Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Is ‘timing the market’ applicable for private markets?

In this blog post, we look at whether short-term volatility can create an attractive entry point for private market investments, despite the long-term nature of these assets.

Investor interest in private markets has grown consistently over recent years. These assets are generally held over the long term (often in closed-ended funds) and are mostly more illiquid than public market assets.

Despite their long-term nature, private markets are still impacted by short-term market volatility. For example, since interest rates started to rise in 2022, real estate and venture capital valuations have weakened. Private equity activities stagnated, significantly reducing distributions back to investors which has constrained the ability to make new allocations. The current conditions have led investors to review whether they should continue allocating to private markets. It has therefore led us to review the impact of market timing in private markets and address the question ‘is now a good time’?

Tough markets can create attractive entry points

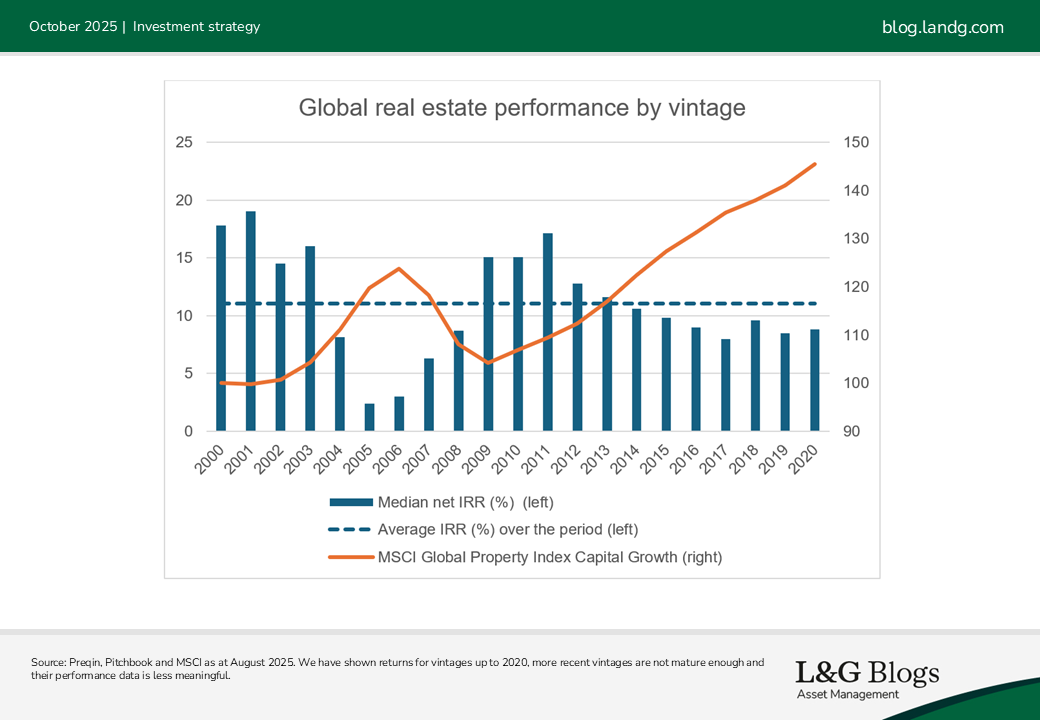

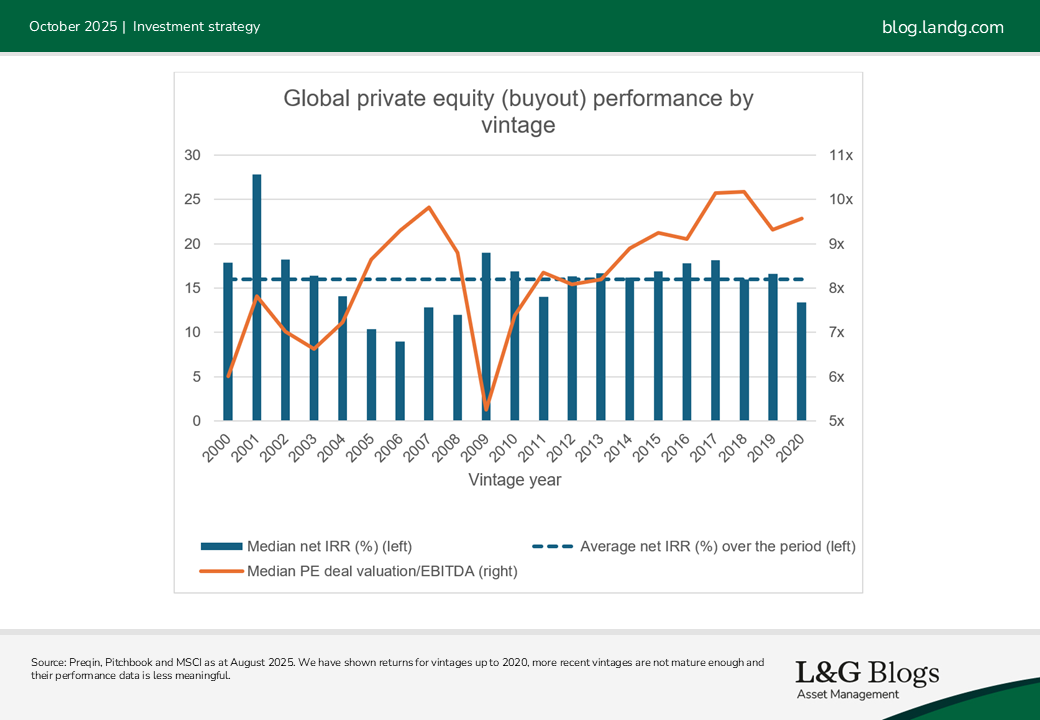

We looked back to data since the Global Financial Crisis (GFC) (the last major crisis) to see how timing affected private market performance. Using closed-end fund data from Preqin, we found that real estate and private equity vintages in the immediate aftermath of the GFC significantly outperformed preceding vintages.

The main driver was entry pricing – real estate and private equity valuations fell significantly during the GFC. Funds that invested in the down years were subsequently rewarded as the market went on a long bull run from 2010.

Income is a valuable buffer

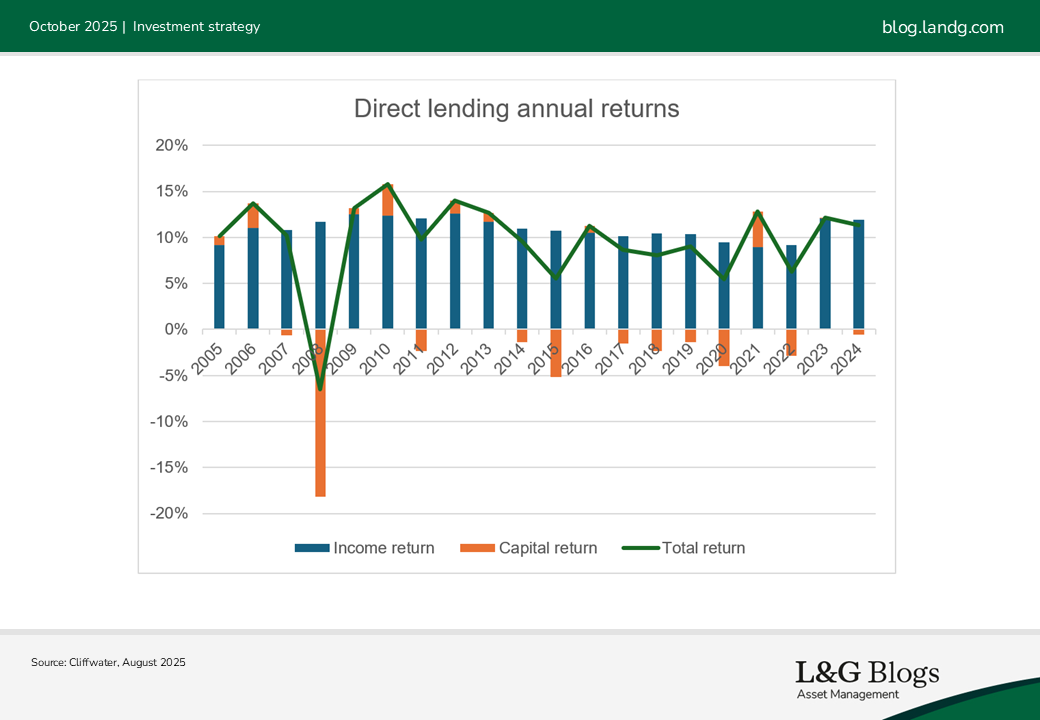

What about private credit and infrastructure, asset classes typically deriving a greater proportion of returns from income?

Historical data show a much more stable performance profile through market cycles. Using direct lending (a sub-set of private credit) as an example, it consistently generated annual income returns of around 10%. This mitigated against valuation volatility which can be largely driven by changes in credit risk (direct lending is floating rate and therefore not exposed to interest rate risk).

Buy well, operate well, exit well

Back to the question at the start of this blog: is now a good time to invest in private markets?

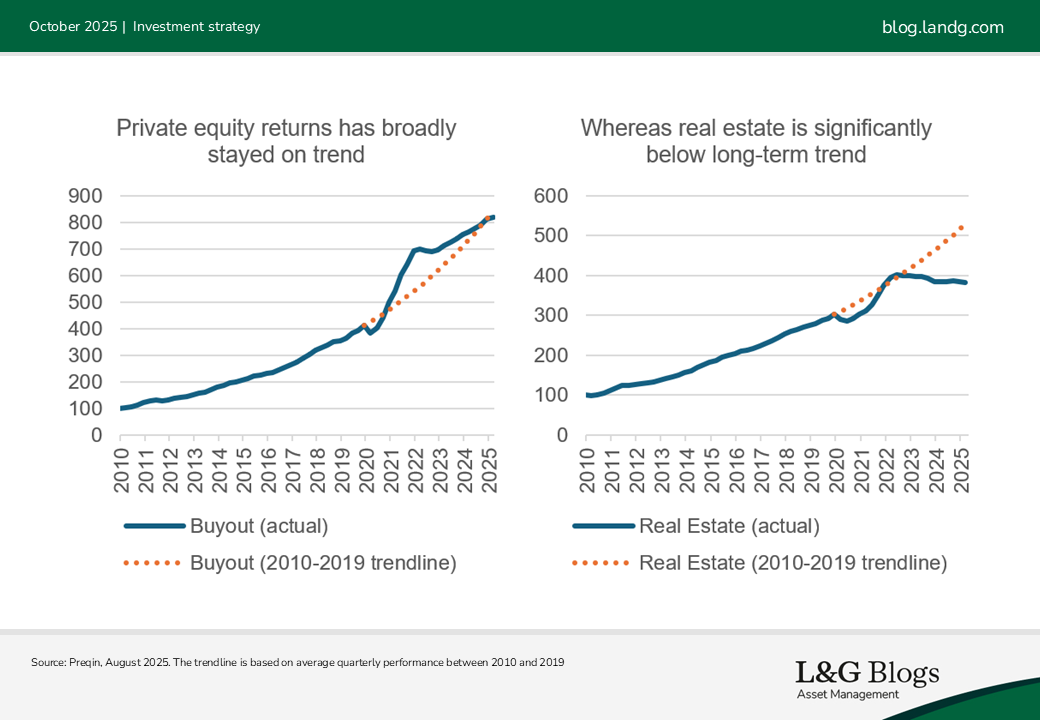

We showed earlier that “buying the dip” and accelerating deployment during market dislocations has worked historically. This underpins our more positive view on real estate and investment-grade private credit, where current yields are notably higher than long-term average. Private equity and infrastructure are currently less generous with valuations towards the expensive end of the 10-year range. We are particularly concerned about the lack of correction in private equity and emphasise the importance of pricing discipline in today’s environment.

However, this does not mean we oppose allocating to parts of the market that have not severely repriced. Academic research has shown that earnings growth can outweigh purchase price as a driver of long-term private markets performance. Higher-growth assets are also likely to exit better with demand more immune to macroeconomic volatility. For example, this is reflected in our UK real estate sectoral views. We like logistics and residential - trends in e-commerce, deglobalisation and demographics are expected to sustain strong long-term return in these sectors. The structural headwinds facing offices and retail makes us less convictional despite more attractive valuations.

As Warren Buffett famously said: “It is far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” We believe good returns can still be generated in ‘less generously’ priced parts of private markets. The key to success is manager skill – making the right sector calls, sourcing high-quality assets, operating them well and exiting successfully.

Invest through the cycle

Private market investing requires a long-term approach. We prefer to invest through the cycle, adopting a well-diversified strategic asset allocation.

We also know that private markets are not fully efficient and seek opportunities to add exposure to attractive sectors/strategies supported by structural tailwinds when there is price dislocation. Developments in private markets mean we can access a broad toolkit, including secondaries, evergreen funds and co-investments.

Past performance is not a guide to the future.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.