Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Why concentration risk matters now – and how equal weight could provide a solution

History has shown time and time again that concentration risk can lead to painful drawdowns during periods of volatility. A different approach to index weighting could help.

In recent articles, we have explored why diversification* is key to building resilient portfolios, how real assets can support portfolio balance, and what investors can learn from unexpected market events like the Section 899 tax debate.

A common thread across all these is the importance of managing risk thoughtfully, especially in today’s market environment, where a small number of stocks wield arguably disproportionate influence over major indices like the S&P 500.

This blog takes a closer look at index concentration risk, and more specifically, how elevated levels of stock concentration in the S&P 500 have historically coincided with deeper market drawdowns.

Examining key historical periods, we’ll show how diversification has reduced the likelihood of downside shocks and mitigated the severity of those shocks when they occur.

Dot-com bubble (1999–2002)

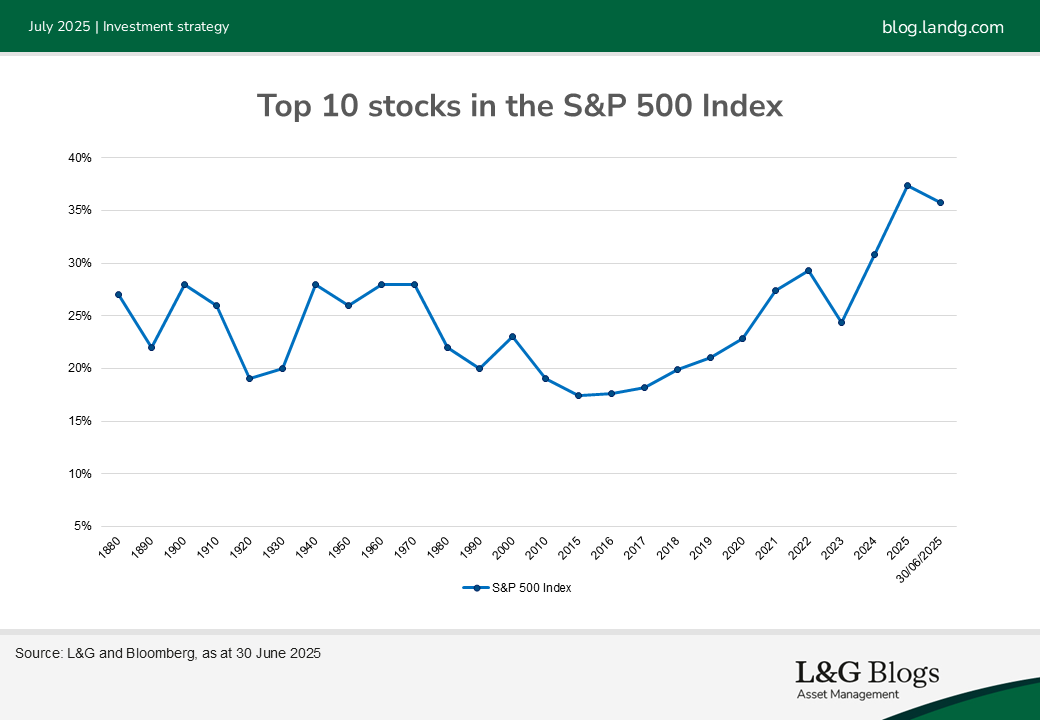

As the internet boom gripped the late 1990s, technology stocks dominated the S&P 500. By March 2000, the top 10 companies represented nearly 27%[1] of the index’s weight, a historically high level of concentration at the time. As investor enthusiasm peaked, valuations became unsustainably stretched.

When the bubble burst, the S&P 500 lost nearly 50% in value, while top tech names plunged even further, some by 80–90%.[2] This period clearly illustrates that when index weights become concentrated in one sector, corrections can be deep and prolonged. A more diversified index would have softened the impact significantly.

Global financial crisis (2007–2009)

In the period leading up to the 2008 crash, the S&P 500 became heavily skewed toward financial and real estate sectors, not tech. As financial institutions became dominant within the S&P 500, their vulnerability to the housing and credit market crash had a magnified effect on the overall index.

The result was catastrophic: the S&P 500 suffered a near 50% drawdown, as the collapse of major banks reverberated through the entire market.[3] The heavy weighting in financials amplified the damage; investors with more diversified exposures during this period typically experienced less severe losses and recovered more swiftly.

Tariff tempest (April 2025)

In April 2025, equity markets again saw a sharp pullback amid a shift to risk-off sentiment, this time driven by a correction in the mega-cap ‘Magnificent Seven’ tech names, which by then made up more than a third of the S&P 500’s market cap.[4]

The chart above shows that index concentration reached an all-time high, even surpassing dot-com era levels. As just a handful of large tech stocks corrected, the market as a whole suffered.[5]

This episode highlights the danger of relying too heavily on a small group of outperformers, particularly when valuations are stretched and volatility returns.

Equal weight indexing: a cure to concentration risk?

One of the most effective ways to mitigate concentration risk is through equal-weight indexing. Unlike market-cap weighted indices, which naturally provide further exposure to the largest companies, equal-weight indices assign the same weight to each constituent regardless of size, sector or country of domicile.

This approach inherently distributes exposure more evenly and limits the dominance of any single stock or sector. Equal-weight strategies can offer improved risk-adjusted returns, especially in market environments where leadership shifts or mega-cap stocks underperform.

Equal-weight indices don’t just spread risk, they also introduce systematic rebalancing, selling outperformers and adding to laggards each quarter. This contrarian approach can enhance long-term returns and reduce overexposure to overvalued names.

By investing in equal-weight versions of the S&P 500 or S&P 100, investors gain access to the same high-quality companies, without the outsized influence of a few dominant names. This makes equal-weight indexing a compelling core holding for long-term, risk-aware investors.

*It should be noted that diversification is no guarantee against a loss in a declining market.

[1] Source: Bloomberg.

[2] Sources: https://financhill.com/blog/investing/market-concentration-and-sp-500-performance and https://www.reuters.com/markets/us/us-stock-concentration-its-not-all-doom-gloom-mcgeever-2024-06-12/

[3] Source: Consequences of Concentration

[4] Source: Bloomberg.

[5] Sources: S&P 500 closes at a record, erasing last of pandemic losses | PBS News and Goldman Says Large Cap Concentration Bad Sign for Future Returns - Markets Insider

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.