Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

All bonds are equal, but some are more equal than others

Which duration assets should investors own? It depends on the underlying motivation for holding duration.

The following is an extract from our Q4 2025 Asset Allocation outlook.

Duration risk, defined as the sensitivity of portfolio returns to changes in risk-free interest rates, is embedded in almost any portfolio.

For some assets, it is explicit. Fixed income securities (bills, bonds, loans, asset-backed securities) reprice directly when government bond yields change.

For some assets, it is implicit. Securities with variable cashflows (notably equities) are sensitive to changes in government bond yields because they impact the discount rates applied to those cashflows. For assets with no cashflows (notably commodities and digital assets), changes in government bond yields impact the price through their effect on the opportunity costs associated with investment.

Thinking about it from first principles helps us to consider why (and where) to hold that duration risk. When crafting a portfolio, we should aim to eliminate unrewarded risk and diversify rewarded risks.

Duration for risk reduction

If you think that duration risk is unrewarded, it only makes sense to hold if it reduces risk (putting aside arguments about liability-hedging or reinvestment risk). That is more likely to be the case when the markets fret about the growth outlook and is less likely to be true when fiscal or inflation concerns dominate.

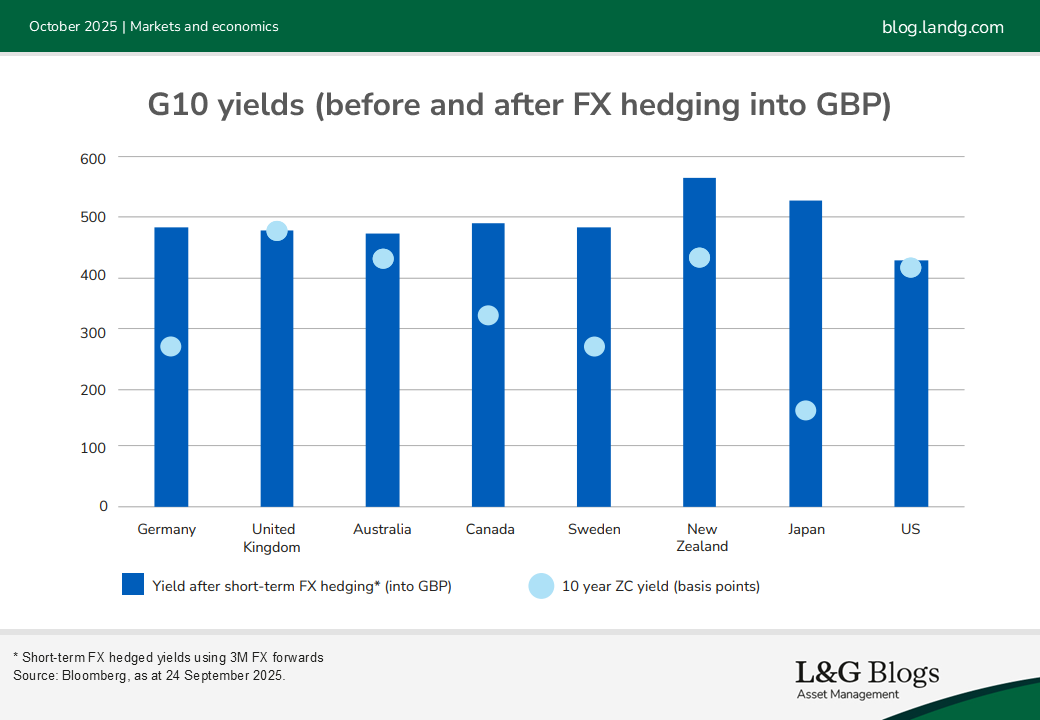

In the current environment, we think these arguments point to taking duration risk in slightly unusual places. Australia has very little debt by international standards, with net debt at just 30% of GDP, and continues to enjoy AAA ratings. The British/ French/US/Japanese concerns about unsustainable fiscal deficits simply don’t apply, but nonetheless they pay some of the highest yields in the developed world.

If you want to hold duration for protection purposes, you can do a lot worse than looking down under.

Duration for returns

But, if you think that duration risk is rewarded, then you should be looking for the markets where government bonds are likely to deliver a return over cash when held to maturity. Academics refer to a “positive term premium” when that condition is met.

The historical data suggests that positive term premia are more likely when yield curves are steep or when government yields are meaningfully above equivalent maturity interest rate swaps. Those conditions are currently met in Japan and the long end of the gilt market. It’s no coincidence that those are the markets where questions are being raised about fiscal sustainability.

All else equal, where investors worry most about fiscal risks the reward for bearing that risk is likely to be highest.

Horses for courses

So, we’re left with a bit of a conundrum: either avoid the markets where fiscal risks are greatest or actively seek them out, depending on your motives. That might sound twofaced, but it raises the prospect of different strategies being appropriate for different investors.

For low-risk portfolios, there’s a good case for allocating more to those government bonds which now compete with investment-grade rate credit.

But for portfolios where growth risks dominate, the incentive to allocate to the more fiscally prudent sovereigns is likely to dominate.

Read our Q4 2025 Asset Allocation outlook.

It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.