Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Why diversification is key to a resilient portfolio

In the first of a series on overcoming equity market concentration risk, we consider alternatives to a traditional portfolio, and provide a practical guide to dealing with market volatility.

A year and a half ago we wrote a blog flagging equity market concentration as a potentially overlooked source of risk in portfolios – today that risk is at the forefront of many investors’ minds. In the final quarter of last year, equity market concentration hit an all-time high, with the weighting of the top 10 stocks in a widely followed global index hitting 28%, and it remains high at 25% as at the end of May.[1]

With market volatility elevated, it seems fitting to revisit our original blog, and to consider how investors might look to diversify their portfolios.

Over the past decade, the weighting of the IT sector in widely followed indices has approximately doubled.[2] This means the performance of a handful of giant companies (such as the ‘Magnificent Seven’[3]) can have a huge impact on the overall return from what may appear to be a diversified core holding.

An Achilles’ heel?

In years past, attention was focused on the outsized positive contribution from the Magnificent Seven. But this year attention has shifted to the impact of falls in mega-cap tech stocks on market-cap indices.

At the start of the year Chinese tech company DeepSeek unnerved investors by releasing a large-language model that was apparently built far more cheaply than its Western predecessors. This called into question the longer-term outlook for companies such as Nvidia*, whose valuation is underpinned by expectations of continued demand for its AI chips.

More recently, ongoing uncertainty around US tariffs has led to price swings for tech giants, along with some idiosyncratic risks such as Nvidia announcing the launch of a cheaper H20 AI chip for China.

Overall, the challenge for investors is clear: amid heightened volatility, what can be done to overcome the risks inherent in a concentrated equity market?

Beyond 60-40

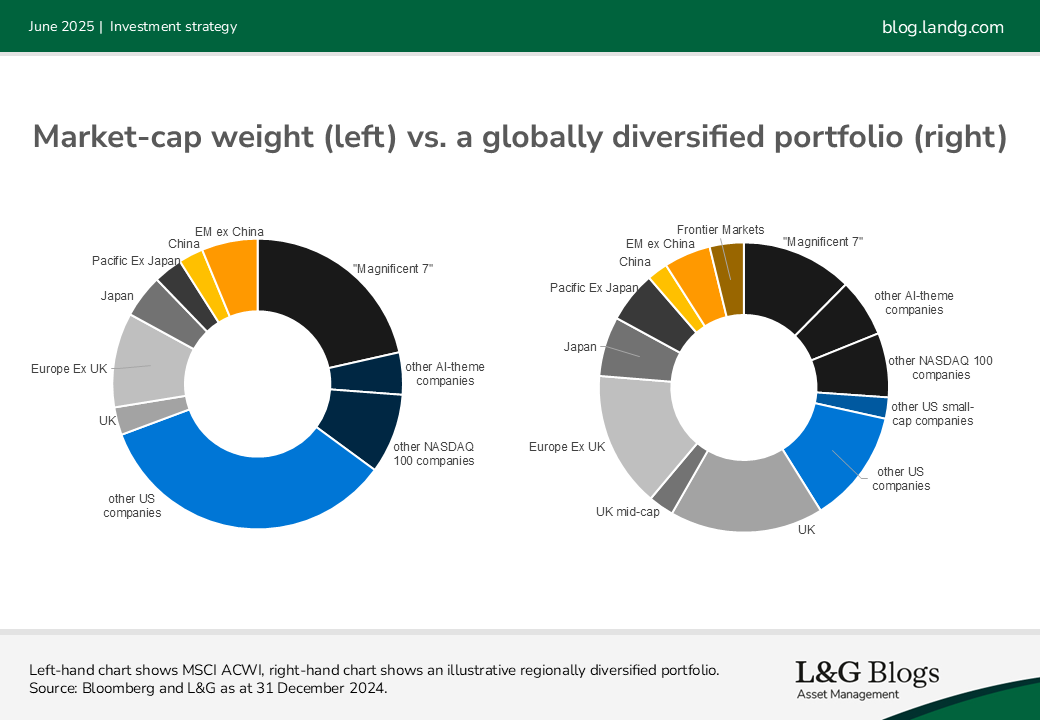

The graphs below show how a traditional 60-40 portfolio, made up of a market-cap weighted equity index combined with a global aggregate bond index, compares with a regionally diversified** approach.

As you can see, on the equity side a regionally diversified approach has resulted in a lower concentration risk in the Magnificent Seven while still providing a meaningful allocation to high-growth equities through a combination of AI-themed companies and other NASDAQ 100 stocks. As well as being over-represented in market-cap weighted indices, these stocks could also feature in active funds given widespread excitement around the potential of AI.[4] This ‘duplication risk’ across index and active holdings may further increase concentration risk.

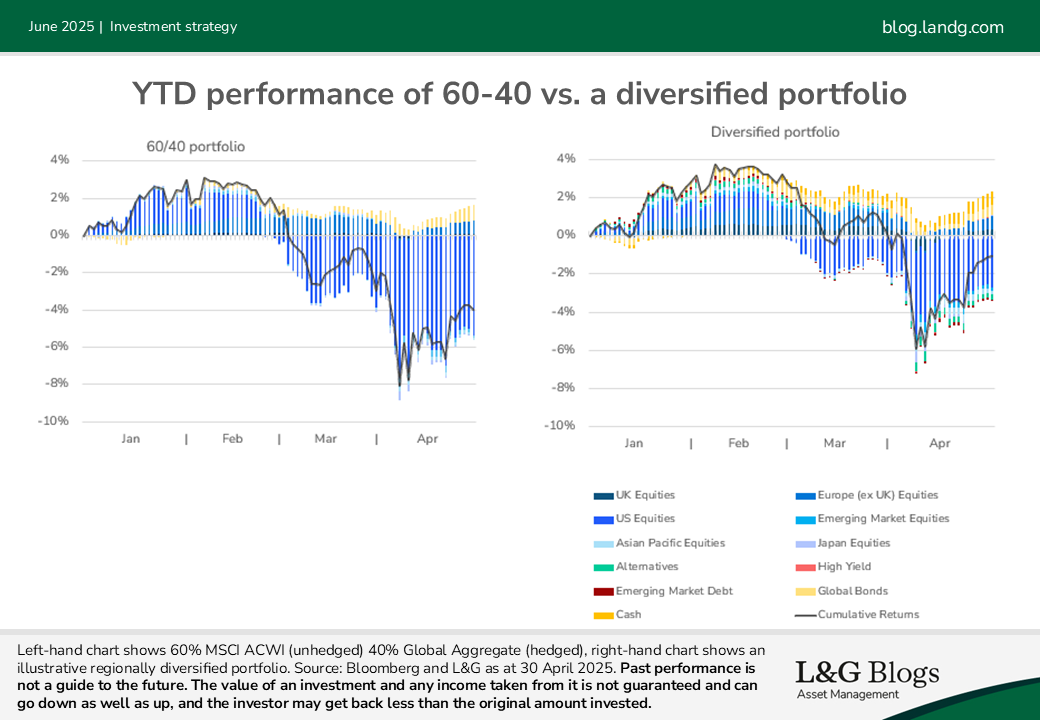

In the year to date, regional diversification has been beneficial for investors, allowing them to capture strong equity market returns from Europe and Japan.[5] This has resulted in better overall returns relative to a traditional 60/40 portfolio, as well as lower maximum drawdowns from a diversified portfolio, as shown in the chart below.

Note that black line tracks the cumulative returns between the start of the year and the end of April, and the coloured bars show the cumulative contribution from individual asset classes.

A roadmap for uncertainty

Ultimately, it is impossible to predict exactly how things might look in 24 hours, never mind over a 20-year investment horizon. However, to help steer the ship through volatile times, there are some simple principles we believe stand the test of time:

- Diversify: With so much geopolitical uncertainty, don't overexpose your portfolio to any specific region, sector or stock.

- Prepare, don't predict: Trying to accurately predict long-term outcomes at inflection points is impossible. Don't overcomplicate it. Build a portfolio that performs in a variety of different environments.

- Think long term: Avoid the short-term noise and remain invested. Achieving long-term returns requires consistent market exposure, even in difficult markets.

- Take your time: Act gradually and follow a robust and explicit process to limit behavioural biases, which are accentuated in trickier times with 24-hour news.

Diversification, in all its forms

In this blog we’ve explained the value we see in a regionally diversified approach. But the market offers many possible diversification tools.

In the next installment of this series, we’ll examine sectors in detail, to show how defensive sectors have offered refuge to investors during recent selloffs. We’ll also show how investors can aim to capture the upside of exciting sectors such as AI in a diversified fashion – something that we feel is particularly important in parts of the market that are developing at unprecedented pace.

Finally, we’ll turn to factors, exploring how this academically established approach to identifying persistent sources of returns could offer an alternative to market-cap weighting schemes.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

** It should be noted that diversification is no guarantee against a loss in a declining market.

[1] Source: MSCI World index via Bloomberg.

[2] Statistics for S&P 500 index. Source: Bloomberg data using ETFs as a proxy of index compositions, as of 02 October 2023.

[3] This refers to Google parent company Alphabet, Amazon, Apple, Meta (formerly Facebook), Microsoft, Nvidia and Tesla.

[4] Holdings of Nvidia as at the end of 2024 provide an illustrative example. M* data shows of 252 funds in the IA North America Sector, c. 95 don't hold the stock, c. 87 are market weight or overweight, and c. 70 are underweight vs the S&P 500.

[5] As at 26 May 2025 European equities are up 10.8% year to date in EUR terms, while Japanese equities are up 8.7% in USD terms.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.