Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

To repo better, you gotta be clever how you sow…

So far in 2021, the UK’s liability-driven investment (LDI) community has experienced a very attractive repo funding market, in which cash is lent in exchange for collateral.

As observers of this market will probably already be aware, the sub-12-month gilt repo funding spread over the equivalent SONIA swap rate has come down significantly to levels below 10 basis points, a multi-year low. Our colleague Nelly Terekhova elaborated on this movement recently.

However, it may be less commonly known that the Z-spread (i.e. the spread between the gilt yield and swap rate of an equivalent SONIA swap) of very short-dated conventional gilts has also reached a multi-year low over the same period. While such bonds are less commonly used as hedging instruments in an LDI strategy due to their relative richness compared with alternatives – such as swaps, credit investments, or interest-rate exposure from index-linked gilts in the same sector – we believe they can offer a lot of value from a different perspective, namely ‘nettable’ repo.

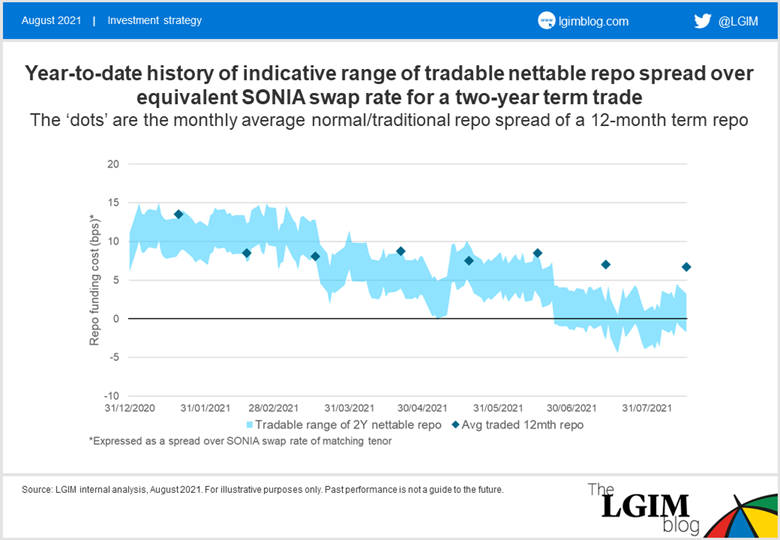

In the chart below, the blue band is the indicative year-to-date range of tradable levels of a two-year nettable repo, compared with that of a 12-month normal/traditional repo (the dark blue dots).

The level hovered about the breakeven point, where it was marginally advantageous to use nettable repos in the first half of the year, and has come inside significantly since July. This allowed us to transact and lock in two- to three-year term repo funding at a level around two basis points above the equivalent SONIA swap rate, which is a level last seen in 2017.

What is nettable repo?

Normal or traditional repo is a repurchase agreement whereby investors sell a security (most commonly a highly rated government bond) to a counterparty and agree to buy it back on a future date at an agreed price. This allows investors to release the capital locked in holding the security and raise cash, by paying a funding cost, i.e. repo interest. A reverse repo is the opposite: investors deposit money in exchange for a bond with an agreed future sell-back price.

Nettable repo is a package of repo transactions that involves simultaneously trading a normal or traditional repo on the gilt you want to hold in the portfolio (e.g. a long-dated index-linked gilt) as well as a reverse repo on a short-maturity gilt.

From a counterparty perspective, the funding position will net down to close to zero (hence the term nettable repo), so there is very little net loan or deposit between the two parties. Economically, the effective funding cost the investors will pay becomes the yield of the short bond plus a spread the counterparty charges to facilitate the trade.

Therefore, as short-dated conventional gilts become richer – i.e. have a lower Z-spread – the effective funding cost of a nettable repo will also come down.

What it takes to be clever…

While nettable repo is part of a standard toolkit for our LDI portfolio management, as an instrument itself it is not without challenges. Compared with normal or traditional repo, it is longer dated, more complex to transact and to process operationally, and very dependent on counterparty axes.

In order to manage these additional nuances, we have worked with counterparties to build a standardised approach, as well as developed a robust management framework that we believe allows portfolio managers to assess values holistically on an ongoing basis and manage client positions accordingly.

We continue to monitor this part of the market and focus our efforts on the most efficient strategies as and when they become available.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.