Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Navigating a tight credit spread environment: Seeking safety in short duration

We believe that short-duration bonds could potentially provide a buffer against market volatility while offering flexibility to transition to long-duration credit when conditions improve.

The current environment of tight credit spreads presents significant challenges for investors, particularly defined benefit (DB) pension funds.

For schemes looking to de-risk or re-deploy proceeds from maturing illiquid investments, we believe one effective strategy could be to reinvest in short-duration investment-grade credit. This approach captures the carry (i.e. the additional yield over government bonds) while maintaining flexibility to adapt to market conditions and transition to long-duration credit when spreads widen.

What can investors do when credit spreads are tight?

The short answer: invest in shorter-duration credit, which has historically tended to outperform during spread-widening events – thereby minimising potential future mark-to-market losses – with the intention of switching into long-duration credit when pricing is more favourable.

The details: shorter-duration credit tends to be more sheltered than longer-duration maturities. The lower credit spread duration[1] of short-duration bonds means they are inherently less sensitive to spread-widening events, providing a potential safe harbour. When assessing the relative excess return potential versus gilts, short-duration bonds have historically typically exhibited lower volatility and less severe drawdowns, making them an potentially attractive and defensive allocation in this credit environment in our view.

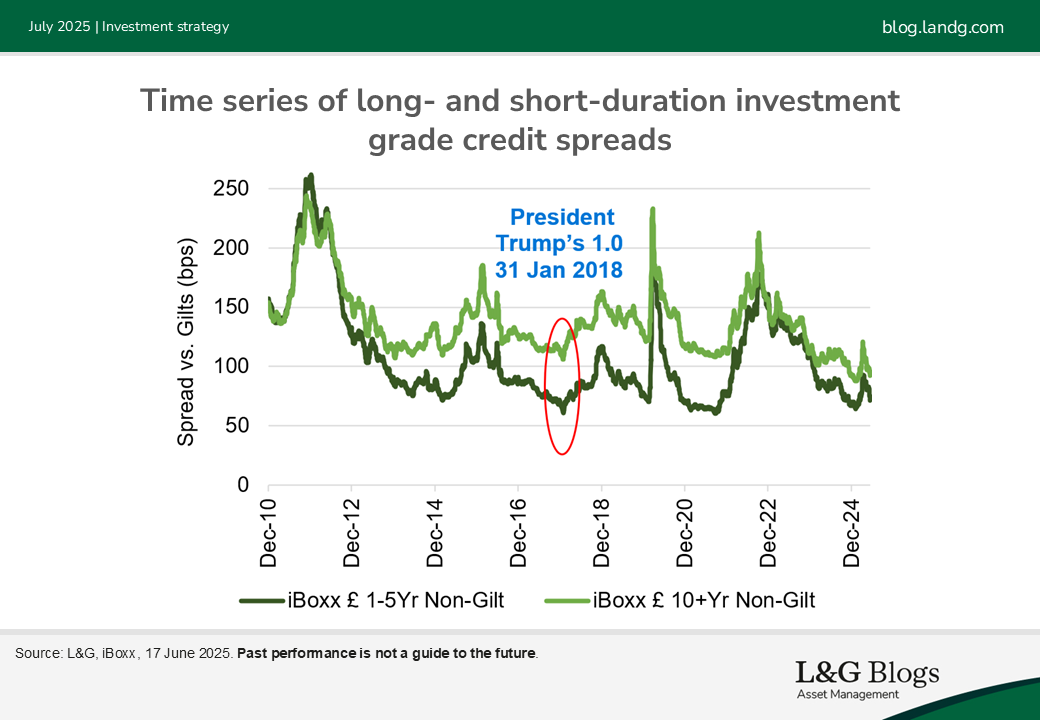

This can be illustrated by examining a period during President Trump's first term. As Mark Twain is often quoted, “History doesn’t repeat itself, but it does rhyme.” On 31 January 2018, credit spreads were relatively tight (see chart below). However, they began to widen for several reasons, including escalating trade tensions between the US and China, and rate rises in the US. This episode bears similarities to current market conditions, where again geopolitical tensions and restrictive monetary policy are in effect.

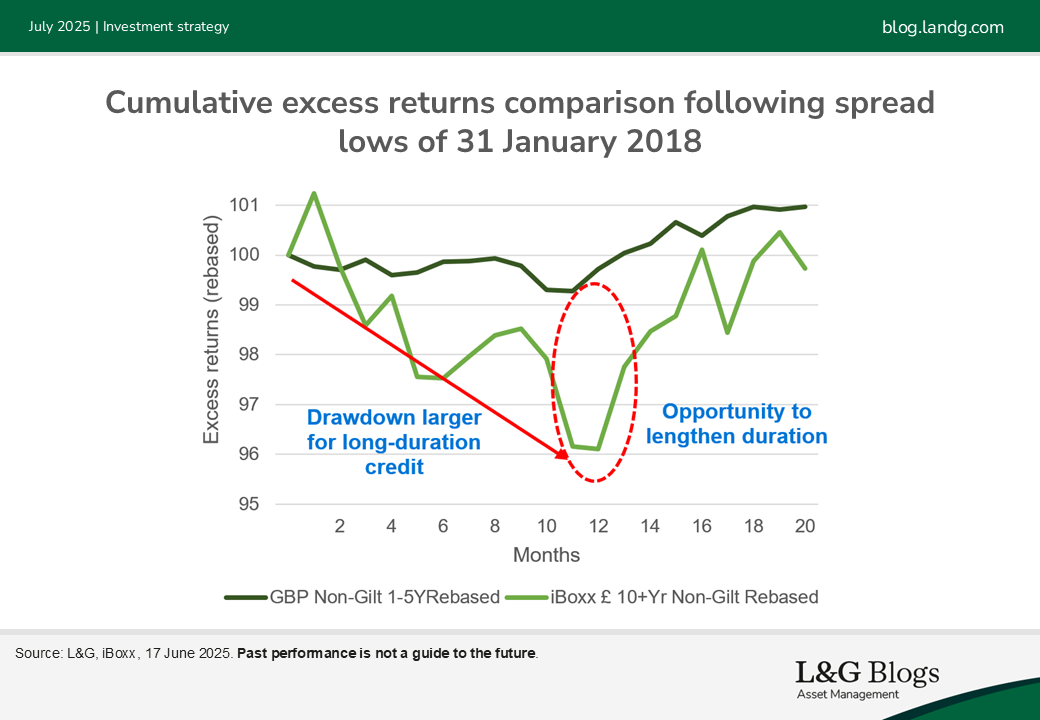

If we then compare excess returns over gilts for the credit indices in the second chart, we see that shorter-duration credit tended to outperform the longer-duration index in this spread-widening event over the course of the 20 months post January 2018.

We believe this presents a potentially compelling opportunity. Investors seeking to gain credit market exposure or capture carry can do so with short-duration credit. This strategy could potentially help them to reduce mark-to-market capital losses as spreads widen. Nimble investors, equipped with pre-defined trigger mechanisms, could then transition from short- to long-duration bonds to lock in a potentially more attractive credit spread premium for a longer investment time horizon.

When considering this strategy, it is important to keep several factors in mind. The term premium for credit typically results in an upward-sloping spread curve, meaning short-duration bonds often trade with a tighter credit spread than longer-duration bonds. This ‘carry deficit’ needs to be assessed by investors against the potential benefits of waiting to capture wider spreads.

Transaction costs associated with moving from short-duration to long-duration bonds also need to be factored into decision-making. Transaction costs can erode the benefits of the strategy, although note that transaction costs for trading in and out of short-duration credit are lower than that of longer duration credit, owing to the typically lower mark-to-market volatility of these bonds and therefore lower risk for market makers who need to be compensated for warehousing positions in these bonds.

This also means that the costs associated with a short-duration credit investment may be quickly recovered by the additional carry earned versus gilts. A final consideration is that this strategy is inherently taking more re-investment risk. If credit spreads mean revert to wider levels, then that re-investment risk will be positively rewarded, but there is the risk that credit spreads remain at tight levels for a long period or even go tighter.

What could cause current spreads to widen?

Credit markets today are pricing in a benign, forward-looking environment, with issuer credit fundamentals remaining strong. Technological innovations, particularly in AI, promise increased productivity and efficiency, potentially boosting GDP. We are also keeping a watchful eye on sectors and issuers that could be negatively impacted.

Additionally, tax cuts in the US and fiscal expansion in Europe, led by Germany, offer the prospect of further GDP growth, complemented by the positive wealth effect of higher stock valuations.

However, these positive factors must be balanced against significant challenges. The market is grappling with various geopolitical risks, notably the restructuring of the global trading system resulting from tariff uncertainly. Exorbitantly high government deficits, rising debt-to-GDP ratios, and steepening government yield curves lurk in the background, threatening to disrupt markets and crowd out private investment.

Think long term

In this context, where credit spreads are tight, we believe that adopting a ‘prepare, don't predict’ investment strategy is particularly prudent. Predicting market movements can be fraught with uncertainty, but preparation allows investors to build resilient portfolios that can weather various scenarios. Understanding that spreads tend to mean revert over time, investors can position themselves to benefit from the eventual widening.

We believe that by focusing on high-quality issuers, maintaining diversification[2], and taking a long-term perspective, investors can seek to mitigate risks associated with tight(er) credit spreads by tilting to shorter-duration credit in the current tight spread environment.

The current landscape of persistently tight credit spreads is challenging. Tactically focusing on short-duration corporate bonds can not only provide a potential buffer against market volatility but ca also offer the flexibility to transition to long-duration credit when conditions become more favourable.

By maintaining a nimble and adaptive strategy, we believe investors can navigate the complexities of the credit market, leveraging short-duration credit as a potential safe harbour while positioning themselves to capitalise on future opportunities.

[1] Spread duration refers to the sensitivity of a bond’s price to a 1% change in its credit spread.

[2] It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.