Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Chart of the month: Picking up pennies

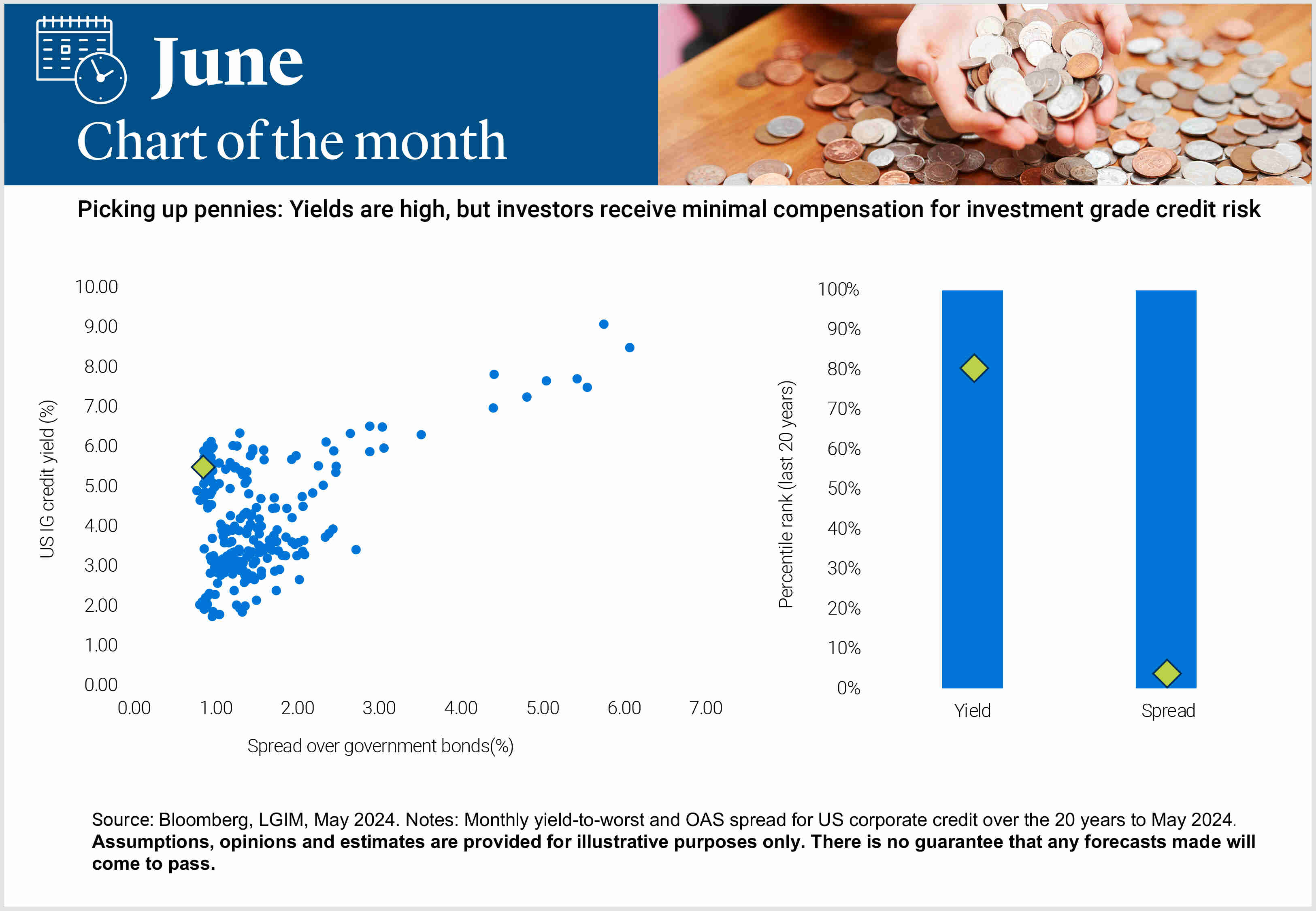

There is a cautionary tale in financial markets about those that indulge in 'picking up pennies in front of the steamroller'. In our view, some credit investors may need to take heed.

As regular readers may recall, for most of the year we have held the view that there is an optimistic narrative priced into risk assets. Indeed, the idea that developed economies will avoid recession, see inflation return neatly to target and begin to loosen monetary policy is now somewhat consensus. While current data supports this view, we see a much broader range of plausible outcomes, leaving markets vulnerable to a shock should the unexpected occur.

No asset class demonstrates this vulnerability more obviously than credit, in our view. While in equity markets there is always upside potential, with no theoretical limits if earnings grow or valuations expand, in credit markets that is not the case. It’s a case of simple mathematics. If credit spreads tighten to zero, there is nowhere else to go.

After all, why would an investor wish to take the credit risk when one could simply own a government bond and target the same expected return?

Consequently, we believe investment grade credit in particular faces a skewed return profile. Credit spreads have little room to compress, but no theoretical limit on how wide they could move if we encounter a bump in the road. Investors can target a marginal excess return versus government bonds as they pick up the pennies. But will this offer sufficient compensation should they end up squashed by the steamroller?

One of the main positive tailwinds to credit performance has been the absolute level of yields. As the charts above illustrate, investors are currently receiving one of the most attractive yields on US credit in the past 20 years. With many investors focusing on total returns, they have been willing to accept paltry credit spreads, ‘safe’ in the knowledge that so long as market conditions remain supportive, they could target an attractive return. The economic backdrop so far in 2024 has been benign and there are few signs of delinquencies among borrowers, which has supported this view.

We believe there are more attractive ways to target comparable levels of return, with less potential downside risk. Given our view that there is a broader range of potential scenarios in play than those reflected in asset prices, we prefer to own government bonds and seek our excess return in potentially better compensated parts of the market.

In particular, we see value in US inflation-linked bonds, given the elevated level of real yields, as well as in hard currency emerging market debt.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.