Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

CAMERA: currency assumptions in focus

There’s no ‘right’ answer, but it’s important to understand the impact of different approaches on long-term return forecasts.

The article below is an extract from our Q2 2025 Asset Allocation outlook.

Producing expected return models can reveal important assumptions that might otherwise be hidden. Here we want to shine a light on currency assumptions. Choosing between alternate but sensible currency assumptions can lead to big changes in expected returns.

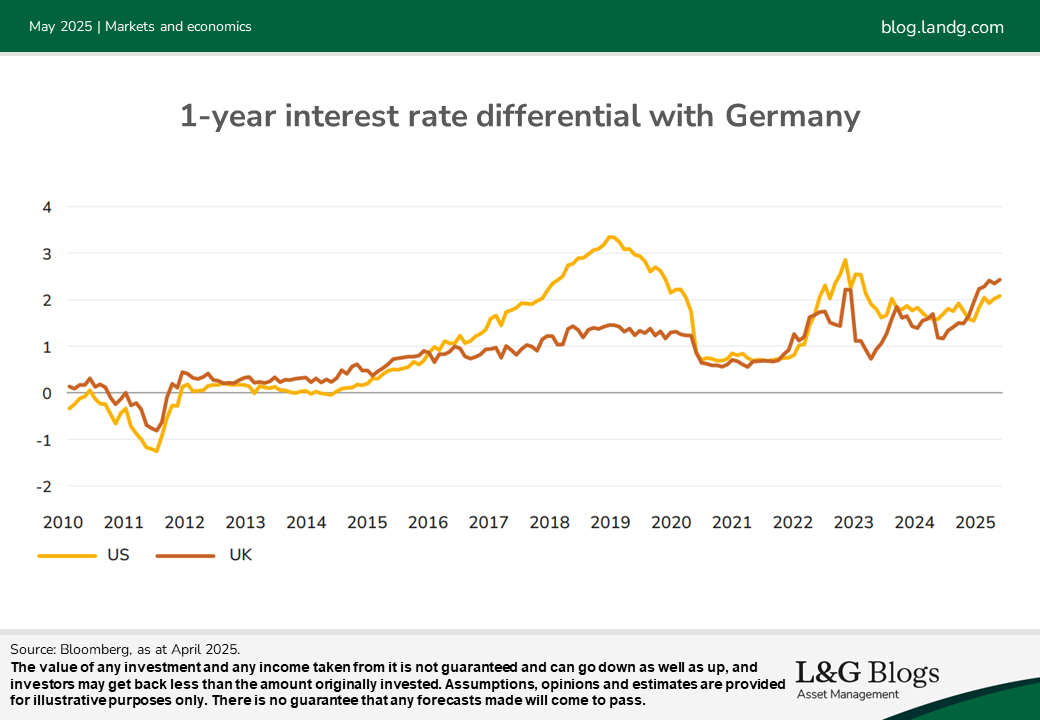

Interest rate differentials

Currency assumptions tend to come in a few different varieties. These assumptions frequently relate to interest rates, either explicitly or implicitly, through inflation differentials. Commonly used assumptions in expected return estimates include:

- Uncovered Interest Rate Parity (UIP): Expected currency movements will offset interest rate differentials

- Relative Purchasing Power Parity (relative PPP): Future currency movements will equal the inflation differentials between the two countries

- Constant Spot Exchange Rates: Hold the currency constant at the current level

When interest rate or inflation differentials are large, choosing between these assumptions can make a big difference. This is particularly true for euro-based investors today.

Picking the ‘right’ model

Unfortunately for investors, no assumption is definitively the best. Each assumption has some merit or some empirical evidence that you could interpret in its favour:

- UIP has a strong theoretical foundation and is consistent with it being hard to earn returns from simple carry trades. However, there is evidence that various risk premia are rewarded in FX markets, even if it is not always the case.

- Relative PPP is often used in economics, where it is based on the Law of One Price i.e. you shouldn’t be able to make a profit simply buying a good in one place and selling it somewhere else (within limits). But empirical evidence is mixed and if Relative PPP does hold, it is often not true over short periods.

- Constant Spot Exchange Rates are a sensible choice if you think the exchange rate is a random walk, and it is also easy to understand. The Bank of England uses this assumption in some of its projections. But it ignores all the theory embedded in UIP and relative PPP.

For our developed market equity assumptions, we use relative PPP over a five- to 10-year horizon. For strategic asset allocation assumptions, which anchor the long-term estimates in CAMERA, we assume UIP.

In practice, that means you can earn carry over the medium term if real interest rates differ across countries, but in the long run there are no expected returns from currencies.

We think that is a sensible starting point, but we are also aware alternative choices could be plausible. In this case it is useful to think in terms of scenarios.

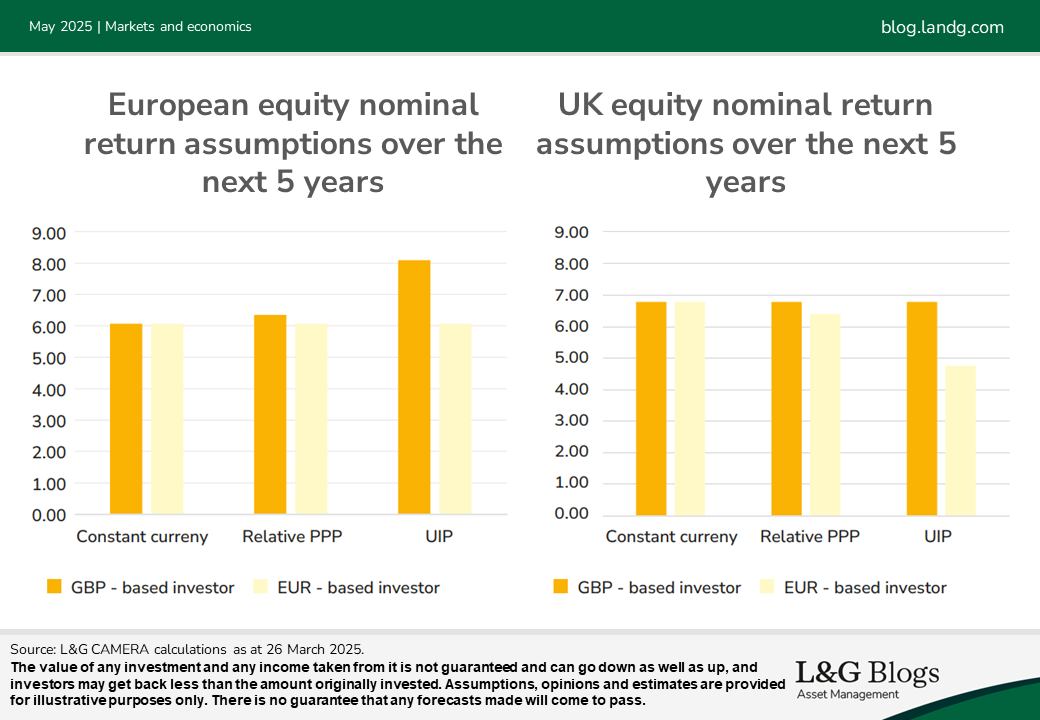

Currency scenarios

The charts below show UK and Europe (ex-UK) expected return assumptions in euros and GBP for different currency assumptions. This shows the expected return deviates by up to 2% (reflecting the interest rate differential) depending upon your return assumption.

What does it mean?

We present CAMERA estimates with the assumptions we think are most sensible. Indeed, relative PPP sits between two of the reasonable alternatives. But where there are uncertain choices, it is good to know how sensitive our assumptions are to those choices.

For example, euro-based investors should be aware that if they are assuming constant currency in their assumptions, they could be biasing international equity return assumptions upward.

The article above is an extract from our Q2 2025 Asset Allocation outlook.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.