Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Autumn Statement surprise?

The Chancellor delivered a modest surprise last week, using increased fiscal headroom to deliver more giveaways than expected. Where has the extra headroom come from, and what are the implications for gilt markets?

The scale of Jeremy Hunt’s fiscal giveaways at his recent Autumn Statement was greater than many expected. While there was an expectation in the market that the government would keep some of the improved fiscal position as dry powder for pre-election giveaways in the spring Budget, the Chancellor decided to spend almost all of it.

Increased fiscal headroom

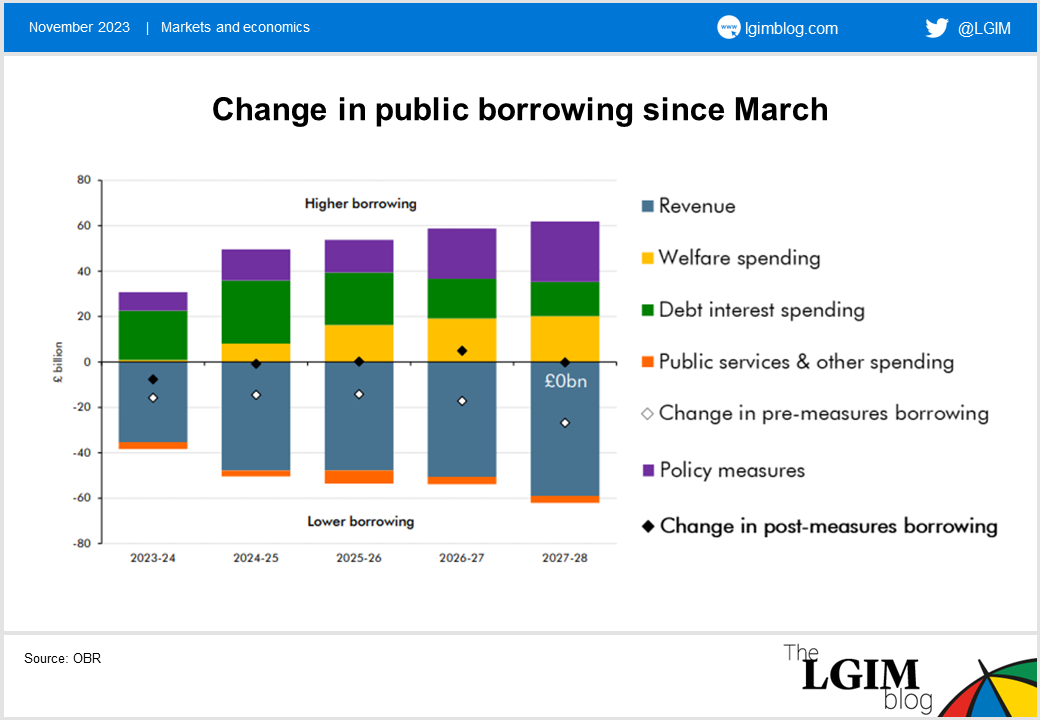

In its pre-measures forecast, the Office for Budget Responsibility (OBR) almost quintupled the fiscal headroom (the buffer before breaking fiscal rules), from £6.5bn in their March forecast to £30.9bn. The windfall is mainly due to underlying forecast changes, reflecting the impact of higher inflation that pushes up tax receipts, while departmental spending is unchanged in nominal terms and therefore lower in real terms.

The Chancellor decided to spend the improvement mainly on tax cuts. The main policy announcements were the two percentage point cut to National Insurance Contributions, starting in January and, as widely expected, the full expensing investment tax relief has been made permanent. The measures mean that headroom at the end of the forecast period is only increased to £13.5bn and the change in public borrowing is almost zero as can be seen in the chart below.

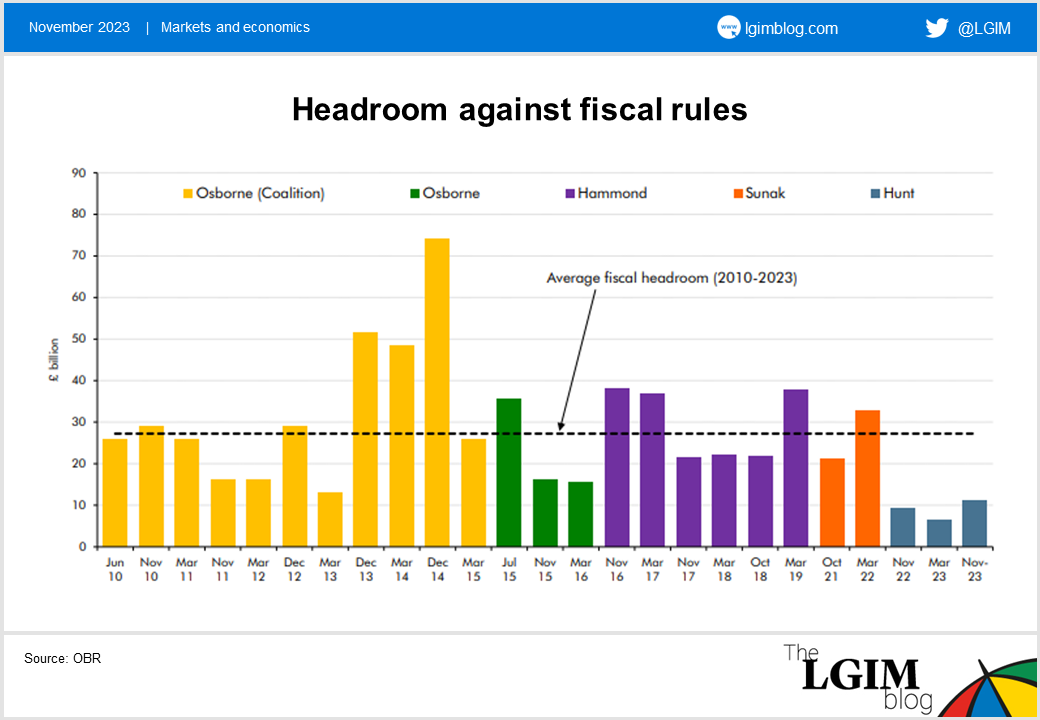

Even though the headroom has increased, it is still relatively low by historical standards and doesn’t leave much room for further easing in our view unless the outlook for the economy improves (see chart below for historical headroom). That said, we believe that this was within the bounds of fiscal responsibility and demonstrated economic competence. We expect the policy changes could add roughly 0.2% to growth and for the impact on inflation to be relatively small.

Gilt market reaction

For the gilt market, the main focus has been on the revision to the gilt remit that the Debt Management Office (DMO) published alongside the Autumn Statement. There were expectations for a cut in gilt issuance of c.£14bn according to a Bloomberg poll ahead of the event, but in reality the DMO only reduced issuance by a mere £0.5bn, while UK treasury bills were reduced by £10bn.

In addition, some of the unallocated supply has been re-allocated to auctions and syndications, and the DMO has added three additional auctions to their calendar (medium- and long-dated conventional gilts in December and an index-linked gilt in January). On top of that, the medium-term outlook for gilt supply also worsened, as the DMO's Illustrative Gross Financing Requirement (IGFR) projections increased by £78bn over the next four years.

The market reaction was a reduction in the pricing of long-dated gilts, both relative to swaps and on the curve. We expect that the elevated gilt issuance and the related question of “who buys all the gilts” will continue to occupy the minds of investors and the DMO.

A budgetary contrast to Germany

While the UK government is cutting taxes to support the economy, we're seeing the opposite in Germany, where budget challenges appear to be developing. Germany has a constitutional ‘debt brake’ (balanced budget) law but has been able to get around this by reallocating special funds raised during emergencies, in particular the covid crisis of 2020.

The constitutional court has ruled this is illegal – particularly for its ongoing climate infrastructure fund. The situation remains fluid but there's concern aplenty in Berlin with estimates of a fiscal tightening of between 0.4% and 1% of GDP needed to balance the books.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.