Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

A new era dawns

Our longstanding thesis of a market vulnerable to shocks has been confirmed, allowing us to take profits on several dynamic positions.

The article below is an extract from our Q2 2025 Asset Allocation outlook.

Markets have been a rollercoaster ride. The S&P 500 was down 20% from its recent peak to 8 April. But then President Trump announced a pause in the higher reciprocal tariffs, and the index rallied over 8% on the day and more than 11% intraday peak to trough, before selling off again[1]. The speed of the market correction, which happened in just a few days, is seldom seen.

I have seen a selloff like this only twice during my career: the global financial crisis and COVID-19 (I was just starting at university when the 1987 crash happened). Importantly, US equities have greatly underperformed the European markets.

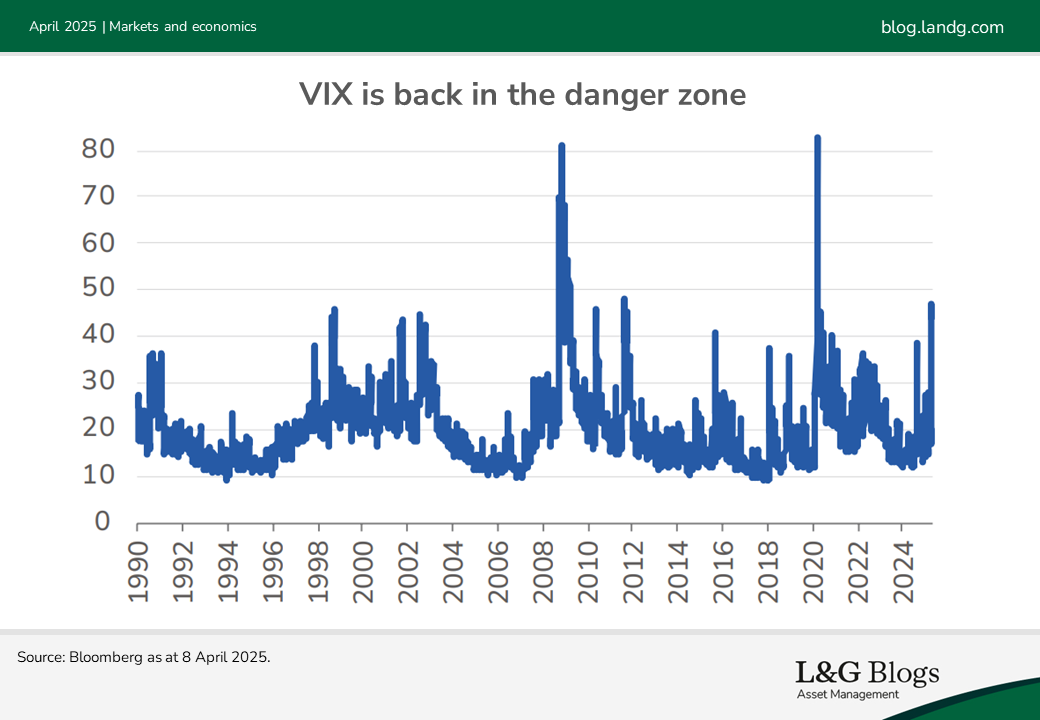

There are always multiple drivers in any market, but given the timing of the start of the correction it is fair to say that ‘Liberation Day’ tariffs and uncertainty around these policies made investors extremely nervous. The VIX, the market’s best [1] known fear indicator, rose to around 50 in early April – a level that has previously only been reached in periods of severe risk aversion.

Case confirmed We believe this selloff is a clear expression of our thesis that the market was vulnerable going into this. A soft landing was priced, and investors collectively believed that US exceptionalism would continue in 2025.

A broadly held consensus makes the market vulnerable, and given this, our multi-asset portfolios were cautiously positioned from a dynamic perspective. At the end of February, we sold our long equity position to neutral. That trade made our portfolios overall underweight risky assets, given our longstanding short position in credit risk and our long duration position, which we see as a diversifier during recessions.

As part of our investment beliefs we are also much more diversified in our long-term strategic allocation, with less US equities and more alternatives and duration than most of our competitors, who usually follow market cap indices.

Recent falls in US equities follow the worst quarter of relative performance of US stocks versus the rest of the world since 2002. Of course, it’s too early to tell if these market moves spell the end of US exceptionalism. But US equities did start the year as investors’ favourite asset class, so some of the recent price action probably represents a clearing of very skewed investor positioning and relatively high starting valuations.

What’s the economic impact?

Tim Drayson was warning of the potential strong negative impact of tariffs months before 2 April.

Although recession probability forecasts had risen in recent weeks, we believe they are now likely to be revised even higher, and recession is our base case at this point.

The headwinds to growth from trade disruption, uncertainty and reduced confidence could all potentially combine to have a much larger impact than that suggested by estimates based on the direct cost of tariffs alone.

Avoiding a US recession is now our alternative upside scenario, and could be achieved by a combination of tariff rollbacks, a limited response from trading partners, or domestic US fiscal stimulus that is passed quickly enough to mitigate the impact of the tariffs.

What are we doing in portfolios?

In the Asset Allocation team, we believe diversification [2] can help to act as risk management by design, ensuring we are not overly exposed to any one asset class, region or economic scenario. While in the past we have adjusted strategic asset allocations of the back of significant macro regime change (for example, post-Brexit), we don’t see the uncertainty around future US policy as meeting the threshold for targeted changes yet.

Part of our more diversified approach extends to equity allocations, where we typically have a lower strategic allocation to US equities than concentrated market cap indices. The recent divergence in performance away from the US has therefore acted as a natural relative tailwind for our approach this year, though it follows a long period of US outperformance.

As mentioned, for portfolios with more dynamic positioning, we were positioned with a cautious bias ahead of the announcements. This was expressed with a negative view on credit, a positive view on sovereign bonds and a neutral view on equities. With credit spreads at historically tight levels earlier this year, we saw the return potential from the asset class as asymmetric, with little upside potential and more significant losses possible in risk-off scenarios.

In currency markets, we have been leaning against the strong US dollar narrative for several months, with a continued preference for the Canadian dollar and Mexican peso. At the start of the year, there was much love for the US dollar that we simply did not share.

In the immediate aftermath of the tariff announcement, when there was significant market stress, we took profit on several dynamic positions. First, with the brief rally in bonds around ‘Liberation Day’ we took profit on some of our government bond positions, our medium-term overweight in duration. Second, we have bought equities to take profit on our underweight risk assets, bringing us back to neutral. We are using equities for this move as they are the most liquid instrument, instead of buying back our underweight credits.

Following the market correction, we have seen a dramatic change in consensus expectations towards our recession view and extreme stress. This provides grounds for us to start buying the dips. To be clear, a full recession is not yet priced (35% equity correction would be required), but we think a more than 20% correction is enough to start building a long risk position. We expect to do this in three areas: buy more equities, close our credit underweight and possibly sell government bonds and build an underweight duration position.

Aiming to deliver long-term value

While the market landscape is shifting, we believe our diversified approach and strategic positioning could provide a robust framework to navigate the uncertainties.

We are committed to managing portfolios that aim to be well positioned for potential opportunities, regardless of the prevailing economic conditions.

As always, our focus remains on aiming to deliver long-term value for our investors through careful management and strategic agility.

Thinking, wide and deep

Our articles in this publication reflect the breadth of our thinking, and I am sure you will find plenty of food for thought in the coming pages. Start with Tim’s detailed analysis of US tariffs, which will no doubt dictate the market mood in the months ahead.

Elsewhere, Rob Griffiths and Simon Bell revisit the prospects for the Magnificent Seven, US small caps and European equities following the European renaissance since the start of the year.

John Southall, meanwhile, turns his quantitative expertise to the subject of private markets, using a modelling framework to determine what level of allocation might be appropriate based on an investor’s circumstances, beliefs and risk appetite.

Finally, our regular CAMERA update will provide a summary of our long-term return expectations across a range of asset classes.

The article above is an extract from our Q2 2025 Asset Allocation outlook.

Key risk

The value of any investment and any income taken from it is not guaranteed and can go down as well as up, and investors may get back less than the amount originally invested. Assumptions, opinions and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

[1] Source: Bloomberg as at 10 April 2025.

[2] It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.