Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Putting cash in its place: segmentation in a rising yield environment

Rising interest rates and inverted yield curves mean investors are looking to their cash allocations for more than the familiar stability and liquidity. But how should investors consider optimising returns?

Now is an interesting time to be a money market investor. That’s someone who makes short-term investments in securities that have been yielding close to zero (or less) for several years now. However, this year, that picture has started to shift.

In part one of this two-part series, we look at cash segmentation before discussing some of the options available to investors.

Rising rates, rising interest

It’s true that cash investors have had to contend with ultra-low interest rates for an extended period. However, now the tightening of monetary policy on the one hand, and inflationary pressure on the other, has made some investors reconsider the structure of their cash investments.

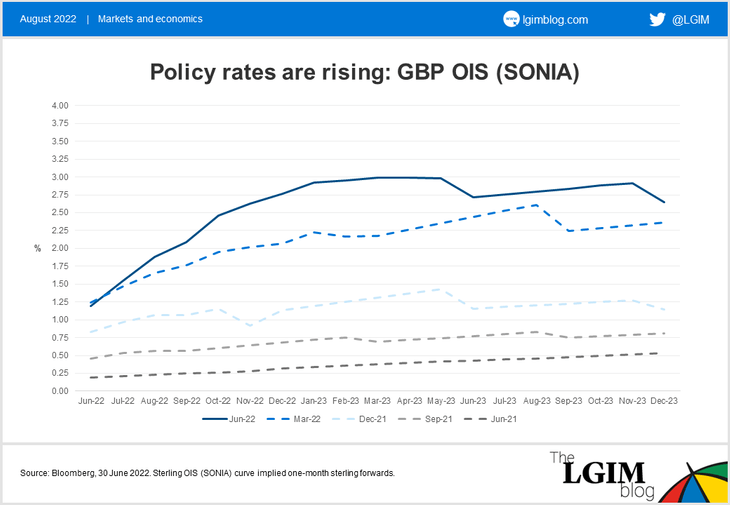

The path of policy rate increases, implied by overnight index swaps, has steepened significantly over the past year, prompting an increased focus on potential return for those investors who can stay the course over a slightly longer term. Of course, not everyone can remain invested, and cash requirements can be uncertain.

Peeling back the segments

Enter cash segmentation. Its objective is to optimise return within the context of an investor’s specific liquidity and capital stability requirements.

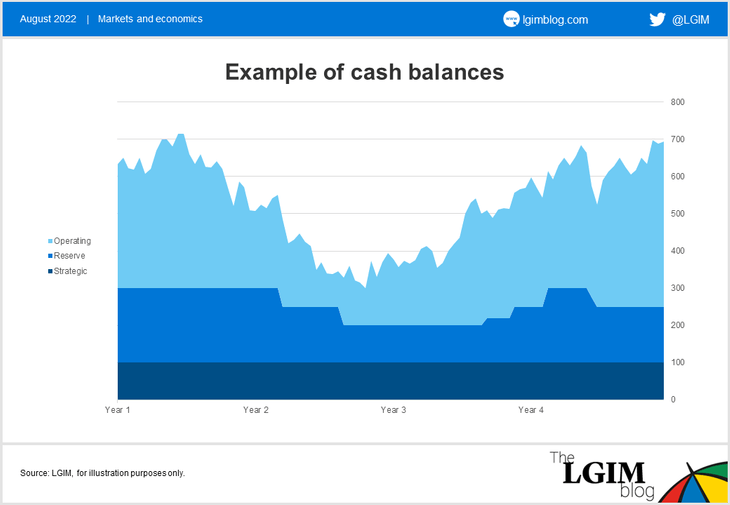

It’s important to consider those liquidity and capital stability needs first (accurate cash forecasting for treasurers, or optimal collateral buffers and payment schedules for pension schemes or insurers) to identify an allocation outside of day-to-day requirements. This can enable investors to segment their cash into ‘operational’, ‘reserve’ and ‘strategic’ buckets:

- Operating cash: requires same-day access for day-to-day needs and should be held somewhere that prioritises liquidity and capital stability ahead of yield

- Reserve cash: is not immediately required but could be called upon when necessary. A typical investment horizon would be six to 12 months

- Strategic cash: has a longer investment horizon, generally over 12 months, with some predictability over when cash will be required

These allocations can also change over time (as illustrated below) as reserve or strategic cash is drawn on to top-up operating cash balances and vice versa.

Finding the right balance

Good cash management is all about having the right amount, in the right place, and at the right time. As interest rates rise, many investors will be looking to capture additional returns. But it’s not just about returns – investors need to consider their time horizons, stability and liquidity needs first.

Now you’ve segmented your cash, what comes next? Part two of this blog will look at some options and important considerations to bear in mind for operating, reserve and strategic cash allocations.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.