Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Q4 2025 Asset Allocation outlook: Calculated risks

Stay nimble, stay humble.

The following is the introduction to our Q4 2025 Asset Allocation outlook.

When writing these introductions, it can be useful to look back at the previous quarterly to take stock of what has changed.

Last time around, markets had just endured the biggest falls since the pandemic in the wake of April’s tariff announcements. In dynamic portfolios, we had added equity risk around the bottom, but this only took our overall risk asset position back to neutral as we maintained an underweight in credit.

Markets then had a sharp rebound when President Trump announced a pause in reciprocal tariffs. We were preparing to buy dips, believing that recession risks remain elevated, but the dips and recession have not materialised. As the rally continued we reduced our equity position to neutral shortly after the US trade deal with China, taking our overall risk asset position back to underweight. With hindsight, this move has proven premature. The rebound has morphed into a bull run with strong returns across virtually all asset classes year to date. But with our underweight entirely in credit and spreads already relatively tight, this defensive posture has not been too costly.

US remains on track to deliver growth

Despite the tariff uncertainty, global growth has been slightly stronger than expected in H1. Some of this growth reflects a front-running of tariffs and inventory build, so there is likely to be some payback heading into year-end as trade and industrial production slow. Nonetheless, consensus still expects 1-2% US growth in the second half of the year.

For the UK and the euro area, sluggish growth is projected. Growth is expected to pick up next year, though the risk is the UK gets left behind as fiscal policy is further tightened. China growth has recently disappointed with housing taking another leg down, but with some policy support the 5% growth target remains within reach.

Gauging the impact of tariffs

There remains uncertainty around US trade policy, which is exacerbated by legal challenges to tariffs. Reciprocal tariffs only went into effect in August, and sector-specifics tariffs are still not settled, so the full extent of tariff passthrough is still to be determined.

There is little evidence of foreigners cutting their export prices to the US. As tariffs work their way through US supply chains, US inflation should edge higher and squeeze real incomes in the months ahead. That impact is particularly pronounced at the bottom end of the income distribution, where some signs of credit distress are already emerging.

Following downward revisions to US employment, it seems that tariffs had a negative effect on business hiring decisions. Unemployment might stabilise as companies anticipate rate cuts from the US Federal Reserve (Fed) and some support from fiscal policy in 2026. However, the weakness in hiring now leaves the economy vulnerable to additional shocks, in our view.

Tackling the big questions: this quarter’s articles

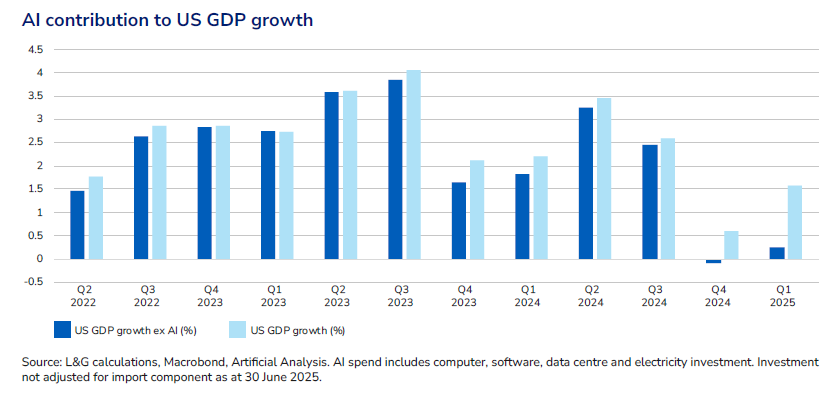

One of the main reasons the US has weathered the tariff shock is that surging AI investment spending across software, computer hardware and data centres has supported overall business investment, even as firms delayed spending in other areas. As shown below, stripping the effect of AI from US GDP growth would present a very different trajectory.

Looking ahead, a potential upside risk to growth next year is an AI-driven boost to productivity. This is a theme James Carrick, Senior Economist, explores in his article in this outlook. He focuses on the impact of AI on job opportunities for younger workers, and the investment opportunities that could be created.

Tim Drayson, our Head of Economics, zooms in on the other elephant in the room: the market reaction to the political drama surrounding the Fed. As Tim explains, a loss of Fed independence could have some counterintuitive ramifications, at least in the short term.

As longstanding assumptions about the Fed come into question, investors may do well to reconsider the rationale behind their core exposures. Chris Jeffery, our Head of Macro Strategy, tackles one such question in his piece, answering the question of why hold duration?

Finally, we offer an update on our long-term expected returns framework, which is now able to incorporate valuation mean reversion. This further builds out our valuations toolkit.

I hope you enjoy the articles my team has put together for Q4, and they provide you with useful insights for your client conversations.

Read our Q4 2025 Asset Allocation outlook.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.