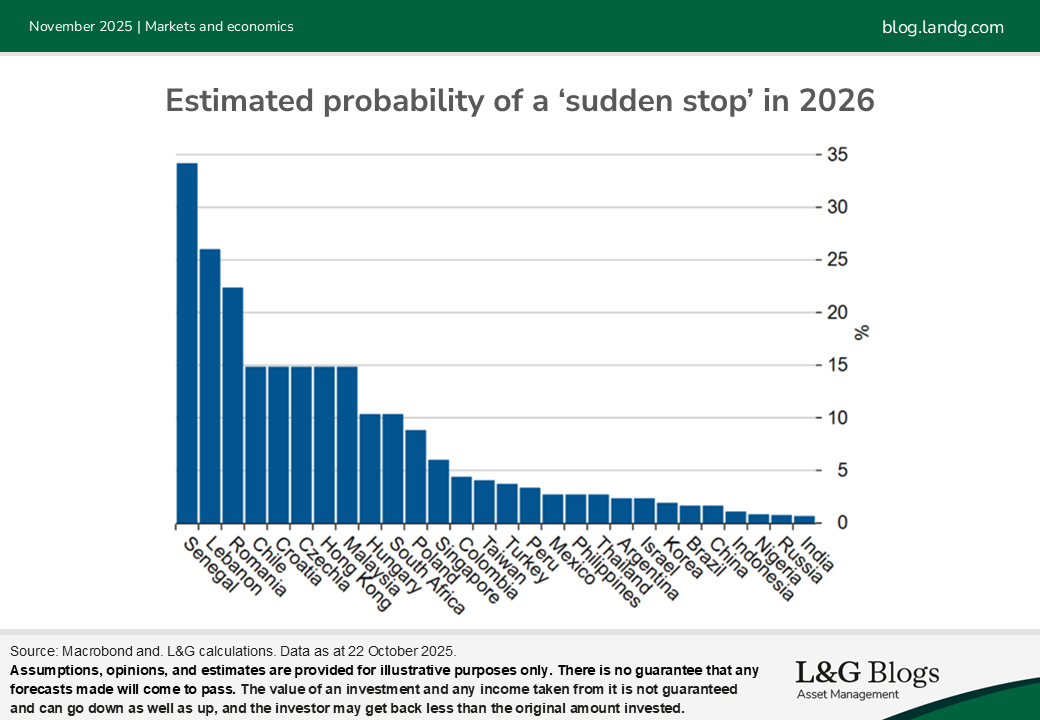

Our median estimated probability of a 2026 sudden stop for our 67 emerging markets is 9.4% – somewhat higher than the unconditional probability but, we would argue, still moderate. The figure shows the probability for a selected few. The country most at risk appears to be Senegal, with an estimated probability of 35%, followed by Lebanon and Romania. The country that’s potentially least at risk out of 67 is India. For Hungary, which experienced a sudden stop in 2023, the estimated probability has fallen to 10%.

What do we take away from this exercise as investors?

Models like the above are one of many inputs into our investment process and are taken with the appropriate pinch of salt. For starters, the predictors are far from precise. We have observed numerous sudden stops where external debt was not elevated and, conversely, high external debt has on multiple occasions not led to sudden stops.

Also, important factors are not captured in the model. For example, Romania, Croatia and Czechia – countries shown at higher risk of sudden stop are all members of the EU. This might give them access to extra safety nets and reduce the risk of bank-run like crises.

The other aspect completely exogenous to the model are valuations. Yes, the risk of sudden stops looks low, but some markets are pricing that already. Sovereign spreads, for example, have become so tight that we in Asset Allocation have removed our long-standing EM credit overweight. In the case of Romania specifically, we have a favourable view, with potentially attractive levels of spread offering more than adequate compensation for the risks in our view.

However, the model does provide a rigorous confirmation of the conjecture we derive from Figure 1, namely that violent capital outflows from EM tend to be preceded by large capital inflows. With EM having been starved of capital in the past decade, the risk of sudden outflows should be low. And, while that may be reflected in the price of EM credit, that is less clear for equity, forex and rates markets.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass. The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested.

[1] In addition, there are country characteristics like openness and smallness that make sudden stops more likely

[2] Four of the predictors are not independent and are looked at jointly.

[3] The probability never reaches 100%, because the predictors are imperfect. They miss sudden stops and trigger false alarms.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.