Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

After February’s purge, will markets surge?

Risk assets repriced last month on higher policy rates expectations. But did the decline capture the full implications of tighter policy, or are investors missing the bigger picture?

![]()

February is named after the Latin verb februa, meaning to purge, purify or cleanse. It seems that the Romans were quite keen on some early spring cleaning in their annual Februalia festival.

This February, financial markets were somewhat ‘purged’ of their excessive optimism about immaculate disinflation. Since the start of the month, markets added 50-60 basis points (bps) to their outlook for UK and European policy rates at year end, and a whopping 85bps in the US. That reappraisal of central banks has come alongside firmer jobs, inflation and confidence data.

That’s been bad news for anyone with a mortgage coming up for refinancing, anyone investing in the front end of fixed income markets, and anyone hoping for a rapid easing of financial conditions.

It’s also had a purgative effect on global equities, commodities, treasuries and credit. These markets were all down over the month in a dynamic that is worryingly reminiscent of last year.

Time for a fresh start?

But has it also cleansed and purified the outlook? The risk-asset repricing on higher policy rates has not been as severe as that seen in 2022.

Plausibly, that’s because there is now less shock value: what’s another 25bp on policy rates between friends when central banks have been hiking interest rates in clips of 50-100bps at a time?

The positive spin would be that the market now has a more balanced outlook of inflation and interest rates, raising the bar for more bad news. The more worrying interpretation is that investors have become complacent about the impact of tightening financial conditions on the growth outlook.

Patience is a virtue

Market participants tend to be an impatient crowd. There is only so long that we can be told “a recession is around the corner” before we start to wonder if it will ever come. Despite having been schooled in the ‘long and variable lags’ of monetary policy, we’re all now looking for the near-instant validation of the bearish cyclical outlook.

As Camilla Ayling in LGIM’s Equities team lays out in her blog post, the recent earnings season failed to provide much evidence of that inflection.

Within the Asset Allocation team, we worry that the purge has further to run, and we stay underweight in both equities and credit, but that shouldn’t be mistaken for a permanently bearish outlook.

What would we need to see to become more structurally upbeat? On the fundamental side, we’d need to see developments which genuinely extended the cycle: improving productivity growth and/or immaculate disinflation are two candidates for that, but neither appear especially likely.

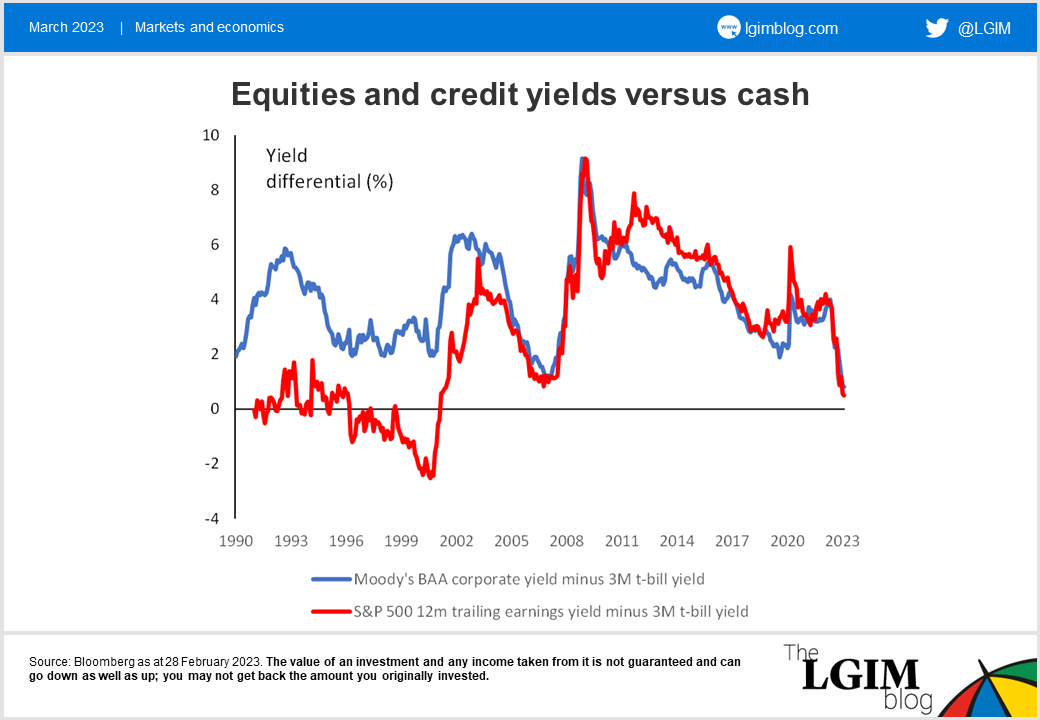

Most likely, we would need to see a valuation improvement in both asset classes. As things stand, the yields available on short-dated government debt are now comparable with both the earnings yield on US equities and the yield to maturity on BAA-rated corporate credit as shown in the charts below. In both cases, that is the tightest yield differential since before the financial crisis.

Februalia was not only a festival of spring cleaning, but also of purging of the fields by clearing away the winter’s debris ready for the new season. In financial markets, there’s currently not much of a valuation buffer to provide compensation for risk.

A reset of those valuations is still needed, in our view, to provide fertile ground for investors.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.