Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

BoE gets closer to cutting rates

A surprisingly dovish vote suggests the Bank of England will begin its interest-rate descent sooner rather than later.

At Thursday’s March Monetary Policy Committee (MPC) meeting, the Bank of England (BoE) voted 0-8-1 to keep rates unchanged (hikes-unchanged-cuts). This compares to a 2-6-1 vote last month.

Consensus was split down the middle between 1-7-1 and 2-6-1, so it’s a dovish surprise that both hawks switched their vote to ‘unchanged’. The MPC continues to downplay base effects (from energy price movements), instead reiterating its focus on inflation persistence (i.e. labour costs and services inflation).

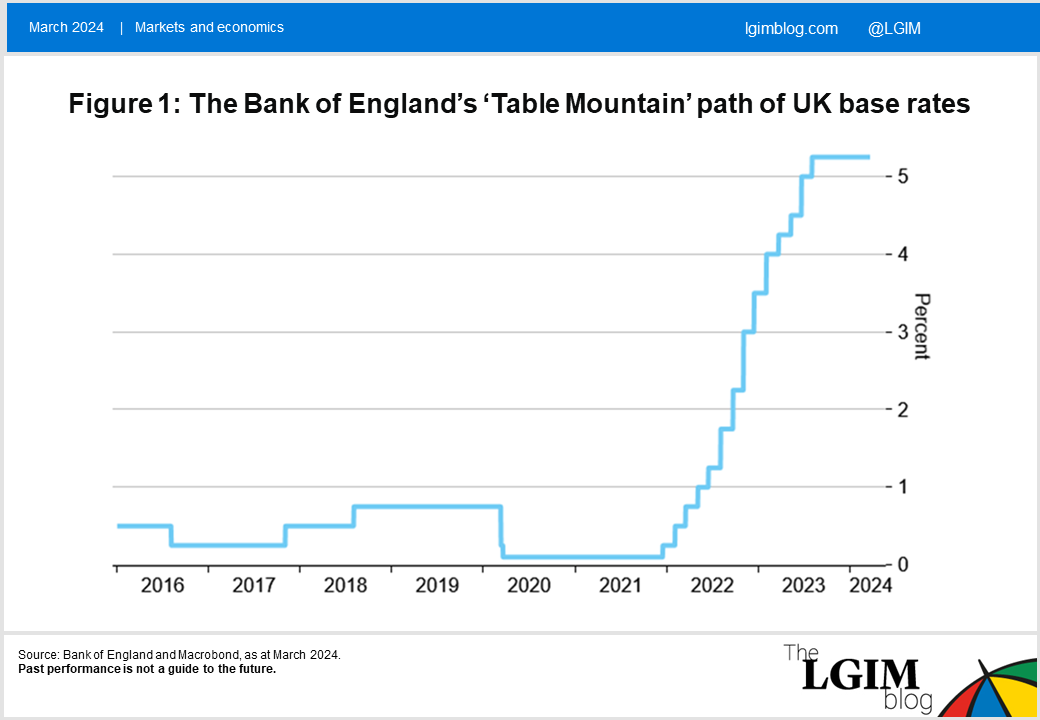

In our view, the Bank of England is uncomfortable being on top of ‘Table Mountain’ (Figure 1). Its February Monetary Policy Report saw inflation falling below target if rates are kept at 5.25% forever. But it’s also wants to climb down cautiously. In ‘financial speak’ that means it wants confirmation that services and wage inflation are moderating.

At February’s press briefing, the BoE had flagged ‘ex-energy’ inflation as the key metric it is monitoring, and at the latest meeting the Bank continued to hint it won’t get too excited by below-target headline inflation as energy costs fall over the spring if other measures remain sticky.

However, in a more dovish move, it also noted that policy can remain restrictive even if the Bank Rate was cut, given its high starting level. The Agents’ Survey pointed to only a slight improvement in near-term activity, with optimism about the future reflecting hopes of rate cuts.

We agree with the market pricing directly after the decision that the May press conference is too early to cut rates given we won’t have the crucial April inflation data when:

- Many services prices reset

- Headline inflation is expected to fall below the psychologically important 2% level

Before the March meeting, markets believed that both June and August were equally likely. The June meeting will have the key April CPI data, whereas August will be a press conference.

We think the MPC prefers press conferences to explain ‘bad news’ hikes more than ‘good news’ cuts, though it could still want to wait for a Monetary Policy Report month to:

- Thoroughly review the data

- Explain a ‘cautious cut’ to the press to contain inflation expectations (i.e. “we’re still worried about high services inflation so don’t get carried away expecting too many more cuts”)

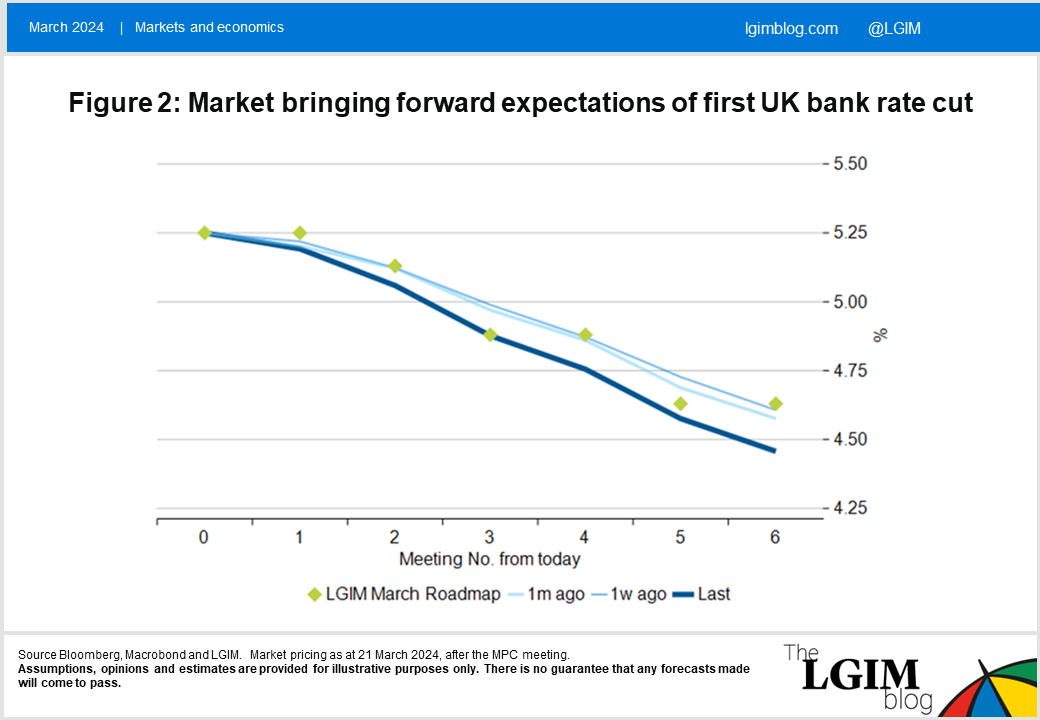

Thursday’s dovish vote split has encouraged markets to price in a June move (Figure 2), with markets seeing a 78% chance of a June cut after the meeting versus a 50:50 chance at the start of the week.

So the descent from Table Mountain could be getting closer. It’s nearly time to lace up those boots…

Closing our overweight gilts trade

We have been overweight 10-year gilts versus bunds since early February, largely based on scepticism that the ‘sticky inflation’ narrative in the UK was sustainable. In the meantime, we have had two UK CPI reports with a downside surprise in both.

As discussed above, the more hawkish elements of the MPC have now dropped their calls for higher rates. In addition, the UK budget has been and gone with only marginally additional fiscal loosening. As a result, we think the narrative for the relative trade versus bunds has now played out with pricing of rate cuts for June almost identical across the UK, Europe and also the US, and have closed out this trade accordingly.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.