Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Price momentum: the curious case of market inertia

In the first instalment of a two-part blog, we examine the academic origins of price momentum, and its uneasy coexistence with the Efficient Market Hypothesis.

In 1687, Isaac Newton published the First Law of Motion, stating that an object in motion tends to stay in motion unless acted upon by an external force.

It would take more than three centuries for this principle to find its way into financial markets through the work of academics Jegadeesh and Titman. In their seminal 1993 paper Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency, they found that systematically buying securities with rising prices and selling those with falling prices can yield profitable returns over time, highlighting the tendency for past winners to continue winning and vice-versa.1 This phenomenon became known as ‘price momentum’.

By 1997, Carhart expanded on this research by integrating price momentum into the Fama-French factor model, solidifying momentum's place in both academic theory and practical investing.2 Today, momentum is a widely recognised strategy within factor-based investing and the broader investment community.

The momentum premium puzzle

Despite its extensive history, the existence of the momentum factor remains somewhat puzzling.

One reason is that it contradicts the Efficient Market Hypothesis, which posits that all known information is reflected in today’s price and therefore indicating that past performance cannot predict future returns.3 Momentum, however, suggests positive historical returns could indicate a future positive trend in the short term, and vice versa. The idea that past performance could be predictive of future performance fundamentally challenged the notion that financial markets are efficient (i.e. prices reflect all available information).

There have been various attempts to explain the momentum effect. Some have attributed the effect to herding behaviour, where investors tend to follow the crowd as opposed to their own judgements. Others suggest that investors underreact to news, with the initial underreaction causing a gradual price adjustment over time and creating upward pressure as prices continue to move in the direction of the initial news.4

Another perspective involves the market’s microstructure, where investors’ tendencies to ‘cut losses and let profitable trades run’ lead them to sell underperforming securities while buying more of those that have outperformed. This subsequently adds to the buying pressure on winners and vice-versa for the losers.

Types of momentum

There are generally two categories of momentum investment practices: time series (or absolute, trend-following) momentum and cross-sectional (or relative) momentum.

Time series momentum is more popular among commodity trading advisors (CTAs) and involves assessing a security’s past returns independently, buying those that have performed positively and selling those that have performed negatively. Cross-sectional momentum ranks past performance across a universe of securities relative to each other, overweighting those that rank high while underweighting those that rank low.

In the context of index investing, cross-sectional momentum has typically been favoured for its diversified nature, relatively low tracking error and credible academic foundations.5

How does it perform?

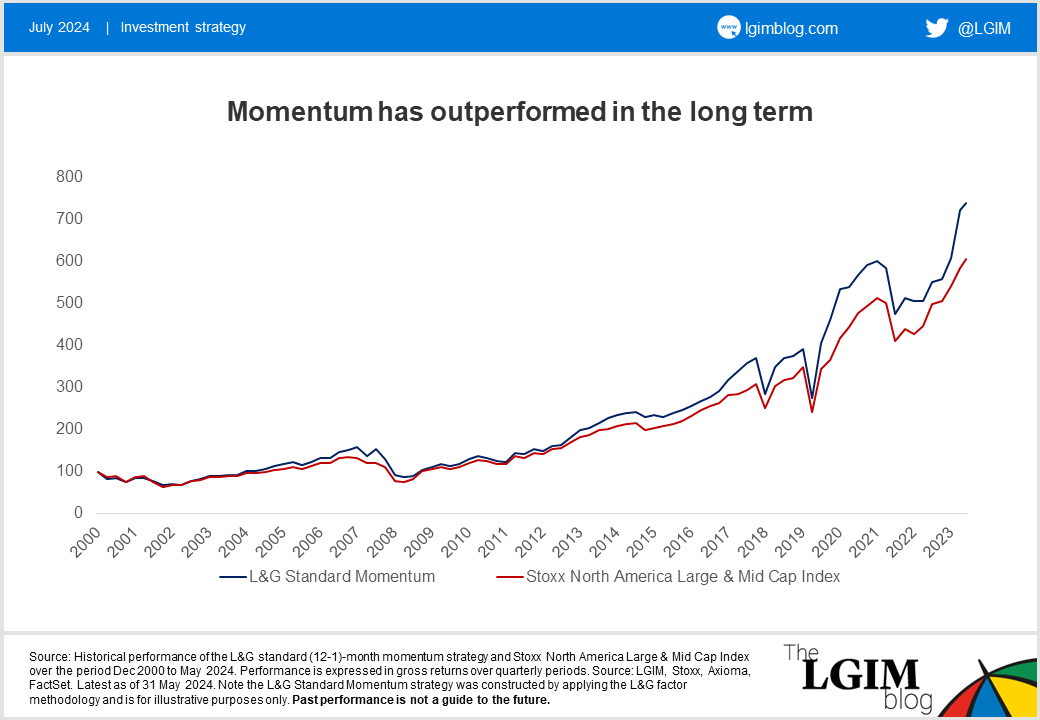

The chart below illustrates the performance of a standard (12-1) month cross-sectional momentum strategy applied to the Stoxx North America Large & Mid Cap Index. This strategy involves scoring each stock in the index on the basis of its historical returns over the past 12 months, skipping the most recent month, and then adjusting their original market exposure to favour those with higher scores, while reducing exposure to those with lower scores. The scores were generated using our proprietary L&G Multi-Factor Scoring Framework.

Over the 23-year period shown below, the L&G Standard Momentum strategy6 has shown an outperformance of around 93 basis points per annum compared with the market cap index, highlighting momentum’s historical effectiveness as a robust investment strategy.

Empirical evidence has shown that the standard (12-1)-month momentum strategy has consistently delivered strong performance over time, indicating that buying winners and selling losers can be rewarding. It’s important to note that this analysis was done on historical data, which of course means it isn’t guaranteed to repeat in the future.

The effectiveness of momentum relies on the tendency of past winners to keep winning and likewise for past losers to keep losing. This, by definition, also means that the strategy can falter during market reversals, when past losers outperform past winners.

In the second part of this blog, we’ll examine some techniques that aim to improve the risk-adjusted returns of momentum strategies, as well as considering other ways of quantifying momentum.

Sources:

1. JEGADEESH, N. and TITMAN, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), pp.65–91. doi:https://doi.org/10.1111/j.1540-6261.1993.tb04702.x.

2. Carhart, M.M. (1997). On Persistence in Mutual Fund Performance. The Journal of Finance, 52(1), p.57. doi:https://doi.org/10.2307/2329556.

3. Fama, E. (1970) Efficient Capital Market: A Review of Theory and Empirical Work. Journal of Finance, 25, 382-417.

4. Zaher F. Index Fund Management: A practical guide to smart beta, factor investing, and Risk Premia. Basingstoke: Palgrave Macmillan; 2020.

5. ibid.

6. Note the L&G standard momentum strategy was constructed by applying the L&G factor methodology and is for illustrative purposes only.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.