Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

A sector approach: UK real estate in 2025

With January’s bond yield-led volatility calming down, we take stock of real estate as an asset class, looking at which sub-sectors might be of interest to investors in the year ahead.

A lot of annual outlooks are published in the closing weeks of December, across many asset classes. Real estate is no exception. Fortunately for us we didn't release anything formal covering the asset class on a standalone basis as the year ended. If we had, it may have seemed outdated quickly as global government bond yields experienced another significant bout of volatility in the opening weeks of January.

Luckily, stability appears to have returned allowing us to take stock and see if our UK real estate expectations have changed.

Over 2024 we published various pieces highlighting our view that UK real estate was increasingly looking fair value following pricing adjustment with expected returns improving. This wasn't just predicated on the risk-free rate. More than one thing explains a property yield and its relative position to other asset classes – we also observed gradually strengthening rental growth expectations, for instance. Although these were still modest on a long-term horizon, they were supportive to yields and offered investors real-terms growth.

Modelled yields began to look lower than actual yields in Q1 2024, suggesting to us a buying signal. Applying the peak government bond yield seen in the early weeks of January to this model and holding all else equal would have challenged this assumption. However, we believe relative recent stability has mitigated much of this risk. This experience helps us re-emphasise three things:

1. Real estate still looks like fair value, but not fantastic value

2. Performance is most likely to be driven by income and income growth, not yield compression

3. Market interest rates appear hyper-sensitive, and we can expect them to remain so. This increases the value of looking ‘through the cycle’ at longer-term signals and structural trends

We also observe that, although segments in living and industrial sectors still look compelling with above average rental growth expectations on top of reset yields, higher-yielding sectors such as those within retail and hospitality - and in some cases offices - are beginning to look interesting relative to the property average. We therefore now see greater nuance between ‘growth’ and ‘income’ sectors.

We should be aware of different underwriting requirements. For instance, growth sectors require addressing whether their relatively lower yields are justified by convictional growth prospects. Whereas, for higher-yielding sectors, depreciation and running costs need to be properly scrutinised as factors which could quickly evaporate seemingly attractive returns.

Alongside this, we also contemplate risk styles. Operational assets offer investors a chance to grow income ahead of inflation. We still expect this to be the case and particularly like operational hotels and self-storage. At the other end of the ‘income barbell’ is long income. Long income funds were severely affected in 2022 due to their sensitivity to interest rates, with a peak-to-trough reduction in value higher than the all-property average. Yields since have been stable and insulated from recent volatility by their higher starting point. For a sector that offers inflation-linked growth (RPI inflation is expected to be in the region of 4% per annum over the next five years, according to rate curves) this looks to be good value, in our view, especially considering assets tend to be newer and more sustainable than average.

Meanwhile, the case for real estate debt remains. With banks reducing their share of commercial real estate lending the financing gap is growing. Institutions’ ability to align long-term liabilities with real estate debt income streams positions them well, in our view. A forthcoming report puts the commercial real estate exposure (including loans and debt securities) of insurance companies at over £140bn[1], supported by growing debt exposures while the value of equity holdings fell over 2022-2023.

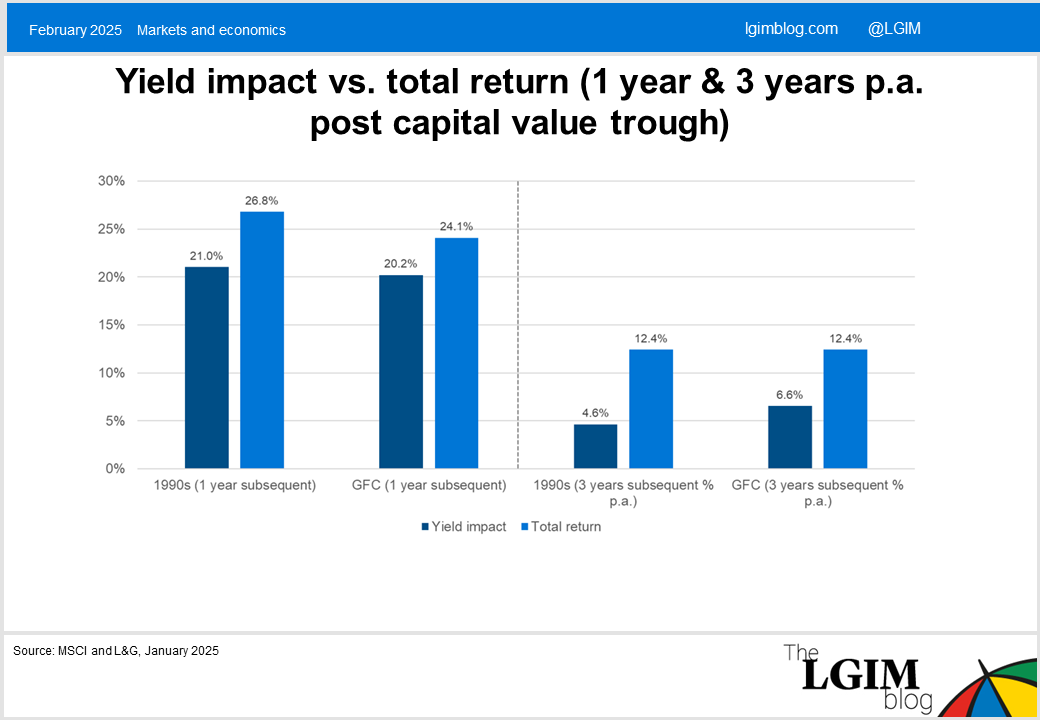

We cannot be certain about how rates will progress from here, but we are more convictional about the sectors that will offer better long-term risk-adjusted returns under various scenarios. We continue to advise against the hope value attached to inward real estate yield movement: yield compression seems unlikely to benefit the all-property average based on macro drivers.

This is different from previous cycles. Many observers had made the point that returns tend to be elevated after a correction - in the order of 10 to 20+% p.a.. For this cycle, in the absence of material yield compression, returns are likely to be more modest.

To outperform in an era of good but not great returns, the emphasis on segment allocation and asset selection is magnified. Fund managers who have already tilted away from traditional benchmark weightings to the ‘right’ segments within ‘beds and sheds’[2] will be well placed to continue to deliver superior returns, in our view, especially with innovative approaches to income risk from portfolios that offer both operational exposures and long income resilience. There is now, however, a growing case for higher-yielding sectors when those yields are defendable[3] as income increasingly complements growth across portfolios.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

[1] IPF, Size and Structure of UK Property, February 2025

[2] Within industrial strongest return expectations are for London & South East multilet industrial estates and urban logistics. Within broadly strong expected performance for the living sector, we highlight as offering compelling returns and income diversification within the sector.

[3] Retail warehouses and city offices stand out on this basis, in our view.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.