Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Taking a close up look at the Argentina crisis.

Taking a closer look at the crisis in Argentina.

Despite the slowdown in global growth, which now appears to have stabilised, very few countries are currently suffering a proper recession. The notable exceptions are Hong Kong and Argentina.

As an economist, holidays are a chance to study the anatomy of a downturn first hand (and to be described as an ‘econ geek’ by my 14-year-old daughter). As I live with a currently weak currency in Britain, a dollar-pegged Hong Kong and riots were not appealing; more enticing was the two-thirds depreciation of the Argentine peso (ARS) over the past couple of years.

Strolling through Buenos Aires revealed a country in crisis and the ravaging effects on poverty of a 50% inflation rate. As Magda highlighted over a year ago, Argentina has become stuck in its high inflation, high external debt and depreciation quicksand, which assistance from the International Monetary Fund (IMF) has so far been unable to solve.

Some prices had failed to adjust to the currency collapse and so appear remarkably cheap for tourists, while imported luxury brands had risen in line with the depreciation. Restaurant prices were about one-third the cost of London. Regulated taxi fares meant a 10-minute cab journey was around 100 pesos (barely over a dollar). The tips were gratefully received. The underground was embarrassingly cheap at 20 pesos (due to price freezes since March which implies increased subsidy and fiscal cost). But they were also clean, punctual and air conditioned – South West Trains, please note!

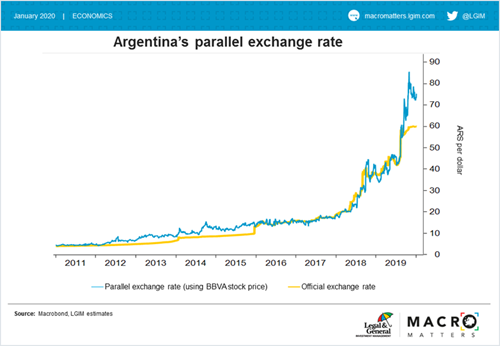

Setting the peso

The one business which is clearly booming is clandestine foreign exchange. There is a desperate shortage of dollars due to capital controls, the impending sovereign debt restructuring, and punitive taxes on trade. Furthermore, nobody wants to save in pesos because of the expected future depreciation, preferring dollars in bank safety deposit boxes.

Official foreign exchange outlets are a bureaucratic nightmare with restrictions on the amounts of dollars which can be exchanged. The banks are unattractive with huge fees and severe limits on cash withdrawals. This has led to cries of ‘cambio, cambio’ on every street corner in the centre of Buenos Aires.

After negotiating a price, clients are led into tiny rooms down side streets (known as ‘Cueva’ – an exchange office hidden inside a regular business unit which is a façade to cover the real transactions) to see the boss and receive rates currently at least 20% better than the official exchange rate.

If like me you don’t fancy the risk of dealing with an unlicensed entity, many of the shops and restaurants took card payments and were happy to offer discounts to tourists or take dollars at favourable exchange rates. The unofficial exchange rate is posted on the blue dollar website or can be calculated by taking the dollar and peso prices of the same assets listed on different stock exchanges.

So what’s the trade recommendation (other than visiting Argentina with a suitcase full of dollars and a security guard)?

The real depreciation is already substantial and, while confidence is unlikely to be restored under fears of another profligate Peronist Fernandez-Kirchner government, it is hard to short the peso given the carry costs and exchange-rate management. Sovereign bonds are already priced for a major default.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.