Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

L&G explains: How primary and secondary markets seek to provide ETF liquidity

We lift the bonnet on ETF trading to explain how a dual-market system can ensure price alignment and track underlying assets.

Exchange traded funds (ETFs) have revolutionised investing by offering potential liquidity, diversification* and cost efficiency. Unlike traditional mutual funds, ETFs trade on an exchange like individual stocks, allowing investors to buy and sell shares throughout the trading day. Behind this seamless trading experience lies a unique market structure consisting of a primary and secondary market.

The secondary market is where most investors interact with ETFs. Here, buyers and sellers trade ETF shares on an exchange, helping to provide liquidity and determine market prices. But what happens when demand for an ETF exceeds what’s available in the secondary market? This is where the primary market comes into play – a less visible but crucial mechanism that helps ensure the ETF maintains its intended value and tracking efficiency.

Understanding the mechanism behind ETF transactions can help investors optimise their trades, assess liquidity and avoid hidden costs.

ETF market structure: primary versus secondary market

ETFs operate within a two-tiered market structure. The secondary market (on-exchange and off-exchange) is where most investors interact with ETFs, buying and selling shares on stock exchanges or through institutional trading venues or bilaterally.

The primary market (creation and redemption mechanism) comes into effect when demand exceeds supply in the secondary market. Authorised participants (APs) step in to create or redeem ETF shares, ensuring price alignment with the net asset value (NAV).

The secondary market: on-exchange trading

On-exchange trading refers to buying or selling ETFs through a regulated stock exchange, like stocks. Investors place orders via an online trading platform or brokerage, and the trade is executed at the best available price in the open market. Transactions are routed through an exchange. Market makers and liquidity providers naturally help to support the liquidity of the ETF.

Trading via an exchange offers several advantages in our view, including potential liquidity, transparency, regulated execution and easy access for both retail and institutional investors. The bid/ask spreads of ETFs can impact execution prices, and the liquidity of the underlying assets is something that needs to be considered, especially in less liquid ETFs where large orders may influence the price.

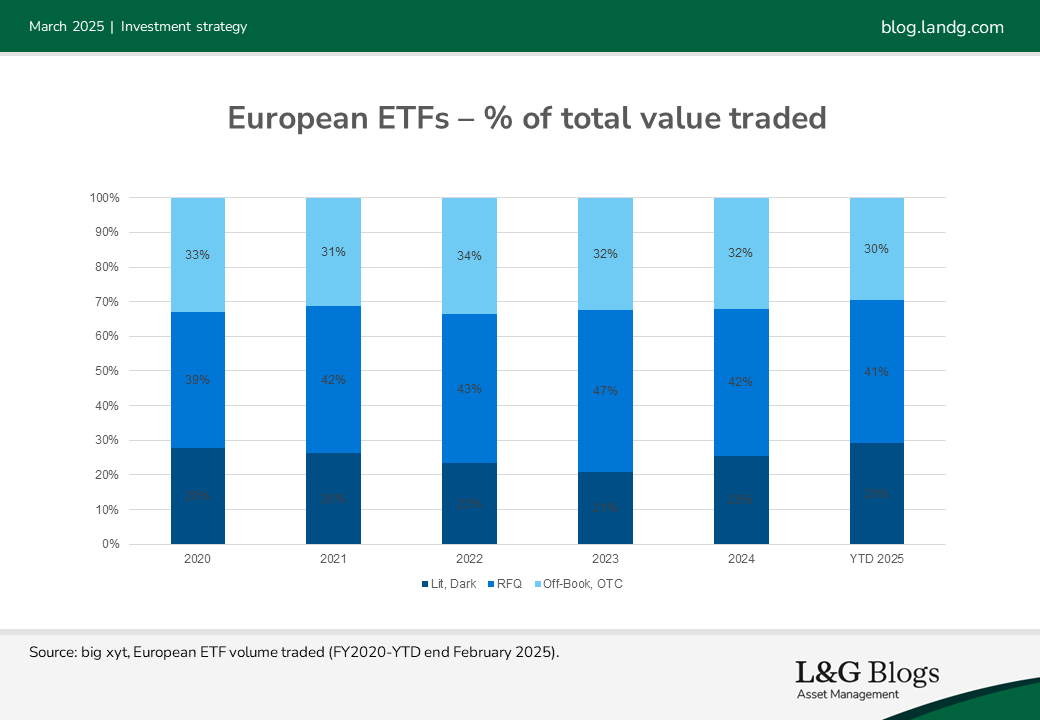

Generally, in Europe, on-exchange volumes represent around 20-25% of the total volume traded, with the remaining 75-70% trading off-exchange. This varies depending on the product and region. There are several reasons for this . First, the European market is much more fragmented in terms of the number of exchanges, depositaries and currencies than the US.

Additionally, the level of retail participation in EU capital markets remains low compared with other advanced economies. In 2021, approximately 17% of EU household assets are held in financial securities, well below the amount held by US households.[1]

European ETFs are largely the domain of institutional investors, who tend to trade off-exchange in blocks via independent venues such as Tradeweb and Bloomberg.[2]

The secondary market: off-exchange trading

Off-exchange ETF trading includes transactions conducted outside public exchanges, typically through over-the-counter (OTC) trades other regulated venues (i.e. MTFs), dark pools or bilaterally. These methods are primarily used by institutional investors, as retail investors generally do not have direct access to off-exchange liquidity.

Key execution methods used in off-exchange ETF trading include:

- Multilateral trading facilities (MTFs) are regulated electronic trading venues primarily used for matching large buy and sell orders. They are not regulated in the same way as exchanges but offer improved price discovery and enhanced liquidity. A central order book provides real-time pricing, resulting in transparent price discovery. Unlike bilateral OTC trades, MTFs allow interaction with various liquidity providers. However, to trade via MTFs, investors must establish trading lines with execution brokers, enabling them to respond to requests and execute ETF orders efficiently.

- Bilateral trading facilities: Investors may also access ETF liquidity bilaterally by engaging directly with a liquidity provider. Prices and trade terms are privately negotiated between the two parties, making it a common practice for large block trades. This can help clients to minimise market impact and maintain discretion over their trading activity.

The primary market

In addition to the secondary market, ETFs have an additional layer of potential liquidity. In situations where the secondary market fails to absorb demand/supply, APs can create (or redeem) new (or existing) shares in the primary market. Only APs can create and redeem ETF shares.

This mechanism helping to ensure ETFs trade efficiently and remain closely aligned with their underlying assets. The ability of APs to arbitrage price differences between an ETF and its underlying assets helps to prevent significant deviations between the ETF’s price and its NAV.

If an ETF trades at a significant premium or discount, Aps can intervene by creating or redeeming shares, bringing prices back in line. Investors who understand the role of APs can recognise when an ETF’s price has deviated from NAV and avoid overpaying. This is particularly important during periods of market stress, when ETF prices may briefly diverge from their NAV.

The interaction between the primary and secondary markets is crucial for ETF efficiency. Even if an ETF has low trading volume in the secondary market, its liquidity is not solely determined by that volume. Thanks to the primary market, new ETF shares can be created as needed, helping to ensure that liquidity is tied to the liquidity of the underlying assets rather than just the ETF’s trading volume.

Sources:

[1] Questions and answers on the Retail Investment Package

[2] Is RFQ dominance of European ETFs set to stay?

*It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.