Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Could UK interest rates be peaking for this cycle?

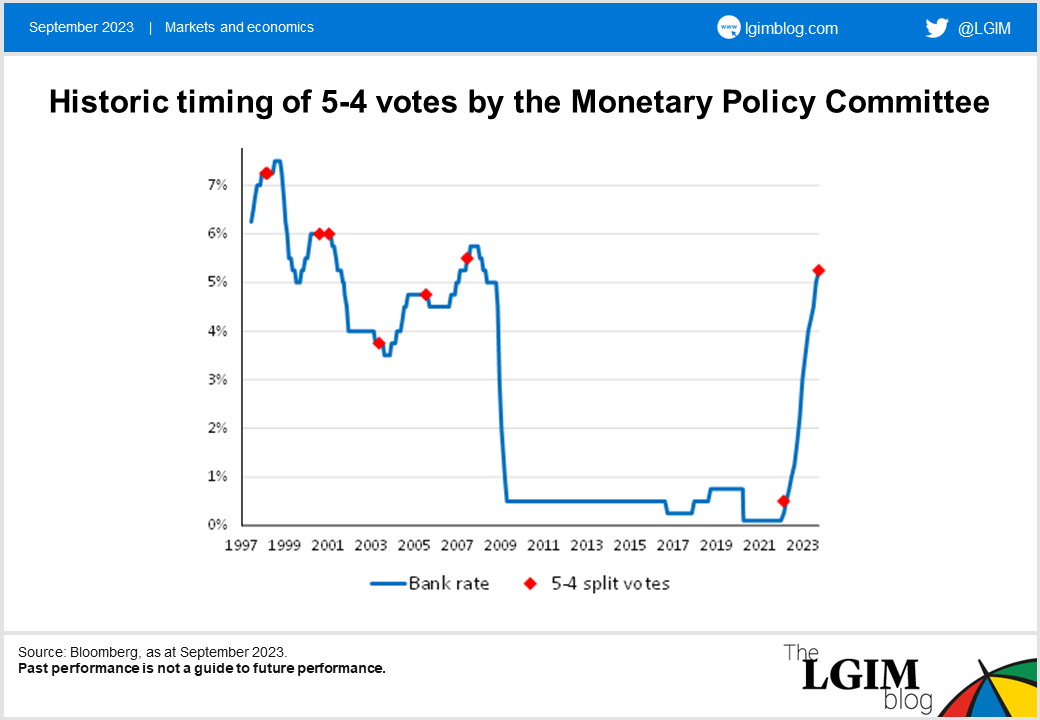

Opinion at the latest Monetary Policy Committee meeting was highly divided, with the vote split 5-4. How often has this happened before, and what could it mean for the future trajectory of the UK base rate?

Split votes at the Bank of England (BoE) are common, but a 5-4 split on the Monetary Policy Committee (MPC) is not. It’s roughly as likely as Eric Morecambe’s favourite scoreline: Fife 4, Forfar 5.

But that’s what happened at the last MPC meeting, with the Old Lady of Threadneedle Street opting to pause her rate hiking cycle after 14 consecutive increases. The MPC was split down the middle, with Governor Andrew Bailey casting the deciding vote to tip the balance in favour of leaving UK rates unchanged this time around.

The prior week’s inflation data seem to have sealed the deal for the doves. Core CPI may still be running at 6.2% (i.e. more than three times the BoE’s target), but the direction of travel is important. Leading indicators (from either surveys of recruitment consultants or purchasing managers) suggest that the turn in both wage growth and service sector inflation is imminent.

The interesting thing about 5-4 votes is that, based on historic data, they often seem to come at inflection points for BoE policy. The last one was in February 2022, just as the current tightening campaign was getting started. The one prior to that was in June 2007, just as the previous hiking cycle was coming to an end.

It was a similar story at the peak of the preceding cycle in 2000. You might say that we’ve previously only seen 5-4 votes when the policy outlook is at sixes and sevens. That would be unkind, but it does provide a strong hint that we could be at the turning point in the interest rate cycle.

The kneejerk market reaction to the BoE’s ultimate decision to leave the base rate unchanged has seen sterling weaken, which has been a potential boon for sterling-based investors with portfolios with unhedged currency exposure.

Furthermore, the gilt market has avoided the trend of globally rising yields since the start of September. We’ve been overweight gilts for several months in our portfolios anticipating that yields could fall back from elevated levels, but have taken profit on those positions after a good run.

However, if the historic precedent for split votes at the BoE holds true again and we’re at or close to a peak the UK base rate for this cycle, then there’s potential for further long positions in gilts in future, particularly if the global economy enters recession as we anticipate.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.