Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Dividing the cake: can you hear the price-wage echo?

Firms and workers are fighting over a bigger share of the cake. The problem is the cake is too big for central bankers, so there are twin threats to corporate profits.

A ‘wage-price spiral’ is a common description of how inflation took off in the 1970s.

Energy shocks triggered wage rises that in turn raised core inflation. High inflation became embedded in the system and a painful recession was unfortunately needed to stamp it out in the early 1980s.

What about today?

We describe the current situation as a ‘price-wage echo’. An echo can theoretically get louder, but normally fades. We think core inflation will fall back, but iterative echo effects will slow its return to target. Following the initial price shock from supply disruptions, workers will fight to restore purchasing power while companies attempt to maintain profit margins, leading to another round of wage and price hikes even as the initial supply disruptions fade.

The chicken or the egg?

There’s currently a chicken-and-egg discussion as to what is to ‘blame’ for high inflation: prices or wages. A recent US academic paper argued uncompetitive (oligopolistic) markets allow firms to exploit bottlenecks (Sellers’ Inflation, Profits and Conflict: Why can Large Firms Hike Prices in an Emergency?). The European Central Bank (ECB) has also expressed surprise at how rising profits have boosted the GDP deflator. Typically, a surge in imported energy costs should squeeze profitability as firms struggle to fully pass on costs. Perhaps, as per the Sellers’ Inflation paper, firms have exploited heightened cost fears to jack up prices.

Rising profit shares could just be a timing issue. If prices can adjust quicker than wages (salaries are often updated annually), then the initial response to a shock could be higher prices and profit share. Later, labour contracts are renegotiated and the labour share of income recovers.

Nevertheless, my preliminary investigations suggest branded products have gone up by more in both absolute and percentage terms than ‘own brand’ products, despite the latter having a greater share of raw materials and energy in their cost base. Higher energy prices don’t boost the cost of advertising.

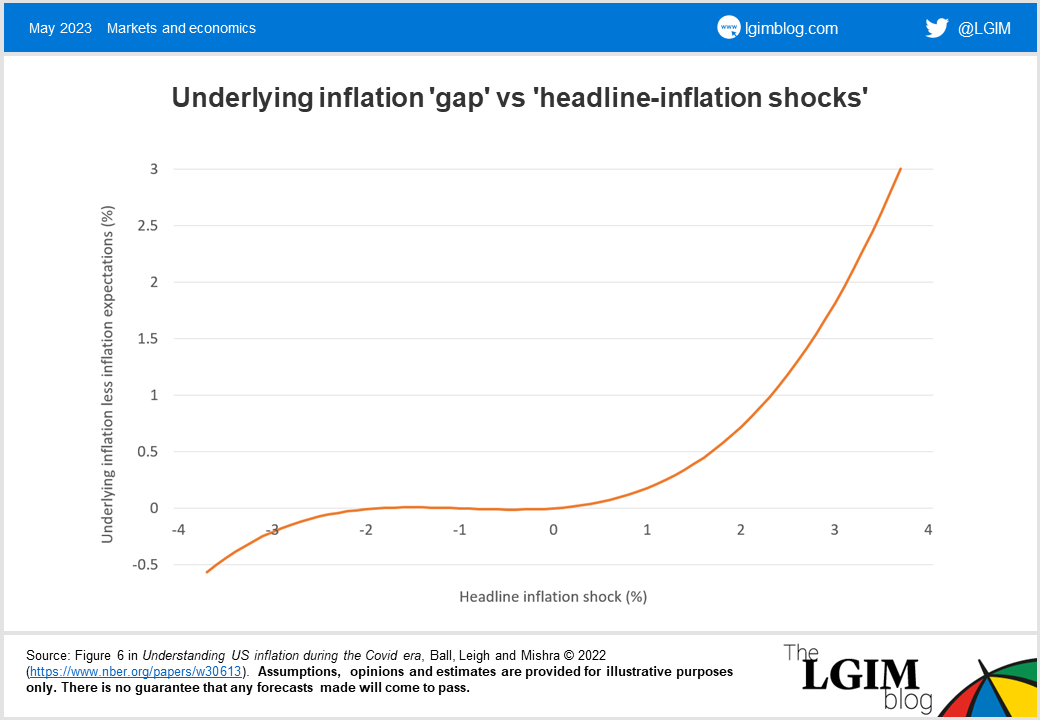

Macroeconomic papers also point to asymmetric and non-linear effects of commodity shocks to core inflation. The chart below shows the estimated impact on underlying inflation (y-axis) from shocks to headline inflation (x-axis, typically energy). Positive commodity cost shocks are more likely to be passed on than negative ones. This is consistent with oligopolistic markets. Moreover, non-linear effects suggest bigger shocks are easier to pass on than smaller ones.

I make the following conclusions after reviewing the papers:

- Fewer downside risks to inflation from a ‘normalisation’ of goods prices. Many prices have soared in recent years and I keep hoping they’ll revert back towards normal. But maybe the higher price is the new normal. In my view, this reduces the chance of ‘goldilocks’ whereby lower prices boost real incomes and make it easier for policymakers to take their foot off the brake

- Profits under pressure from smaller share of the cake and central banks reducing the size of the cake. Firms and workers are fighting for a bigger share of the cake. But the problem for central bankers is that the cake is growing too rapidly. As per the paradox of thrift, perhaps we’re also in the paradox of inflation. It makes sense for each of us to raise our own price – that makes us relatively better off. But if we all raise our prices that creates inflation, forcing central banks into restrictive policies. Either way we see profits under pressure. Either because rising labour costs squeeze margins or because tighter policy pushes the economy into recession

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.