Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Retirement Choices: Time to splash the cash?

With £100 billion in assets under management, Legal & General is the largest defined-contribution (DC) pension provider in the UK. We conducted a five-year study on our members’ retirement choices during the period 2015-2019.[1]

They say that “cash is king”. And while the average member taking cash at retirement may not be living like a king on their DC pension pot alone, it still feels good to finally get your hands on your savings.

In normal times, taking cash at retirement could pay for a well-earned cruise holiday, major renovations to your home, or a graduation present for the kids. But scheme members now approaching retirement worry that they lack investment confidence and knowledge – and the COVID-19 pandemic has only heightened their concerns. So, is the ‘cashing-out’ theme set to grow or will more savers opt to stay invested for longer?

Below, we look at the trends for taking cash over the last five years – and what to expect for the future.

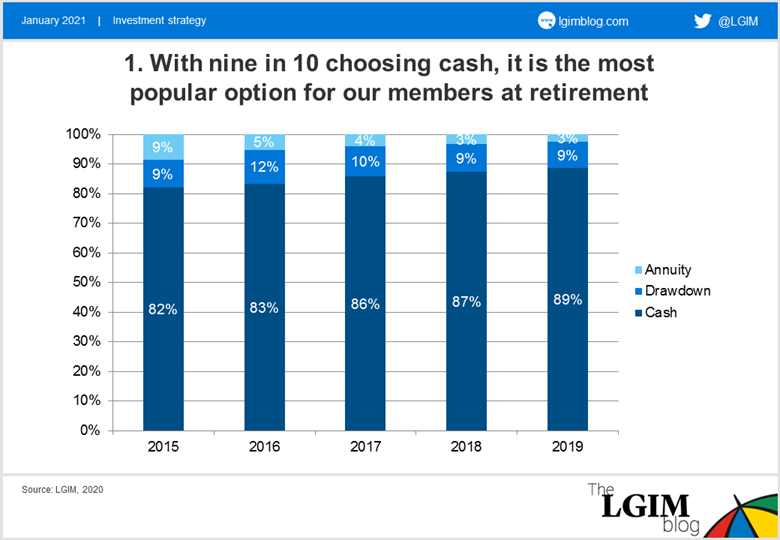

Taking cash has been a popular decision for many members of ‘Generation DB’ (defined benefit, now in their mid 50s and up). Nearly 90% of members retiring over the past five years have chosen to take their DC pot as cash, a proportion that has steadily grown since 2015.

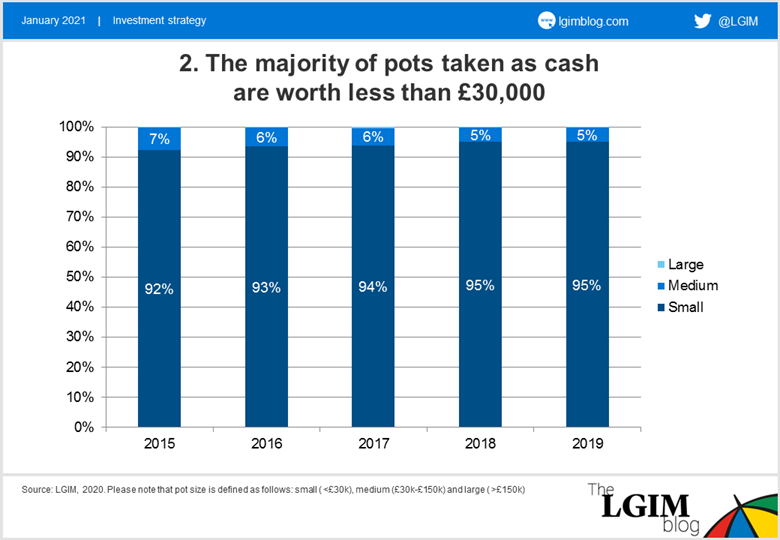

These retirees often had smaller DC pots which they used to complement other sources of income at retirement: the average pot size taken as cash is just £8,000, a number which has fallen over the last five years by about £2,000. As such, these retirees may have been in a better position than future retirement savers to treat their DC savings as a timely boost or a mid-life perk rather than a retirement-income lifeline.

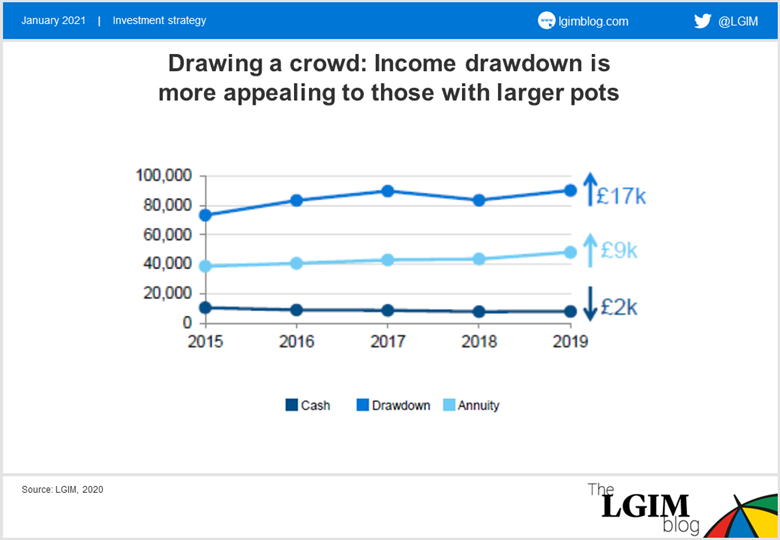

As you might expect, the proportion of those taking their pension as cash dramatically falls for members with pots greater than £150,000. Income drawdown is this group’s favourite option. This makes sense; it is only with a larger pot that a member can feasibly expect to draw a regular and sustained level of income to last the course of their retirement.[2]

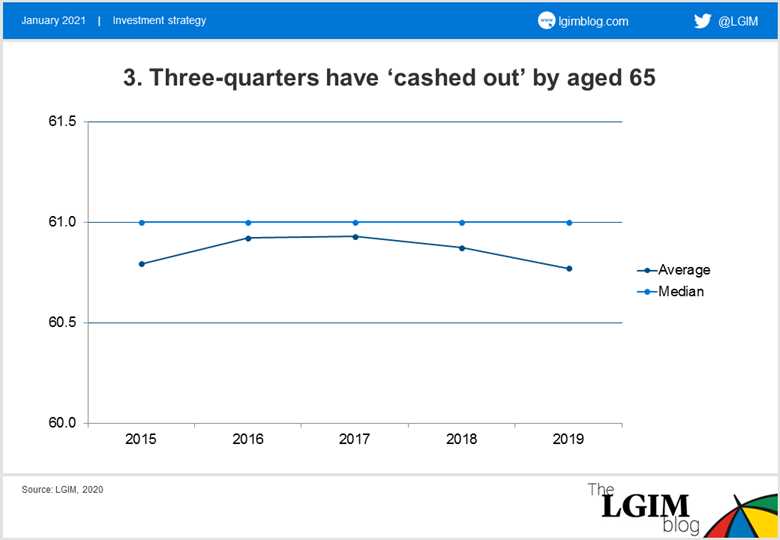

Taking cash has been a relatively young retiree’s game: something members do in the early years of retirement. The average age that members have taken their pot as cash has stayed fairly consistent at aged 61 over the last five years. In the past half-decade, roughly 40% of members chose to take cash before they reached 60, and about three-quarters opted to take their pot as cash before they hit 65.

Forging their own path

In the future, we’re not expecting any seismic shifts in the age at which members take cash. However, as the DC market develops further, we would expect to see average pot sizes increase and as a result cashing out at retirement may lose some of its appeal. We can already see that, to the relief of many trustees and regulators, as pots get larger, members are less likely to withdraw it all at retirement.

Instead, these members are plumping for drawdown or an annuity at retirement: options which saw average pot size increases of £17,000 and £9,000 respectively over the last five years.

In fact, we think that the percentage of members choosing cash is set to shrink in the years to come. And while many of those still taking cash are likely to access it for immediate use, leaving a pot sitting in cash, for however long, may not be the wisest decision over the long term. In retirement members are usually highly loss-averse and unlikely to tolerate significant fluctuations in their pot value well, so investing in equities isn’t the right answer either.

In this, the introduction of Investment Pathways and the associated regulatory steer from the Financial Conduct Authority is a welcome development, pushing providers to develop more sophisticated offerings for members that balance an additional return pickup relative to cash with managing downside risk.

[1] The number of members whose choices were reviewed in the study was 16,000 in 2015, 23,000 in 2016, 29,000 in 2017, 42,000 in 2018, and 53,000 in 2019 (rounded to the nearest thousand).

[2] Of course, choosing income drawdown does not mean a guaranteed income. If the member wants to ensure this throughout retirement, buying an annuity is really the only choice.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.