Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Does fast food show emerging currencies are cheap as chips?

The COVID-19 pandemic led to massive capital outflows from emerging markets, some of which have now reversed. It also caused large swings in current accounts, which affect supply and demand in emerging-market currencies. To analyse how this turmoil has changed the valuations of these currencies, we employ three workhorse models, two based on relative prices and one based on current accounts.

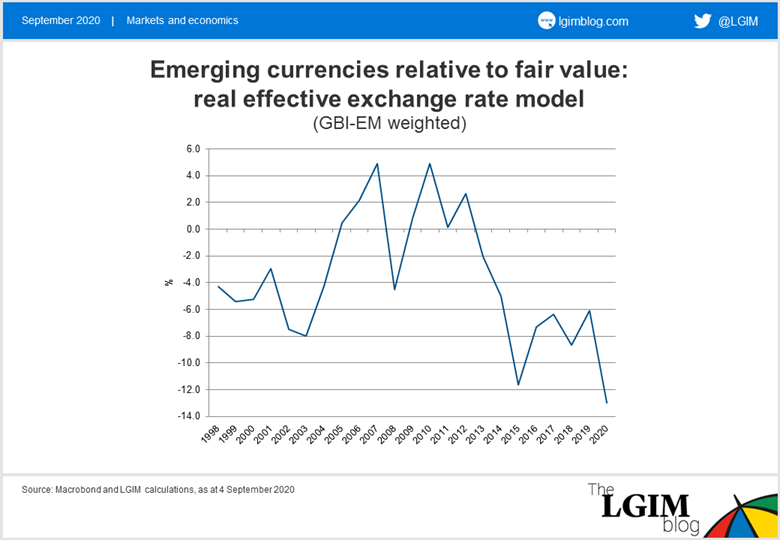

The starting point of the first model is that things should cost the same across countries that trade freely. The model therefore tracks price levels in a country relative to its trading partners when all prices are converted into US dollars at prevailing exchange rates (the so-called real effective exchange rate). Rising relative prices point to an overvalued exchange rate.

In reality, matters are a bit more complicated. Countries that have higher productivity or a commodity boom can pay higher wages in the export sector, for example. Wage pressures then spill over into the wider economy and raise the general price level. Our model therefore corrects for productivity and commodity or government spending booms when assessing the real effective exchange rate.

The chart below shows emerging markets’ real effective exchange rates relative to their fair value, using a GBI-EM weighted average. The last observation, corresponding to September 2020, suggests that emerging currencies have not been this cheap since at least 1998.

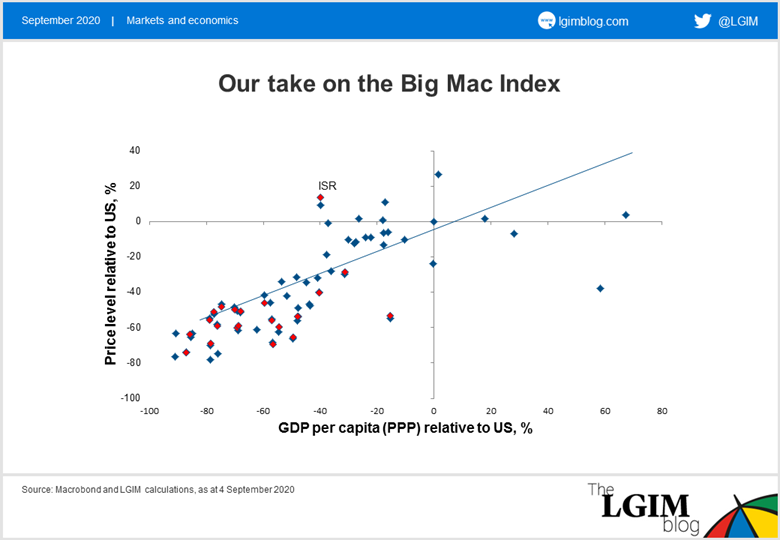

The second model has been popularised by The Economist as the ‘Big Mac Index’. Instead of tracking relative prices over time, it looks at the price of a Big Mac across countries at a given point in time. As before, Big Mac prices are converted into US dollars at prevailing exchange rates.

In our version of this model, we don’t use the prices of Big Macs, but of an identical basket of goods. To account for the fact that prices are higher in countries with higher productivity, we plot the price level against countries’ level of development.

The next chart shows this scatter plot with emerging markets marked in red. Again, emerging-market dollar prices and, hence, currencies are weaker than their level of development would suggest (the big exception being Israel).

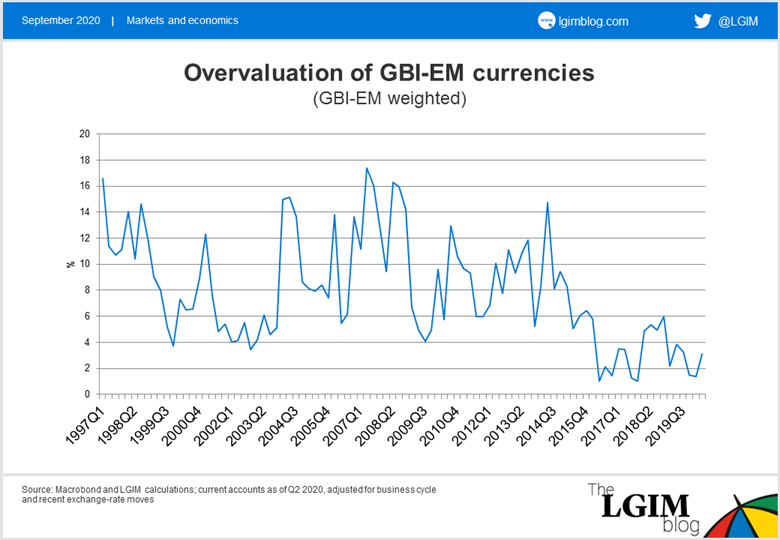

The third model assesses currencies on the basis of current account balances. More specifically, it sees large current account deficits (cyclically adjusted) as a signal of overvalued exchange rates. This is because investors should eventually balk at financing large current account deficits, at which stage the currency collapses. The model asks by how much the currency needs to fall to return the current account to more sustainable levels. This is the degree of overvaluation.

Some researchers see large current account surpluses as a sign of undervalued exchange rates. However, large surpluses and associated exchange rates are much more sustainable than large deficits, which reduces their usefulness for currency valuation and forecasting.

This final chart shows the GBI-EM weight of countries with overvalued exchange rates multiplied by their degree of overvaluation. This captures the breadth and degree of overvaluation observed among emerging markets.

Consistent with earlier findings, this model shows that the overvaluation in emerging currencies is at its lowest since at least 1997.

All three models send a clear signal that emerging-market currencies are cheap. Yet this is not a new phenomenon arising in the wake of the pandemic. Emerging currencies have been cheap according to these models since the taper tantrum of 2013, when Brazil, India, Indonesia, Turkey and South Africa were singled out as the ‘fragile five’.

The corollary is that emerging currencies could stay cheap for a bit longer. Nevertheless, in conjunction with a catalyst (such as investors’ hunt for yield when a vaccine reduces uncertainty) – or for the long-term investor – cheap currencies should prove a boon.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.