Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Degrees of doubt

AI, anecdotes and the graduate labour market: why the threat may be more gradual than feared.

As we hit peak graduation season, my inbox is inundated with alarming anecdotes of the impact of AI on the graduate labour market. “Canary in the AI coal mine”, “jobs market devasted by AI”, “AI is stealing young people’s futures before they have even started” – are some of the headlines. As an economist with a teenage son, I’m doubly interested in this topic. But when I delve into the data, the picture appears more nuanced than the headlines suggest.

Most of the evidence comes from vacancies on jobsites like Adzuna* or Indeed*. The most comprehensive analysis is from McKinsey* on the UK labour market. Looking across industries, it finds a slight negative correlation (R^2 6.4%) between the change in online job adverts and AI exposure since mid-2022. It also shows graduate roles are down 33% versus a 28% fall in non-graduate roles. The problem is we have no back data to put this into context – either in terms of typical volatility or vacancy levels.

My biggest critique is the starting point. The write-ups often point out that Chat-GPT was launched in 2022. But it was also the peak of what I’ve previously shown was ‘war-like’ labour-market tightness following post-COVID reopening (see my previous blog).

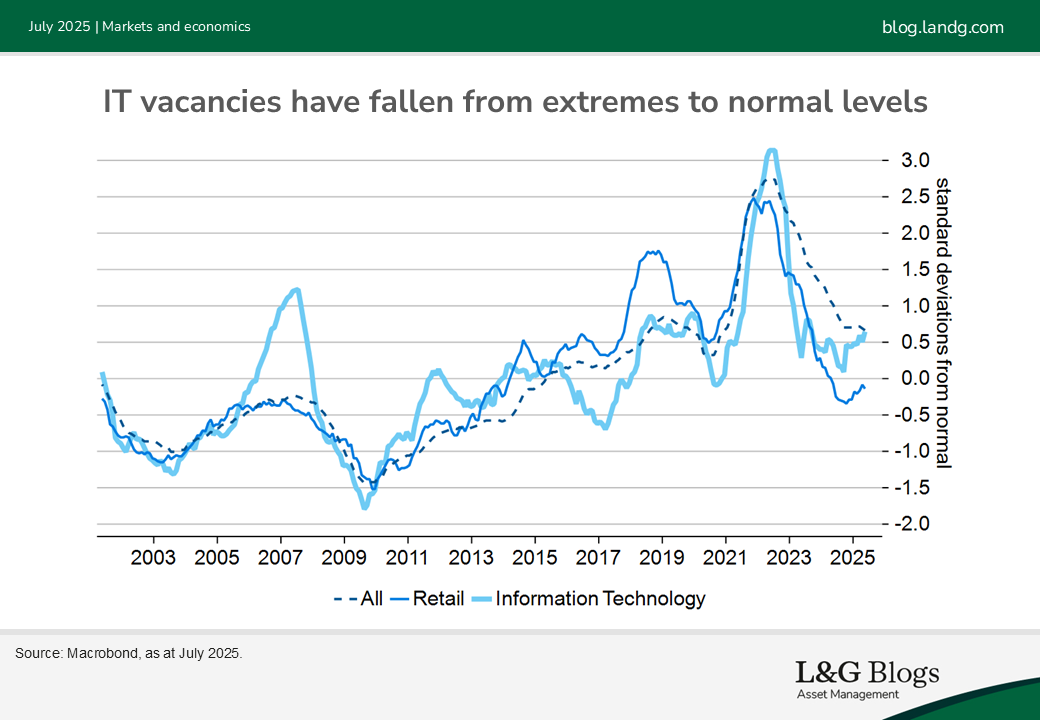

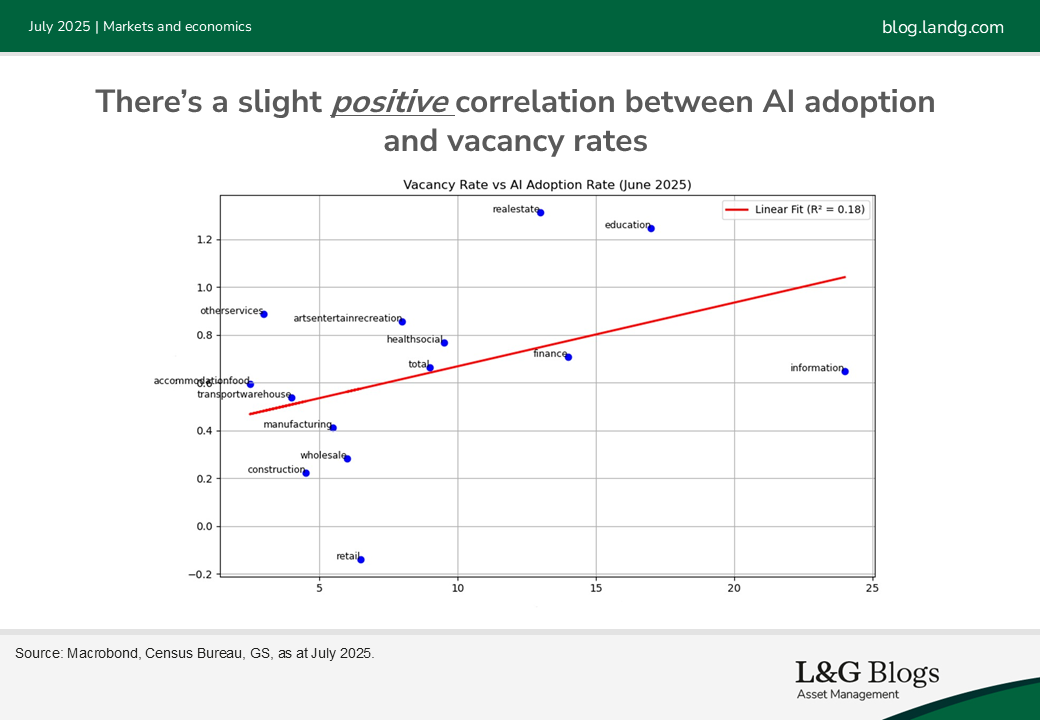

This was especially true in IT, as the world moved online. In level terms, the bigger they come, the harder they fall. So while the IT sector (which has the highest AI adoption) has seen a large percentage fall, this partly reflects its extreme starting position. In level terms, US IT vacancies have stabilised in line with both their long-term average and the broader economy. Moreover, there’s also a slight positive correlation between AI adoption and vacancy rates in level terms.

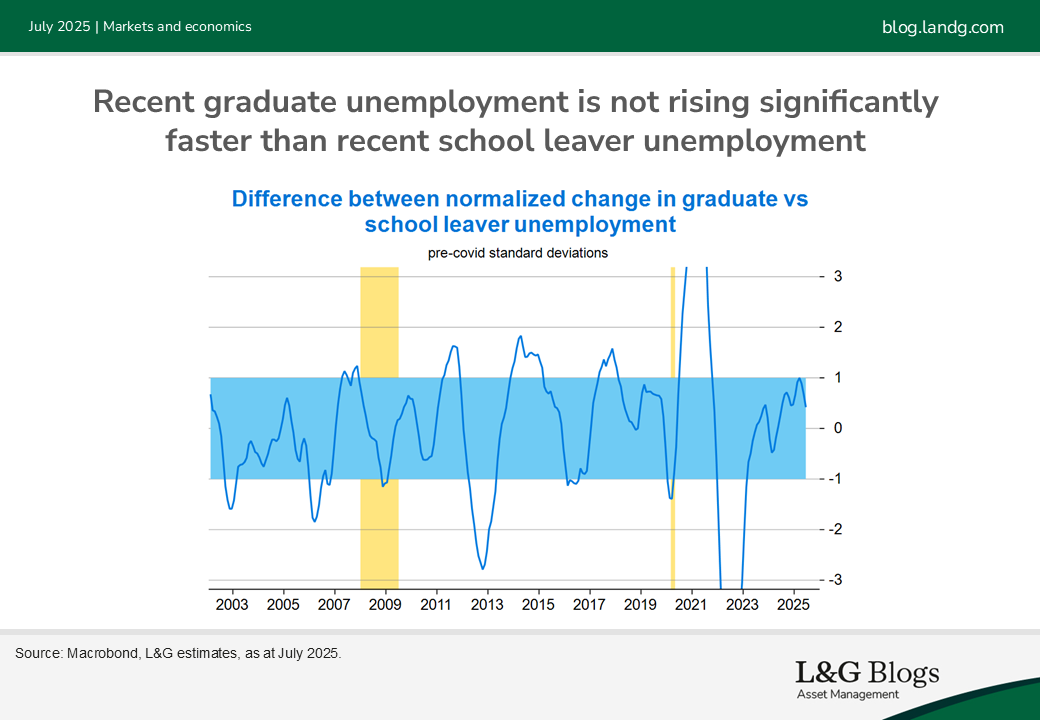

The Federal Reserve Bank of New York has also explored the issue. In a recent blog it showed how unemployment among recent graduates had risen relative to their peers (others aged 22-27). The problem with this is it’s the wrong counterfactual. A high-school leaver in their mid-20s has years of experience under their belt, so is settled and advancing in their career. This is not the appropriate comparison for a fresh university graduate. Instead, we should be comparing recent school-leavers with recent university leavers.

Why? Because in an economic downturn firms stop hiring. So the rise in graduate unemployment could just reflect a cyclical hiring freeze given macro pressures of tighter monetary policy rather than a technological change. When we look at the change in school leaver versus graduate unemployment over the past year (adjusting for the higher volatility of school-leaver labour market), we find no significant difference.

This suggests the rise in graduate unemployment could be due to a broader hiring freeze. Or the AI revolution is affecting lower and higher skilled occupations similarly, which is not consistent with fears of AI moving up the value chain and hurting the ‘graduate’ labour market. Moreover, the NY Fed blog also shows that underemployment of graduates (working in lower-skilled jobs) has not increased. Again, this points to a broader cyclical hiring freeze than a technological change.

So while the headlines of sharp falls in graduate job vacancies are concerning and could be forward-looking, they’re difficult to put into context with no back data. A broad assessment suggests nothing unusual is going on in graduate unemployment versus school leavers or the level of job vacancies in AI-affected areas. AI adoption is rising, and as we saw following the dot.com boom, the next recession is likely to accelerate cost-cutting structural changes.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.