Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Chart of the month: Could the ‘Magnificent 7’ become the ‘Fabulous 5’?

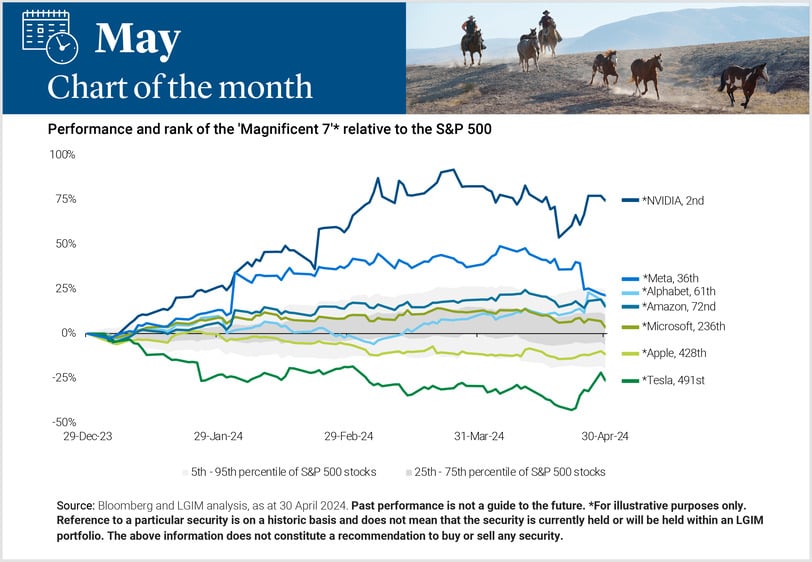

Leading US stocks have seen divergent fortunes of late, as investors assess the capex cost of AI.

The extraordinary performance of the ‘Magnificent 7’* US stocks – which has driven US equity markets higher for much of the last 18 months – may have led some to watch the 1960 film which inspired the name. Anyone who watched to the end will know that (spoiler alert) four of the seven eponymous gunslingers don’t make it. The performance of the ‘Magnificent 7’* stocks this year suggests this group may also be shrinking.

Last year, all seven of the group enjoyed a boost from market appetite for AI. More recently, two of the group, Tesla* and Meta*, have acknowledged in their results that, for now, their AI exposure is costing them a lot of money, and bringing little immediate payoff. That has seen their share prices fall notably, with Tesla down 25% year to date, and Meta down 18% from its recent peak earlier in April. The combined loss of market cap of these two companies over these periods amounts to around $550bn, or nearly a quarter of the value of the FTSE 100[1].

After a relatively smooth journey higher in 2023, the group appears to be offering the potential for greater volatility and more mixed returns. The question from here is, will these cracks in the engine room of the S&P 500 dent the broader appeal of big cap US equities? Or, as members of the seven potentially fall by the wayside, could the concentration risk in US equities only build further if the group becomes a ‘Fabulous 5’ or even a ‘Fantastic 4’?

After a period focused only on the opportunities of AI, there is now growing investor recognition that those opportunities could come with a cost in the form of capex. It seems likely to us, therefore, that the path forward for US equities could remain bumpier than it has been, and diversification[2] within equities potentially better rewarded.

[1] All data correct as at 30 April 2024.

[2] It should be noted that diversification is no guarantee against a loss in a declining market.

* For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an LGIM portfolio. The above information does not constitute a recommendation to buy or sell any security.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.