Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Private Credit: Don’t be afraid of the doc!

In the second blog of this series focused on private credit market fundamentals, we use some horror-infused imagery to bring the concept of structural protections – those facets of private financings designed to protect creditors’ value – to life.

There are rules to surviving a horror movie. According to Scream, you should never say “I’ll be right back”. Generally, one probably shouldn’t investigate strange noises or separate from the group…and definitely avoid clowns. While all could be used as analogies, here I’d like to focus on Rule #22 of Zombieland: “When in doubt, know your way out”.

Private credit transactions are negotiated, crafted to balance the needs and preferences of both borrower and investor(s).

One of the core value drivers of investing in private markets is access to structural protections. These are the ‘quid pro quo’ for the conceptual illiquidity of unlisted investments, helping to minimise income interruption and preserve capital if things don’t go as expected.

Broadly speaking, private credit documentation looks and operates like a bank loan, and typically incorporates similar clauses to a borrower’s bank facilities.

Structural protections are an important tool for managing downside risk, providing investors with controls to manage asset credit quality by ensuring they do not significantly veer from pre-agreed parameters. Protections can result in greater early-stage influence and control, which may force pre-emptive borrower steps to de-risk the situation and increase recovery rates in the event of default.

We can place structural protections into three main categories:

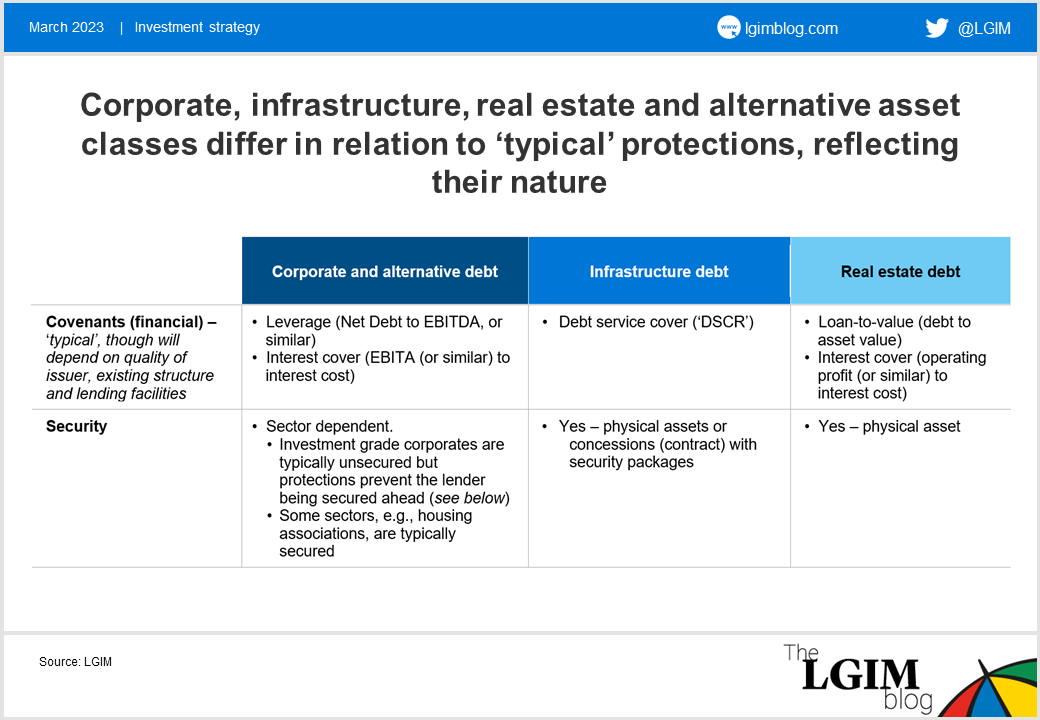

- Seniority – the priority of ranking in a capital and organisational structure i.e., what repayment priority do you have? While not dwelling on seniority herein, this is akin to where one stands in relation to the exit of the haunted house…

- Covenants – the documentary clauses that apply restrictions on the borrower – think of this as your ghost-detecting machine or garlic…

- Security – the claim or charge a lender has over a borrower’s assets, which can be physical (e.g., buildings) or other (e.g., contracted cashflows) – keeping a claim on Dracula’s castle?

Not-so-frightening covenants

Financial covenants create an effective cap on the amount of financial risk that management or a sponsor can put on the business, as well as better alignment of interest between long-term stakeholders.

Covenants and threshold levels should be set appropriately. These will vary depending on opportunity type and sector. For instance, food companies may be able to take on greater leverage than a retailer, without affecting their overall credit quality, due to less cyclical cash flows.

Monitoring of a borrower’s performance against covenants can give early warning signs of credit deterioration and promote engagement between borrowers and lenders. The ability to address problems quickly, potentially before wider market awareness, is a reason why recoveries in private credit transactions can be higher than comparable public bonds.

Non-financial covenants can be especially important. These can include controls on assets being pledged to other lenders and/or restriction on the debt a borrower can issue. These are designed to restrict both legal and structural subordination i.e., protecting against superior claims on certain assets and cash flows in insolvency. Preserving asset claim is not dissimilar to security-based protection – important in businesses where assets are not fixed.

Taking security seriously

The provision of security is a function of asset class, existing capital structure and borrower credit quality. It can be hugely valuable – a necessity, even – in various financings but is not, by itself, essential from the perspective of potential recovery.

In real estate debt financings, for example, lenders ensure primary access to the revenue-generating asset or asset pool that underpins the lending proposition. As such, these are secured. Conversely, high-quality corporate borrowers will often not provide security. Here, private credit investors will seek to rank at least pari passu (equal in right with payment) with other senior lenders (e.g., banks, bonds) and benefit from non-financial covenant protections.

Stick together

Private credit markets are ‘relationship’ markets – borrowers typically maintain regular lender dialogue. Coupled with the need for borrowers to report and measure financial and covenant performance, this provides lenders with context for more transparency and allows problems to be discussed, while actions can be taken before it affects credit quality.

Structural protections allow more informed investment decisions and can force corrective action before problems materialise. If things do deteriorate, a covenant breach opens dialogue and the opportunity to declare default.

Perhaps they’re not dissimilar to deciding not to walk through the cemetery at night or play with the Ouija board – eyes open, tools to keep things the way you expect and protection in case things go awry.

In my next blog I consider the asset classes in which we invest. ”I’ll be right back”…

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.