Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Chart of the month: Poles apart?

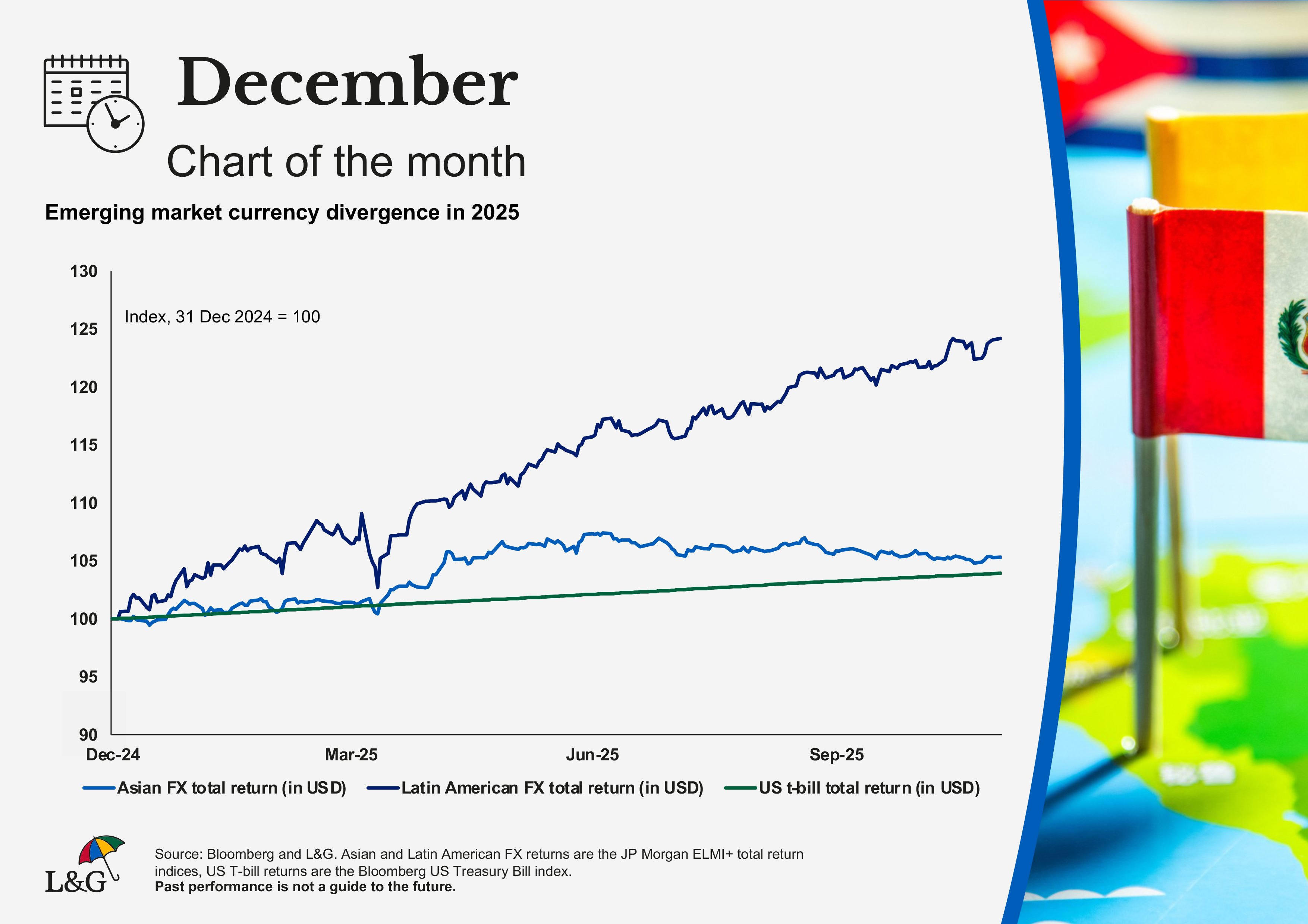

We assess the divergent path of emerging market currencies in 2025.

Investors often make the mistake of bracketing emerging markets as one amorphous block subject to global shocks. When you read headlines like ‘A weak dollar will be good for emerging markets’ or ‘Emerging markets to suffer as funding conditions tighten’, there is an implicit assumption that their fortunes are joined at the hip. We think that is a mistake, and 2025 has been testament to that. Our chart of the month highlights the divergent trends in foreign exchange (FX) markets over the past year.

In Latin America, we have seen currencies benefit from inflows chasing high real interest rates, bolstered by the US administration’s modern-day Monroe doctrine with respect to their ‘near abroad’. The first is a legacy of hawkish monetary policy from the regional heavyweights in the last couple of years. The latter is a story of fears about dismantling the trade agreement with Mexico and tariffs on Brazil having given way to hopes about support for Argentina and a regional tariff rollback. Returns been stellar, with regional currency benchmark up over 20%.

In Asia, where real interest rates are substantially lower, currencies have largely been treading water despite a small rally in the Chinese yuan this year. There have been a number of idiosyncratic stories behind the weakness, but the common threads that link them are Chinese economic malaise offering little positive growth impulse for the region and more transactional US diplomacy weighing on sentiment (secondary sanctions on India, an unequal trade and investment agreement with Korea). Investors could have earnt 5% by putting their money into Asian FX this year, which was barely more than was available by taking no currency risk and investing in US T-bills.

The difference between the two regions has been particularly stark in the second half of the year. Since June, the rally in Latin America has continued apace whereas Asian FX has been underperforming consistently. The message here is that we need more nuance when talking about emerging markets rather than tarring them all with the same brush.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.