Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Surplus to requirements: rates and inflation hedging in the endgame

Amid the improvement in defined benefit scheme funding levels, a number of schemes are now finding themselves in surplus, even versus a buyout measure. How can schemes manage this position to best effect: should they hedge the buyout surplus or the funding level?

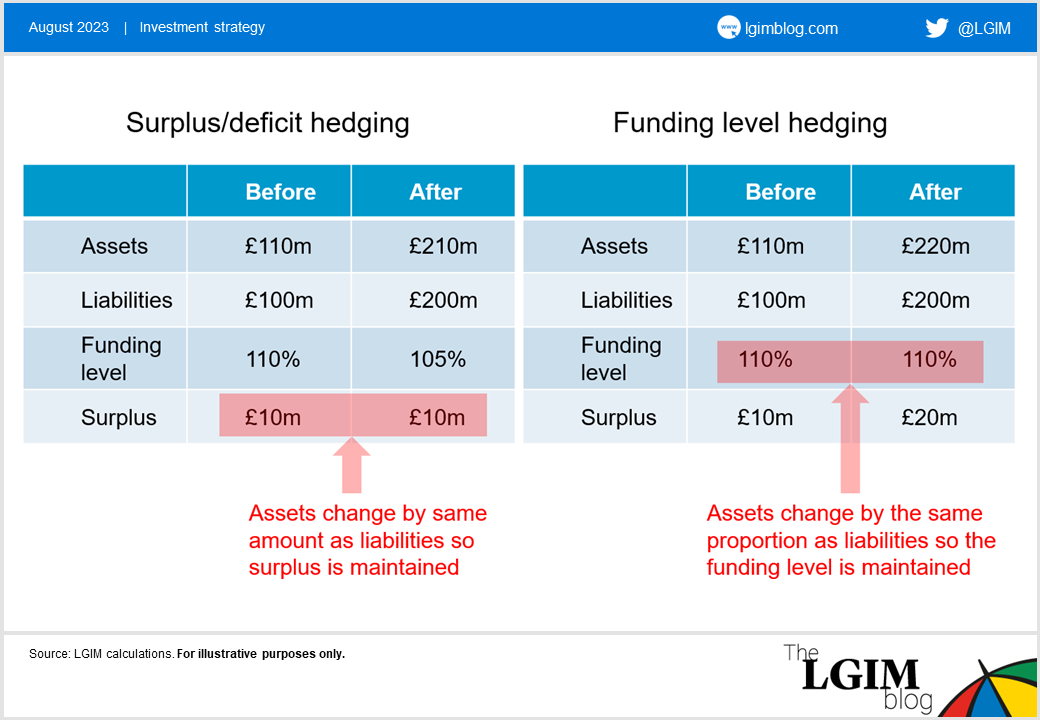

Up to now, the key question of liability hedging has been whether to hedge the funding level or the deficit of a scheme, depending on the trustee view of which is more important.

|

Hedging type |

Liability hedging target |

Immunises |

|

Funding level |

Funded value of scheme liabilities (i.e. the value of the assets) |

Changes in funding level due to moves in rates and inflation |

|

Deficit |

Total value of scheme liabilities |

Changes in deficit from moves in rates and inflation |

Improving funding levels – more than 100% funding levels and surpluses are becoming more common

Given the substantial increase in scheme funding positions over the last year, we estimate that the median scheme is close to full funding on a buyout basis (i.e. can afford to transfer scheme liabilities to an insurer under a risk transfer transaction), therefore, a significant number of schemes are running a material surplus on a buyout basis.

Whilst the theoretical aspects of liability hedging remain the same, the question for these schemes is now subtly but importantly different. Should these schemes hedge the buyout surplus or the funding level?

Hedging funding level or surplus?

Below we illustrate how the two approaches differ for an example scheme that starts off 110% funded on a buyout basis and where there is a large drop in (real) interest rates, causing liabilities to shoot up:

Stepping back – big picture

In making this decision it’s important to consider:

- How could a scheme surplus be used?

- How would the liability interest rate and inflation exposure vary under different approaches?

Whilst this is heavily scheme-specific and dependant on legal aspects such as a scheme’s own rules, a surplus may be able to be used in the following ways:

- Uplifting current DB member pensions in % terms

- Providing current DB members with a one-off lump sum

- Transferring surplus to the sponsor, with a potential use case being to better support DC pensions

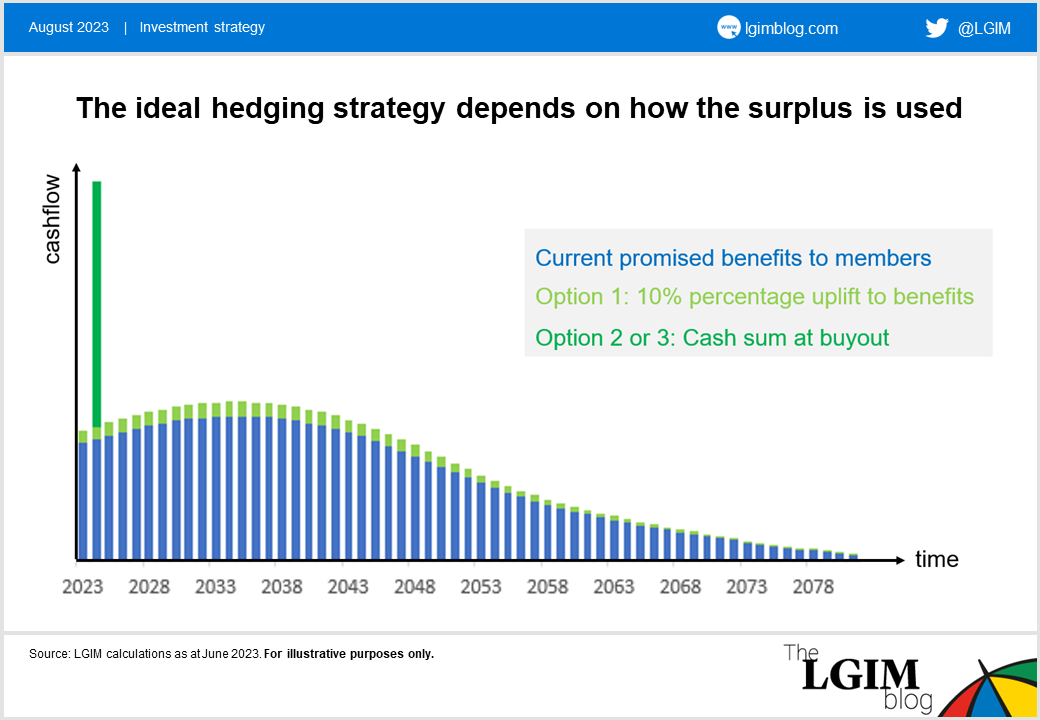

One way to consider when assessing how to hedge a scheme’s interest rate and inflation liabilities is using a cashflow chart. As in the example above, we assume the scheme could secure currently promised benefits for £100m with an insurer and the value of assets is £110m. Meaning there is a surplus of £10m and a funding level (on a buyout basis) of 110%.

In the below the blue bars signify the current promised benefits to members. The green bars then show how the surplus could be used.

The light green bars show the additional cashflows if there is a 10% percentage uplift to all benefits (Option 1 above). The dark green bars show the cashflows if the surplus is instead used to provide a £10m cash lump sum or is transferred out the scheme at the point of buyout (Options 2 or 3); we assume a buyout will happen relatively soon with the surplus extracted at the same time.

This could imply the following liability hedging approach:

|

Option |

Implied hedging target |

Rationale |

|

Option 1 |

110% of buy-out liabilities (£110m in exposure terms) |

The additional discretionary benefits would have interest rate and inflation exposure |

|

Option 2 or 3 |

100% of buy-out liabilities (£100m in exposure terms) |

Surplus would be a near-term obligation with little interest rate or inflation exposure |

If the surplus of the scheme were to be extracted more gradually, the dark green bar under options 2 and 3 would shift further into the future and could be more spread out. Under this scenario it could make sense to hedge somewhere between the value of liabilities and the assets i.e. do something between surplus and funding level hedging

Other factors

Whilst the decision around hedging level will be driven by potential use of a surplus, there are wider considerations such as:

- Uncertainty around the cost of a buyout (unless insurers have already been approached). This may favour hedging to funding level, as this target is less sensitive to assumptions around buyout pricing

- Collateral headroom. This may favour hedging the surplus, as less LDI exposure will be required (albeit a well-funded scheme will typically be running a relatively low level of leverage)

What to hedge?

In conclusion, schemes may want to consider how scheme surpluses could potentially be used and recognise the potential implications for their liability-hedging strategy – either to hedge their funding level or their surplus.

IMPORTANT INFORMATION

This document should not be taken as an invitation to deal in investments, a financial promotion or a marketing communication. The above information (the “Information”) has been produced by Legal & General Investment Management Limited and/or its affiliates (‘Legal & General’, ‘we’ or ‘us’).

No party shall have any right of action against Legal & General in relation to the accuracy or completeness of the Information, or any other written or oral information made available in connection with this Information. No part of this or any other document or presentation provided by us shall be deemed to constitute ‘proper advice’ for the purposes of the Pensions Act 1995 (as amended).

Limitations: The Information is not investment, legal, regulatory or tax advice. To the fullest extent permitted by law, we exclude all representations, warranties, conditions, undertakings and all other terms of any kind, implied by statute or common law, with respect to the Information including (without limitation) any representations as to the quality, suitability, accuracy or completeness of the Information. The Information is provided ‘as is’ and ‘as available’. To the fullest extent permitted by law, Legal & General accepts no liability to you or any other recipient of the Information for any loss, damage or cost arising from, or in connection with, any use or reliance on it. Without limiting the generality of the foregoing, Legal & General does not accept any liability for any indirect, special or consequential loss howsoever caused and on any theory or liability, whether in contract or tort (including negligence) or otherwise, even if Legal & General has been advised of the possibility of such loss.

Legal & General Investment Management Limited. Registered in England and Wales No. 02091894. Registered Office: One Coleman Street, London, EC2R 5AA. Authorised and regulated by the Financial Conduct Authority, No. 119272. Legal and General Assurance (Pensions Management) Limited. Registered in England and Wales No. 01006112. Registered Office: One Coleman Street, London, EC2R 5AA. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority, No. 202202.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.