Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Surplus in focus: What should DB schemes look out for?

The market backdrop for defined benefit (DB) pension schemes has fundamentally changed. Now the regulatory environment is changing too, with changes proposed to allow (where there is trustee-employer agreement) trapped surplus funds to be invested in the wider economy, potentially fuelling economic growth.

What has the government announced so far?

In January, the Prime Minister and Chancellor announced their intention to introduce greater flexibility for well-funded DB pension schemes to release surplus funds, with the Pension Regulator estimating that 75% of schemes are currently in surplus on a low dependency discount basis, worth £160 billion, or 49% of schemes on a buyout basis, worth £100 billion (as at 30 September 2024).

Three key elements of the government’s proposals include:

- Ease of access: Legislative changes to enable all DB schemes to change their scheme rules to permit surplus extraction, where there is trustee-employer agreement

- Striking a deal to extract: While there are unlikely to be requirements on what surplus is used for – e.g. the employer may choose to invest funds in their core business, and / or provide additional benefits to members of the pension scheme – trustees must consider how scheme members can best benefit from any agreement to extract surplus

- Safeguarding existing benefits: Trustees must fund the scheme and invest its assets in a way that leads to members receiving their full benefits

The government is expected to release further details of the surplus policy is its response to the Options for Defined Benefit schemes consultation, due this spring.

Why change and why now?

The proposals are designed to achieve two objectives: (1) boost UK economic growth and (2) improve saver outcomes, with the Chief Executive of the Pension Regulator commenting:

"Our first priority must be to ensure pension scheme members have the best chance of receiving their promised benefits. Where schemes are fully funded and there are protections in place for members, we support efforts to help trustees and employers consider how to safely release surplus if it can improve member benefits or unlock investment in the wider economy."

Practical considerations – what might trustees look out for?

While we wait to find out more about the practical details of how the government aims to make it easier to extract surplus, the key question remains how to set the extraction level, for example:

1. Intergenerational fairness – surplus now or safety later?

How should trustees balance (1) the opportunity to share available surplus with current members (via ad hoc payments or discretionary benefit increases) with (2) safeguarding existing benefits for future pensioners – set the extraction bar too high favours future payments but setting the bar too low may increase risk. We covered the trade-offs between the goals of benefit security and the level of regular surplus extraction in our earlier blog, Unlocking surplus in the endgame.

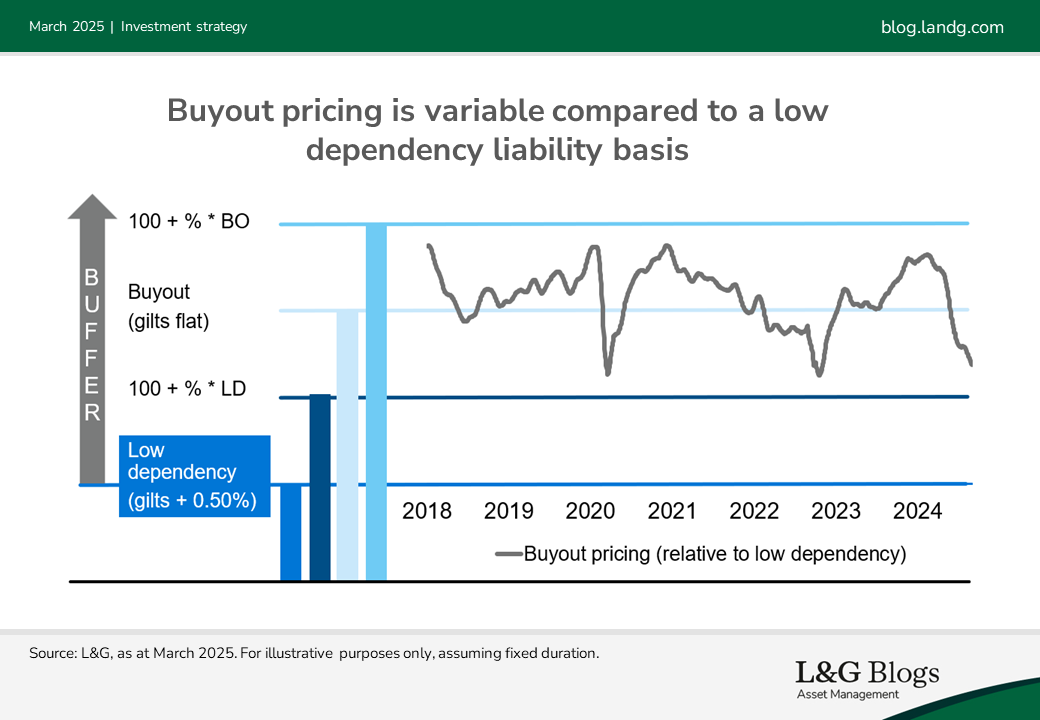

2. Variability of buyout pricing versus a low dependency basis

The DB funding code uses a low dependency basis (for example at a gilts + 0.50% discount rate) as its primary funding basis, with proposals in the consultation to consider surplus extraction at a buffer above low dependency.

For trustees allowing surplus to be extracted on an ongoing basis, the key risk is employer insolvency at the same time as being in a deficit on a buyout basis (after any recoveries from the sponsor’s insolvency).

Live buyout pricing will be variable over time based on changing market conditions (see chart below), so we believe a prudent approach may see trustees seeking to be funded to above a buyout basis (when considering the value of assets and the sponsor covenant) before allowing surplus extraction.

3. The rise of contingent assets

One way for trustees to balance the above issues and allow surplus extraction while preserving security, would be to set dual extraction criteria, for example:

- Scheme assets: above a low dependency funding level plus a buffer

- Total security (assets + sponsor covenant): above a prudent buyout funding level plus a buffer

Consequently, we may see renewed interests in the use of contingent assets such as parent guarantees, asset-backed security or bank-led credit enhancement.

Greater endgame flexibility on the horizon

Increased flexibility around the extraction of surplus will provide even more options for trustees and corporate sponsors as they consider their journeys to endgame, whether their objective is buyout, run-on or a combination of both.

If you’ve enjoyed this content, we’d like to highlight that you can find all our latest content for DB schemes in one place at our designated DB blog page.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.