Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Chart of the month: EU-turn

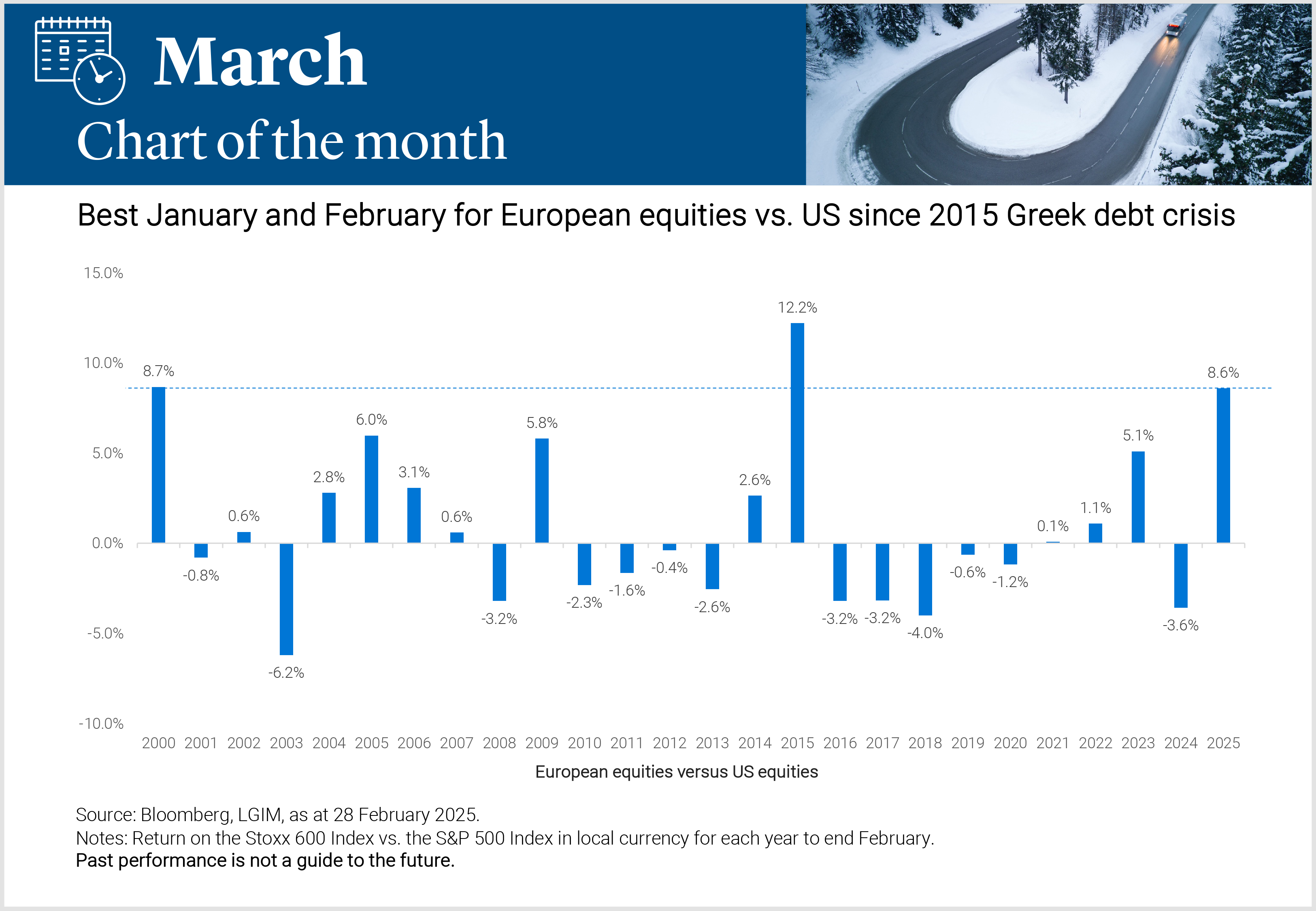

One of our potential surprises for 2025 was a resurgence in non-US equities. In this vein, it’s certainly been a bumper start to the year for European equities relative to their US counterparts. What’s driving this?

This year has seen the best start for European equities relative to US equities since 2015, with the Stoxx 600 index outperforming the S&P 500 by 8.6% to the end of February. The result is even more anomalous when you consider that the two previous highs both occurred in times of crisis.

In 2015, Europe was engulfed in the Greek debt crisis, leading to significant swings in financial markets. It has been 20 years since we’ve seen such a strong start to the year for Europe in a non-crisis environment, when US equities fell from their dotcom bubble peak.

So, what’s is driving this shift? As with any attempt to rationalise movements in equity markets, we have to show a degree of humility. A portion of the change may simply be random noise that is hard to attribute to a single factor. However, we see a few potential forces that may be influencing market movements.

Firstly, the move occurred against a backdrop of extraordinarily strong positive sentiment towards the US and weak sentiment for Europe. For example, in our survey of 2025 predictions produced by professional analysts, every single report showed a preference for US equities. Conversely, most analysts were pessimistic about the outlook for Europe. This sentiment was reflected in investors’ portfolios, with prominent industry surveys showing one of the largest overweight positions in US relative to Europe since 2001.

Sentiment and positioning can be like an elastic band. They stretch and stretch until eventually something unexpected happens and then can snap back rapidly. When everyone believes the same thing and has their portfolio positioned accordingly, if circumstances change, it can cause a rush in the same direction, which can lead to outsized changes in market prices.

We believe the likely candidate in early 2025 was the release of Deepseek’s open-source AI model, which led investors to question whether the gains from the AI revolution would be quite as large and concentrated in the US as many had assumed. The model performed well on a series of benchmark tests and is around 30x cheaper than the leading US equivalents.

While there is plenty of reason to be sceptical that this upends the AI trend in equity markets, when positioning and sentiment is so stretched, even small developments can lead to large price swings. We continue to like the AI theme, but prefer a more diversified** implementation that has less of a concentration in a small number of mega-sized US companies.

Finally, not all the action was driven by US developments. European equities struggled over the latter half of 2024, as macroeconomic data weakened and political uncertainty increased. Since the start of 2025, we have started to see some small improvements in economic data, particularly in surveys of company confidence, and European political uncertainty appears to be gradually fading.

This likely also contributed positively towards investor sentiment in European equities. We remain relatively balanced from a regional perspective, preferring to focus on high-quality diversified** exposure across markets, avoiding excessive concentration in any given area.

All data is sourced from Bloomberg as at 31 January 2025, unless otherwise stated.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an LGIM portfolio. The above information does not constitute a recommendation to buy or sell any security.

**It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.