Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Chart of the month: Are US rate cuts necessarily bullish for US equities?

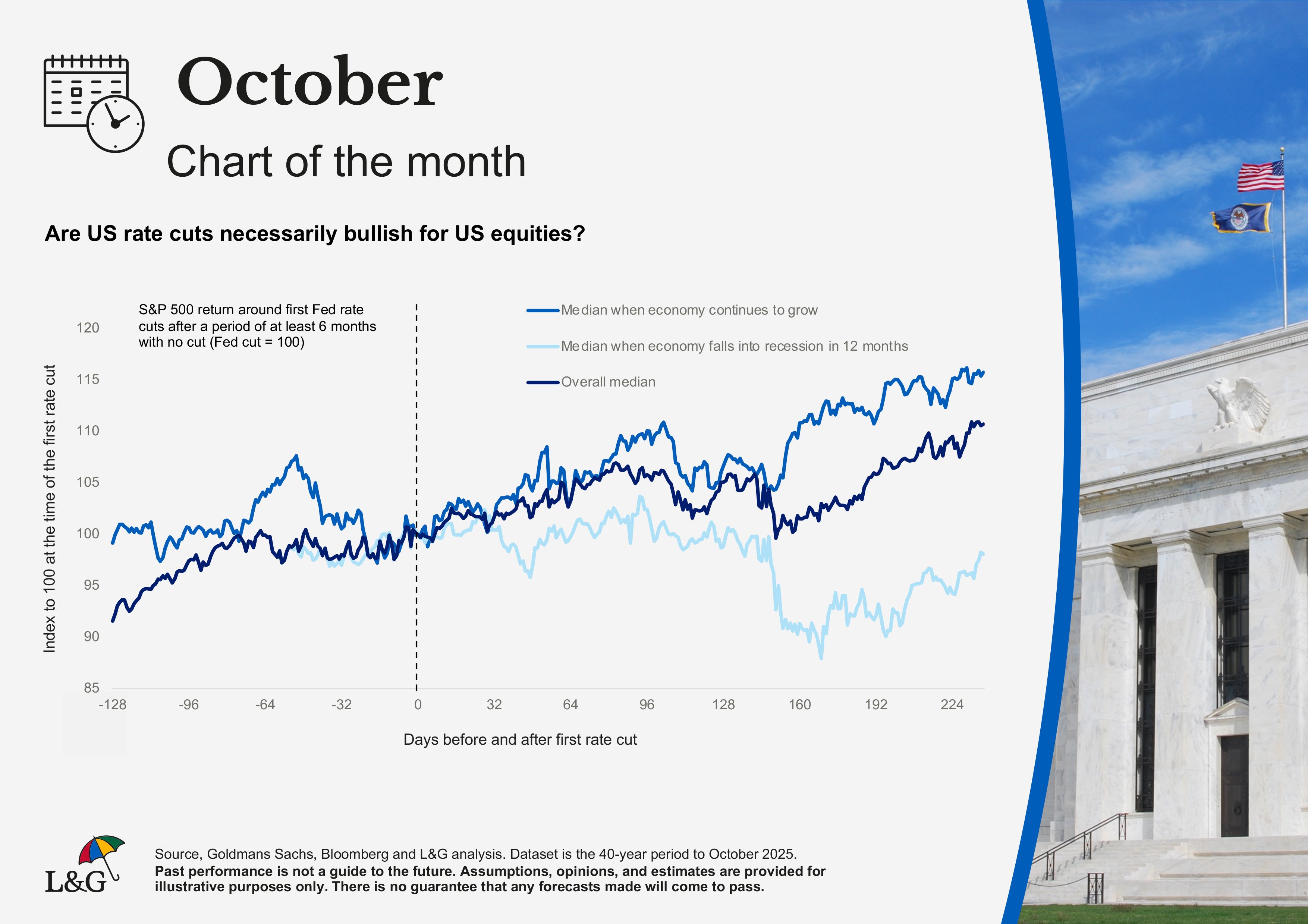

Equity investors are often minded to cheer when the US Federal Reserve begins a cutting cycle. But what do the last 40 years of history have to say about the matter?

Recently, investor minds have turned back to 1998, when a market crisis – then volatility in Asian markets and the collapse of the hedge fund LTCM – pushed the US Federal Reserve (Fed) into easing rates, despite a buoyant US economy. That crisis proved isolated, and the cuts by the Fed arguably helped underpin the extraordinary run in US equities (led by tech) which unfolded over the 18 months or so after the Fed intervened.

Now, we are recovering from the intense volatility associated with President Trump’s ‘liberation day’ reciprocal tariffs. Again though, with thus far limited read through to consumer prices or corporate profits, this might be a disruptive event which has proved contained, but which has helped tip the Fed into a more dovish stance than might otherwise have been the case.

Ultimately though, history suggests that whether a cutting cycle proves bullish or bearish for equities can depend upon the pathway for the economy. Recent history suggests that investors face a 50:50 probability. When the economy proceeds to fall into recession – as has been the case in around half of the cutting cycles commenced over the last 40 years – the period after the Fed starts cutting has been challenging for equities. When the economy has gone on to avoid recession, gains in markets following the commencement of a cutting cycle have been particularly strong.

For now, investors appear confident that this time will be one of the latter, more optimistic occasions, when Fed cuts are more of an insurance policy and the economy continues to grow. Time will tell.

Past performance is not a guide to the future. Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.