Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

The alchemy of mania

Bubbles are hard to identify in real time, but the parabolic price rise in precious metals is showing all the hallmarks.

There is lots of chat about bubbles, primarily focused on AI. On this topic I am uncertain. Could this be the moment hope triumphs over experience (I started my career in the late 90s)? However, I feel more confident (relatively – one can never be that confident about markets) calling out the recent price action in precious metals as a classic speculative mania.

The popular narrative

All manias have a good story. Once gold broke free from the shackles of real yields and the dollar, the new paradigm began. This coincided with Russia’s invasion of Ukraine. Since then, geopolitical uncertainty is seen as ratcheting higher, matched by the increasingly unsustainable US fiscal deficit. Investors are thought to be beginning to move out of dollar assets. Many believe this process could have much further to run.

In the case of gold, central banks have been a price-insensitive buyer, steadily diversifying their foreign exchange reserves. There is also belief in the market that China is significantly understating its purchases. There are new sources of demand for gold, such as to underpin stablecoins. Tether has disclosed itself as one of the largest non-sovereign holders of gold in the world, amassing a stockpile of approximately 140 metric tonnes (just under 1% of the stock of gold ever mined in human history).

Silver has an even more seductive narrative. Not only is it part of the ‘debasement trade’ but it is catching an epic fundamental bid from the rapid growth in AI investment. Silver is used across AI infrastructure from semiconductors, electrical distribution, storage and thermal management (to help cool data centres). At the start of the year, China reclassified silver as a strategic mineral. This has led to export restrictions and reports of state stockpiling. This seems to be compounded by anecdotes of a retail buying frenzy across parts Asia with queues and bullion dealers running out bars.

Supply of gold and silver is very inelastic. Gold is scarce, while silver is primarily a by-product of other mining activities, making new supply less sensitive to price. The value of gold ever mined at current prices is in the $30-40 trillion range. Visually, this would form a cube measuring 22.5m on each side. The total value of the smaller silver market is estimated to be $6-7 trillion. So it only takes a modest increase in either investment or industrial demand to move prices.

Questioning the vibe

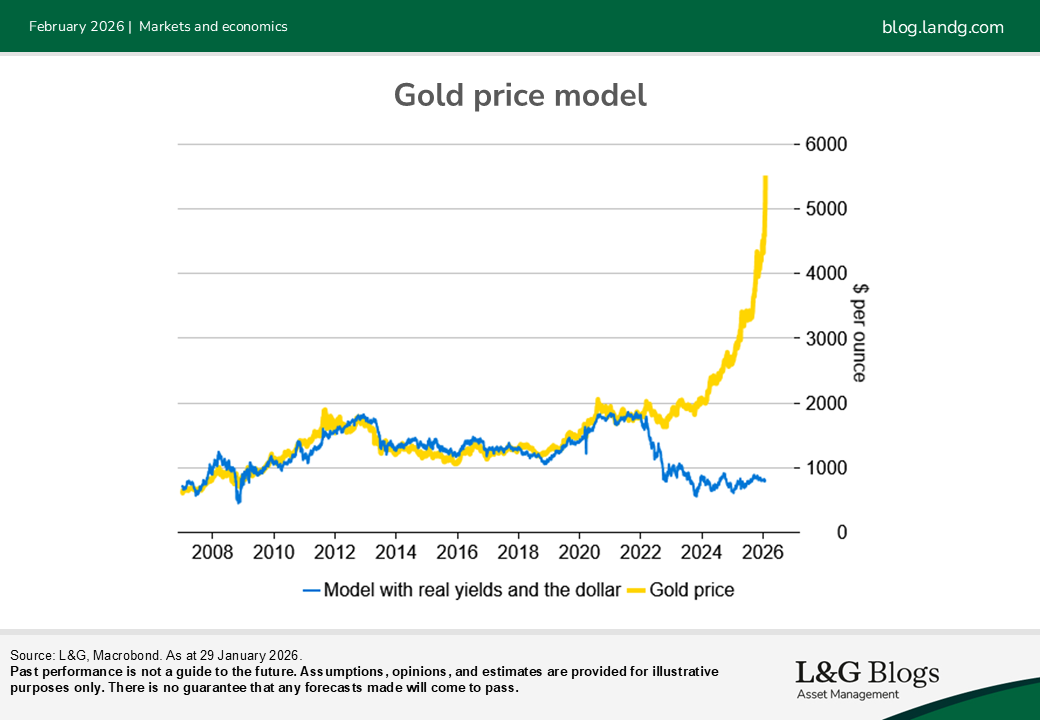

Long-term worries about the US economy are nothing new. We believe that the twin deficits should ultimately put downward pressure on the dollar and be a tailwind for gold. But the timing for the sudden price spike is strange. The macro outlook has improved in recent months. Economists have revised up growth forecasts without expressing any increased concern about inflation.

Risk assets also appear remarkably sanguine. Since Liberation Day, the US has backed off from some tariffs and a global trade war appears to have been averted. If this is a dollar debasement trade, why is the dollar not significantly weaker and why is the gold to silver ratio collapsing when central banks don’t buy silver?

Furthermore, inflation expectations remain well contained. If you are worried about inflation, we believe the index-linked bond market appears to offer a cheap hedge. True, these have been poor investments as real yields rose. But if you now hold to maturity, you can lock in positive real yields. If there is concern around CPI manipulation and mistrust of government then why are investors selling ‘digital gold’ to invest in ‘physical crypto’?

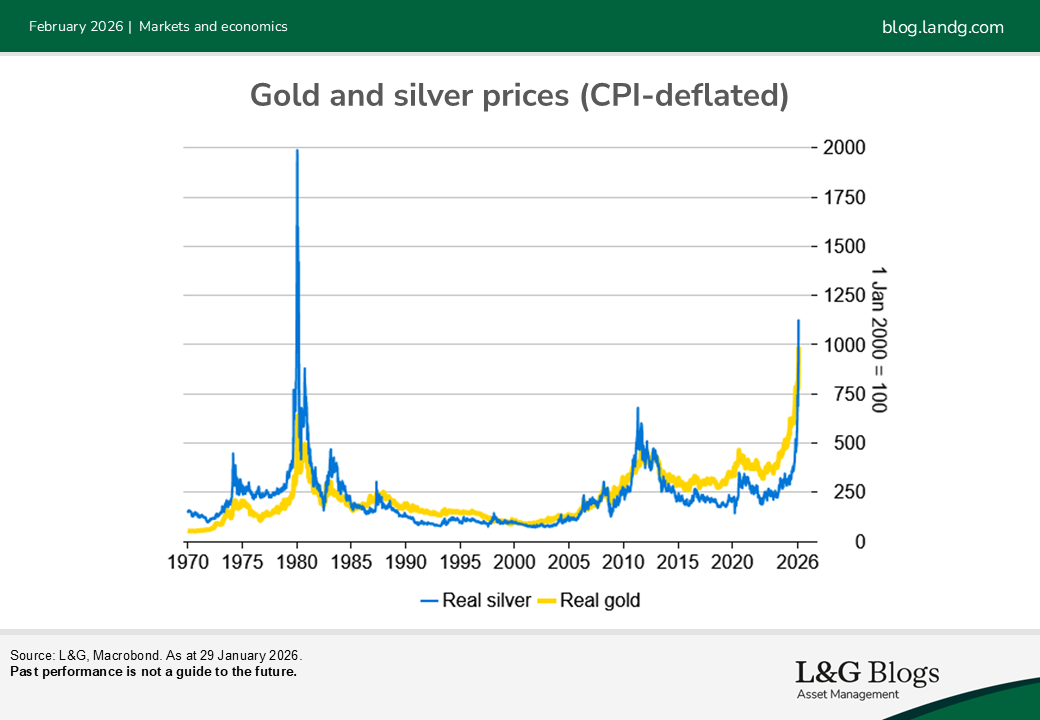

It is also hard to value precious metals, which makes it tricky to identify a bubble. There is no anchor, no future revenues and they pay no income. But relative to their own history the charts are striking. Gold in real terms has tended to chop sideways for decades, until the recent price spike to a record high. Silver has been higher once before in real terms, during the infamous Hunt brother attempt to corner the market in 1980.

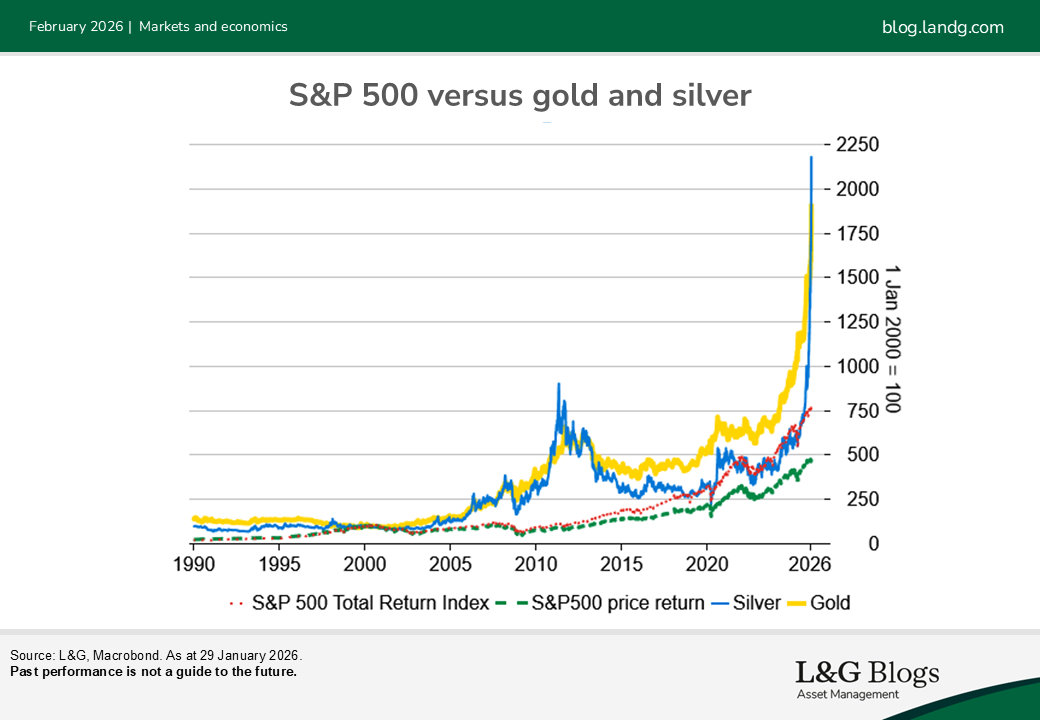

The outperformance of gold and silver relative to equities is harder to explain. Comparisons are sensitive to the market chosen and the time horizon, but even looking at total returns of the S&P500 (one of the strongest equity markets since 2000), they have significantly outperformed. One needs to go back to mid-1990s for S&P500 total returns to have beaten silver.

The popular narrative highlights strong structural tailwinds for gold, but does not fully explain the price moves in recent days which I think reflect an additional layer of speculation. Momentum-driven buying is being amplified by the fear of missing out. A parabolic price curve can signal a final flurry of intense buying as rational analysis gives way to more speculation and hype.

Crash watch

I’ve no idea how much more extreme the situation can become. Momentum is hard to fade and the trigger is not obvious. I first started to voice concern about silver in October. My colleagues point out that prices have subsequently more than doubled since then. So even a repeat of ‘Silver Thursday’, which for most is unthinkable, only takes silver back to these levels.

Given heightened speculation, alongside the structural tailwinds which show no sign of reversing, the risk of severely volatile moves, especially in silver, is probably greater than a long drawn out bear market. Good luck out there![1]

[1] This blog was written on Thursday for publication early this week. Since that point, there has been a massive plunge in precious metal prices, especially silver amid extreme volatility.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.