Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Currency market at a standstill

One of our currency traders told us last week that she has been seeing the same spot levels in developed currency markets for months now. It’s not that we love volatility, but there is a lack of action in the currency space. Even this week’s scare about potential contagion from China's property sector has so far had little effect on currencies.

Idea generation is easier when prices are on the move as momentum traders will enforce the trend up to the point where positioning and sentiment become stretched, and a contrarian approach starts to look more promising.

We know volatility has been low across financial markets, reflected in the realised volatility of assets and implied volatility in option markets having dropped sharply since the pandemic peak in March last year. But where equity volatility (e.g. the VIX index) and bond volatility (e.g. the MOVE index) have tended to move more sideways in recent months, currency volatility in developed markets continues to grind lower (e.g. the CVIX index).

The impact on prices of this low-volatility environment is quite different too. It’s a boon to equity markets, with one market after another having reached new all-time highs over the summer; a blessing for credit issuers keeping spreads historically tight; and a godsend to bondholders, with longer-end yields reversing much of the sharp increase from earlier this year despite high inflation prints. Stable spreads and yields may sound dull, but they allow fixed-income investors to continue earning that credit spread and capture the rolldown of longer-dated bonds.

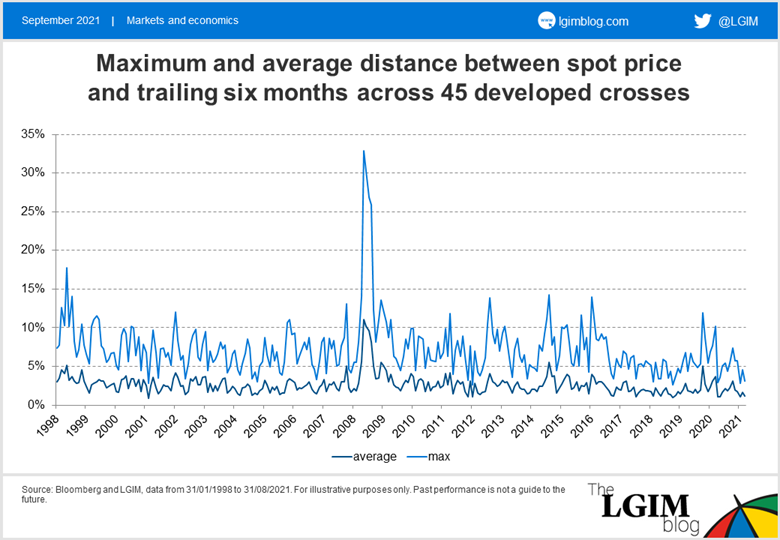

In currencies, things are different. Carry is almost non-existent with interest-rate differentials at a historical bottom, while spot prices have stopped moving. To quantify our trader’s observation, we calculated the average distance between today’s spot price and the six-month trailing average across all 45 developed crosses (as portrayed below). That average is just 1%, close to its lowest point over 20 years, which illustrates that developed currency markets are stuck.

We don’t have many active currency positions open and don’t take much risk in this asset class at the moment. It’s tempting to chase smaller and smaller movements, but in our view it wouldn’t be good portfolio management and so we prefer to be patient and wait for bigger opportunities to come.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.