Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

How pension proposals could power sterling assets

We assess the extent to which UK government plans might boost investment into private market assets and bolster economic activity.

The following is an excerpt from our midyear global outlook.

As global investors rebalance their geographical exposures, sterling assets may gain on the margin. But we believe the long-term trajectory of the UK economy will ultimately prove a far more potent factor in their performance.

To this end, how might the UK government’s plans for pensions boost the country’s growth? The Pension Schemes Bill 2025 released in June is aimed at building scale in the industry by encouraging various forms of consolidation. It also seeks to stimulate UK investment, in the expectation that larger pools of capital will be more easily able to invest in longer-term private market assets.

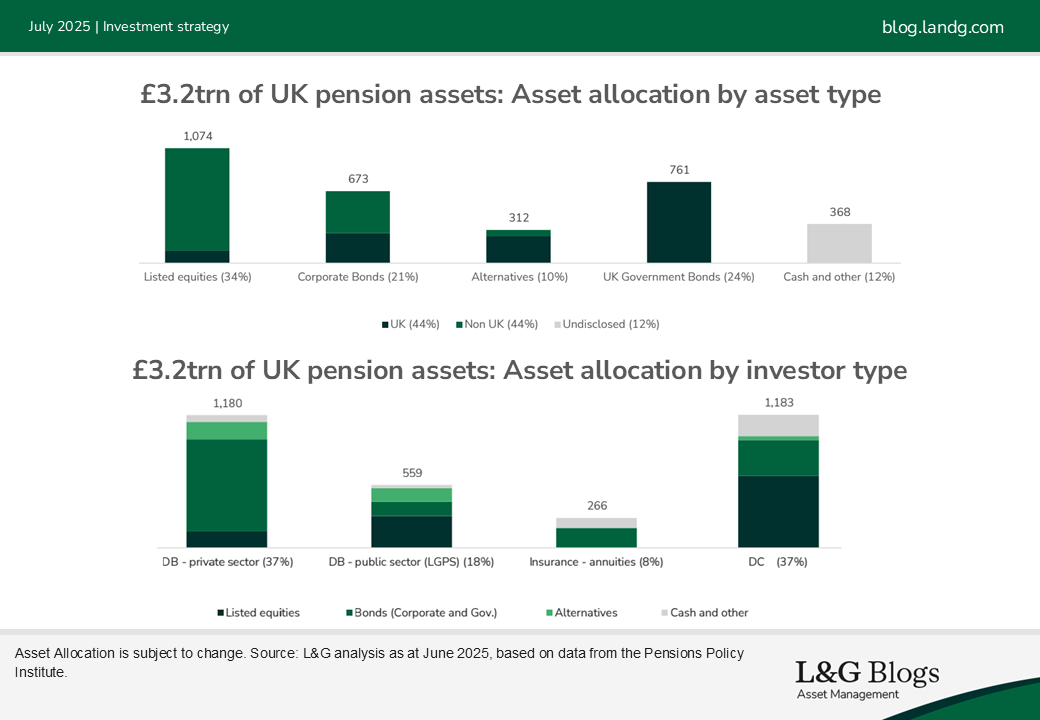

Of the estimated £3.2 trillion of UK pension assets (as at September 2024), some 44% are already invested in sterling assets, predominately UK Government bonds. Only about 10% are invested in alternatives (property, private equity, private credit and infrastructure), albeit with an already high 80% allocation to the UK.[1]

In order to increase the overall allocation to private markets (i.e. the Alternatives category in the charts), the bill proposes:

DB – private sector: making it easier for trustees of well-funded Defined Benefit pension schemes to release money back to employers and their scheme members, when safe to do so, unlocking some of the £160 billion surplus funds to be reinvested across the UK economy and boost business productivity and deliver for members.[2] There is the potential for some of this surplus to be invested for growth in private markets.

DB – public sector: consolidating and further professionalising the Local Government Pension Scheme (LGPS), with assets held in six pools that can invest in local areas infrastructure, housing and clean energy. There is the potential for the existing allocation of larger LGPS schemes to private markets to be taken up more broadly by the larger pools.

DC: new rules creating multi-employer DC scheme ‘megafunds’ of at least £25 billion, so that bigger and better pension schemes can drive down costs and invest in a wider range of assets. Together with the voluntary Mansion House Accord (to invest 10 percent of their workplace portfolios in assets that boost the economy such as infrastructure, property and private equity by 2030, at least 5 percent ringfenced for the UK) this has the potential to increase private market allocation within DC.

Insurance – annuities: insurance companies are already investors in private market assets to back their insurance liabilities, albeit with a focus on cashflow generating assets. This is set to continue as well funded private sector DB schemes select buyout as their endgame strategy and will increase as Solvency UK and consultation on the Matching Adjustment Investment Accelerator seeks to expand the range of assets that insurers can invest in.

We wait to see how this legislation will change the current asset allocation across these investor types. Each will have different risk, return, liquidity and regulatory objectives and, importantly, different expected growth rates.

However, what is clear is that the government’s intention is to increase interest in UK private market assets across the entire domestic pensions market, thereby also catalysing economic growth, by setting policy and through defining framework in legislation.

It is up to the market to take up this call to action – both in terms of demand for UK private market opportunities, but also in supply, to kickstart growth in the government’s plan for change.

For investors more generally, this growing focus on UK private market assets may present an opportunity to invest, albeit amid with some risk of being crowded out if demand outpaces supply.

DC deep-dive

As the global economic landscape evolves, UK pension schemes – particularly DC funds – face both opportunities and challenges in navigating their sterling-denominated assets. While UK DC pension schemes traditionally relied on public markets, DC investing is evolving beyond a singular focus on low fees, shifting toward value-driven funds and defaults that prioritise long-term outcomes for savers.

Historically, private markets were kept at the margins of DC investing – deemed too complex, too illiquid. But these asset classes offer the potential for enhanced long-term returns through exposure to high-growth assets and sectors, including venture capital, infrastructure, clean power and affordable homes.

As noted elsewhere in this report, the current push towards private assets can provide further diversification, seeking to mitigate volatility linked to global financial cycles.

In July 2024, L&G was one of the first asset managers to launch a private markets strategy range designed for UK pensions and DC savers. By incorporating private markets, our funds seek potential enhanced returns through high-growth assets. Our approach strikes a balance between global opportunity and a UK focus – offering strong market access and creating a differentiated engagement opportunity for DC savers.

Our new DC and multi-asset approaches enabled us to be one of 17 UK asset managers to sign the updated Mansion House Accord,[3] cited earlier. Further pension reform, such as the Pensions Investment Review, encourages greater allocation to private markets.

We see sterling assets as a potential beneficiary given expected inflows from the wider DC market, which is poised to play a more significant role in financing UK-led projects. As this policy shift not only aims to enhance retirement outcomes, but strengthen domestic investment capacity, bolstering the UK economy. As UK assets are influenced by macroeconomic forces – global inflationary pressures, central bank policies, and geopolitical uncertainties, the priority remains clear though: looking to help safeguard DC savers while aiming to secure sustainable, long-term growth.

We believe that by keeping the focus on what is best for our members, UK pensions can navigate uncertainty to help future-proof retirement outcomes, while supporting domestic investment in critical projects.

Real estate reallocation?

We have seen anecdotal evidence of US investors considering capital allocations outside their domestic market. So far, however, this has been contained within a few surveys or ‘shows of hands’ at industry conferences.

Any reallocation would most likely, in our view, focus on continental Europe as well as the UK – but UK real estate values were marked down significantly in 2022 and 2023. At a market level, despite some recent value appreciation, valuations remain -21% lower than their recent peak. This is slightly more than the US and significantly more than Europe ex UK, where values were lower by a more modest -14%[4]. The UK offers investors scale and transparency. It is the third-largest institutional real estate market globally and the second-largest developed market after the US. It is the largest market in Europe[5]. According to JLL, it remains the most transparent real estate market in the world – offering strong legal protections, robust data availability, and high liquidity.

Putting UK real estate in a broader private markets context shows that real estate yields, based on a spread to risk-free, are screening relatively strongly – a reflection of the fact that real estate globally has repriced more quickly than private equity and infrastructure.

Based on independent forecasts, a market-weighted sector average of ‘prime’ real estate in the UK is expected to outperform global averages with an average annualised return of 7.5% p.a. to 2029[6]. Part of this is supported by structural shortages of supply in many real estate segments following a period of significant construction price increases. This, and continuing friction in achieving planning permission, is supporting rental tension in areas of the market with resilient demand such as multi-let industrials, many parts of the residential market and high-quality offices.

In a global context, the case for UK commercial real estate is not about turning away from the US; we see it as about building resilience and enhancing returns through diversification. With elevated yields, a favourable policy backdrop, and strong sector-specific opportunities, the UK offers a timely and tactical complement to US exposure.

This article is an excerpt from our midyear global outlook.

[1] Source: 20250604-pension-scheme-assets-2025-final.pdf

[2] Source: Government response: Options for Defined Benefit schemes - GOV.UK as at May 2025.

[3] As at May 2025.

[4] MSCI quarterly data to Q1 2025

[5] MSCI valuation data, end 2024.

[6] Property Market Analysis (PMA), spring forecasts 2025.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.