Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Rolling the dice on rebalancing: a hidden risk in momentum strategies

The timing of rebalancing can cause meaningful differences in momentum strategy performance. We model the effects of this phenomenon and suggest practical solutions for investors looking to avoid uncompensated risk.

When it comes to rules-based investing, attention tends to focus on signal construction – designing robust rules to define which stocks qualify as ‘winners’ or ‘losers’, particularly for momentum strategies. However, there is a subtler and often overlooked aspect of these strategies that can influence returns: the timing of rebalancing.

A typical systematic strategy is rebalanced periodically to ensure that holdings reflect the latest market information driving investment signals. For example, a stock that appears attractive based on past performance may no longer qualify just a few months later. Likewise, the predictive power of an investment signal can decay over time. Therefore, to maintain the effectiveness of a strategy, periodic rebalancing is necessary.

It’s easy to assume that systematic strategies are immune to calendar effects, given that the rules are fixed and the results are reproducible. Yet the choice of when to refresh the strategy can have a meaningful impact on performance.

A matter of timing

Rebalancing ‘timing luck’ refers to performance differences that arise purely from when the strategy is rebalanced, not from stock selection or portfolio design. Momentum strategies are rebalanced periodically, ranging from monthly to annually, to maintain target weights set by the investment signal and portfolio construction.

However, since markets don’t deliver returns in a smooth, linear fashion, the specific day or month a portfolio is rebalanced can have a material impact on which returns are captured, and which are missed.

Consider a strategy rebalanced just before a market rally: it may rotate out of stocks that go on to outperform. On the other hand, rebalancing just after a rally might result in stronger near-term performance due to better alignment with recent winners. This element of randomness introduces a form of performance ‘luck’ that can cause two otherwise identical strategies to behave differently, purely because of when they’re rebalanced.

Modelling the impact of rebalancing timing

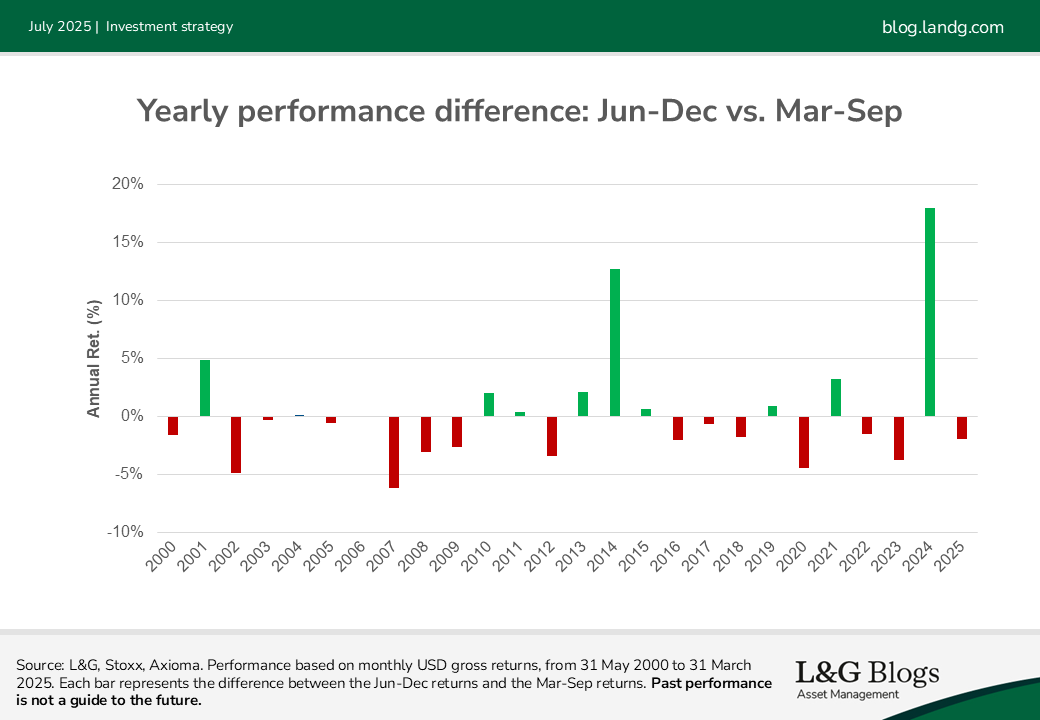

We constructed two momentum strategies that are rebalanced on a semi-annual basis. One rebalances on a March-September schedule, the other June-December. Both strategies are identically constructed by applying the same L&G momentum score tilt on the Stoxx World Global Large and Mid cap equity universe, subject to the same constraints and construction rules.

The only difference between the strategies is the timing of rebalancing. The chart below shows the difference in annual performance between the two.[1]

Over a 24-year backtest, the June-December variant outperformed the March-September version by an average of 23 basis points per annum. In some years, the return difference reached as high as 18%.

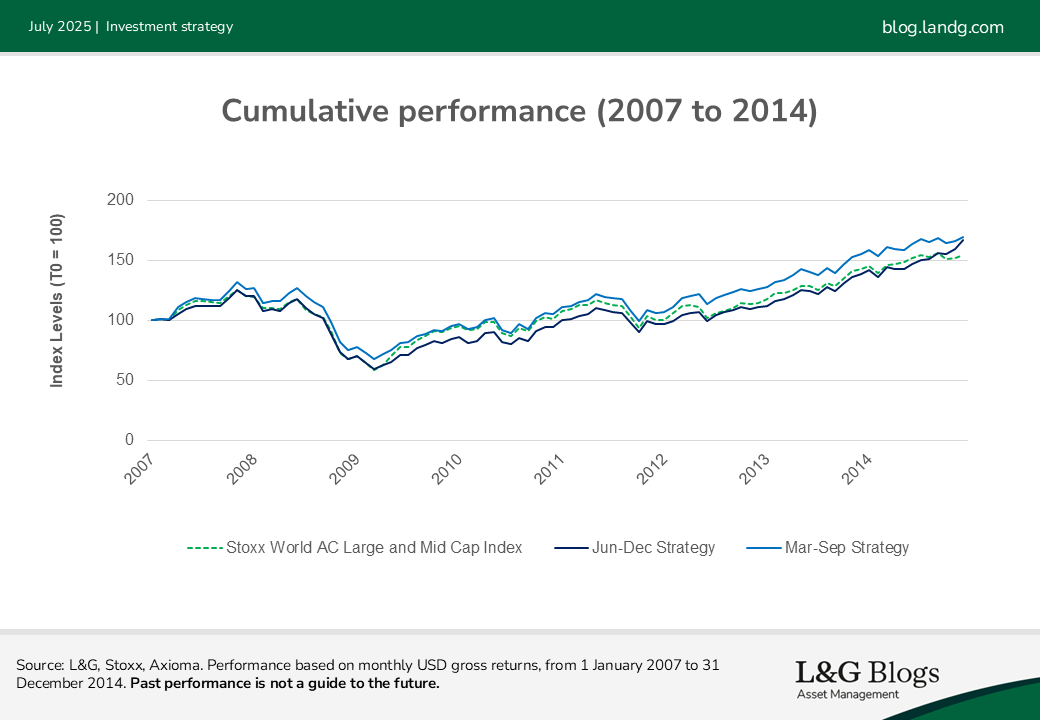

Timing-related differences can also persist over long periods. For example, between 2007 and 2015, the March-September strategy outperformed both its June-December counterpart and the market cap-weighted benchmark.

Therefore, an investor allocating to the March-September momentum strategy in 2007 would have outperformed the benchmark in the subsequent years, while the June-December equivalent would have underperformed over the same period.

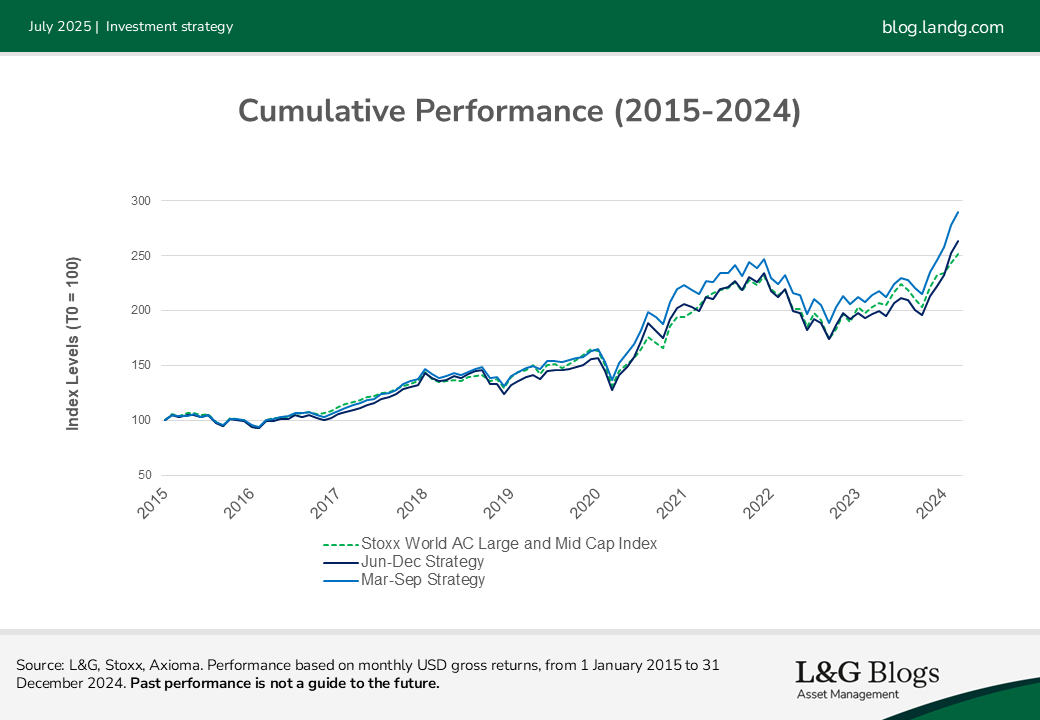

Similar performance gaps emerged between 2015 and 2024. These differences are not trivial. They reflect prolonged divergences between strategies that, on paper, follow the exact same rules.

Why does this matter?

For investors, the implications are significant. Timing luck introduces an uncompensated risk that’s especially relevant for strategies built on price-based signals like momentum. Two portfolios that follow identical rules can end up with materially different results just because they rebalance on different dates.

And unlike other forms of deviations, this difference does not necessarily mean-revert. The divergence can last for years, which complicates performance evaluation and can distort assessments of a manager’s skill.

Mitigating rebalancing timing luck

Since rebalancing is the point where timing luck enters a strategy, how and when you rebalance matters. One approach is to rebalance infrequently. Fewer rebalancing events mean fewer chances for poor timing to influence performance. The trade-off, however, is that the portfolio may hold outdated positions that no longer reflect current market information, drifting away from its intended exposures.

At the other extreme, rebalancing very frequently, even daily, can average out the luck effect. Just like flipping a fair coin many times brings you closer to an even split of heads and tails, frequent rebalancing can smooth out the randomness of any single rebalancing date. While effective in theory, in practice excessive turnover and trading costs will likely erode the strategy’s performance.

A more practical approach is to stagger the rebalancing while controlling turnover. Instead of refreshing the entire strategy at once, investors can divide the strategy ‘churn’ into multiple points across the year, say, on a quarterly basis. This avoids being overly exposed to any single rebalancing date, reducing the portfolio’s exposure to calendar-based fluctuations, or timing luck. Turnover constraints can be applied at each rebalance.

For example, rules can be set to restrict turnover to a maximum threshold, such as 30% per rebalance. This ensures that the portfolio gradually adjusts toward the new weights without excessive trading, helping to limit transaction costs while maintaining exposure to the signal.

Ultimately, timing luck can be mitigated either by reducing the number of times you roll the dice, or by averaging across many rolls to smooth out the randomness. The right approach will depend on trade-offs that investors are willing to accept between reactiveness and cost.

Conclusion

Rebalancing timing luck is a subtle force that can cause meaningful differences in strategy performance even when everything else remains the same. Its effects are real, can be long-lasting and often overlooked.

Strategies that rebalance on different schedules can produce noticeably different outcomes, sometimes for years. This matters for assessing backtests, manager comparisons and asset allocation decisions.

By understanding timing luck and applying thoughtful design techniques, like staggered rebalancing and turnover controls, investors can dampen its impact to overall performance.

Future work by the Index Solutions team will explore this subtle effect in other factors, such as Value, Quality and Low Volatility.

Past performance is not a guide to the future.

[1] The Jun-Dec portfolio is rebalanced every June and December of each year, while the Mar-Sep portfolio is rebalanced every March and September of each year.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.