Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Securitised products explained

With roots dating back to the 1970s, securitised products have evolved to such an extent that they have now become the second-largest sector in the US fixed-income market*.

The following is an extract from our Q1 Active Insights publication.

What are securitised products?

Securitised products are bonds backed by the cashflows from a dedicated pool of financial assets (for example, loans, leases and lines of credit). This is the key differentiating factor versus corporate debentures and sovereigns, which are general obligations of the sponsoring entity. Securitisation allows for both the financing of assets and the transfer of risk from lender to investor. Securitised bonds typically appeal to domestic banks, asset managers, insurance companies, hedge funds and overseas investors.

A large market

The market is large, diverse and mature, with a wide variety of income-producing assets being securitised. The combined outstanding balance of the overall securitised market, which stands at around US$13 trillion*, second only to the US Treasury market, can be segmented into mortgage-backed and non-mortgage-backed securities.

Mortgage-backed securities account for around 85% of the market* and include sectors such as agency single-family, non-agency single family and commercial real estate. In terms of annual issuance, mortgage-backed securities accounted for 75% of new issuance up to the third quarter of 2023*, while asset-backed securities (ABSs) and collateralised loan obligations (CLOs) comprised the remainder. The chart below gives a sense of the types of collateral that back securitised bonds.

Secured versus unsecured debt – potential investor benefits

We believe some of the potential benefits of securitised debt for investors may include:

Bankruptcy remoteness from the deal sponsor: Securitised bonds are created by transferring financeable assets to a special purpose vehicle (SPV) on a ‘true sale’ basis. To qualify as a true sale, the sponsor must surrender control of the assets, thereby isolating the respective trust from any potential bankruptcy risk of the sponsor. The trust then issues debt against the pool of assets, which is purchased by investors. If the sponsor of the SPV becomes insolvent, bankruptcy protection does not extend to any assets owned by the trust.

Diversification: Underlying collateral pools typically contain hundreds, or thousands, of assets that are diversified in many ways including by credit profile and geography. Diversification[1] tends to lower aggregate default rates and result in more predictable periodic and cumulative losses.

Credit protection: Securitised deals are typically structured with multiple classes spanning a wide range of credit ratings. Bonds at the top of the capital stack benefit from subordination, reducing the risk of principal loss. Moreover, the deals often include other diversified forms of credit enhancement, including overcollateralisation, reserve accounts and excess spread.

Range of weighted average lives: The deal structures distribute the underlying collateral cashflows to create bonds with a variety of weighted average lives (WALs) to fit investors’ needs. WALs range from a few months to more than 10 years in some cases.

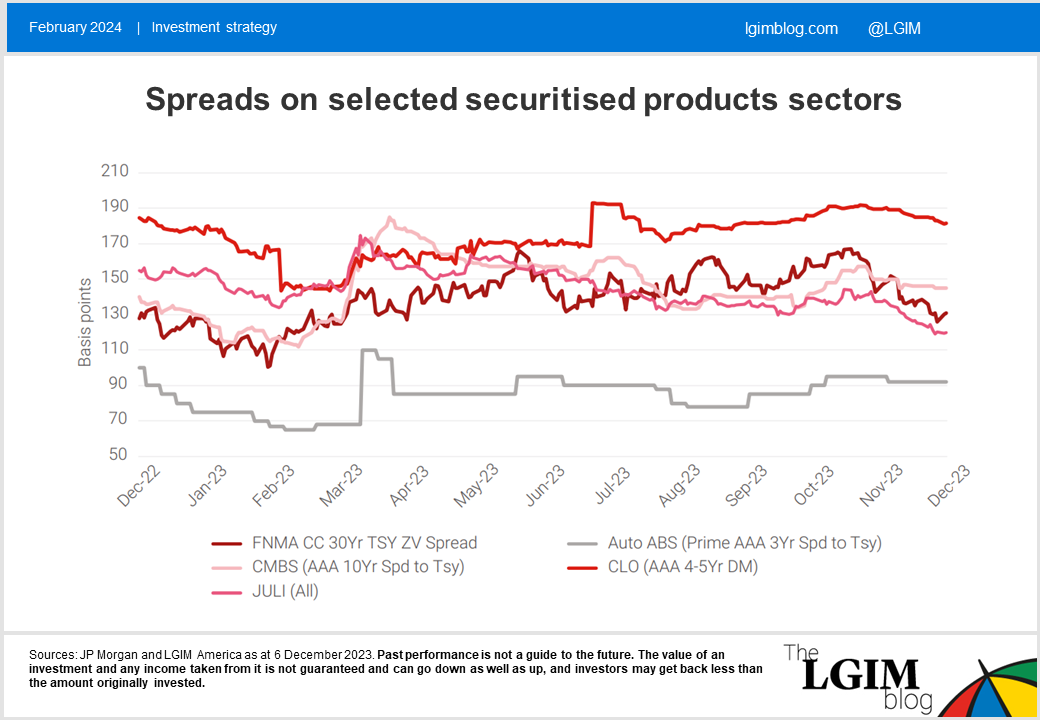

Spread pickups relative to competing sectors: The sector frequently offers a spread pickup versus competing unsecured debt. In the chart below we highlight generic sector spreads relative to investment-grade corporate spreads. Duration, liquidity, underlying credit characteristics and convexity are inputs that we believe could be considered as requirements for spread compensation.

Implications for investors

Securitised products can be much more complex than corporate debentures in terms of deal structures. Certain sectors of the market, notably single-family residential MBS, are characterised by volatile and path-dependent cashflows. Market participants rely on complex models to project interest-rate paths, cashflows and bond analytics.

There can also be a trade-off in terms of liquidity in the more esoteric corners of the securitised bond market. But, for investors willing to put in the effort to acquaint themselves with this asset class, we believe the sector can offer an attractive risk/reward profile and a potential diversification opportunity.

The above is an extract from our Q1 Active Insights publication.

*Source: BofA as at 30 September 2023.

[1] It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.