Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

How can platform investing be deployed to meet wider portfolio objectives?

In our first blog on operational real estate, we looked at how growth equity investing can be applied to this asset class. In our second instalment we’ll compare this style of investing to a value-add/opportunistic real estate strategy.

Growth equity vs value-add and opportunistic real estate: Return drivers

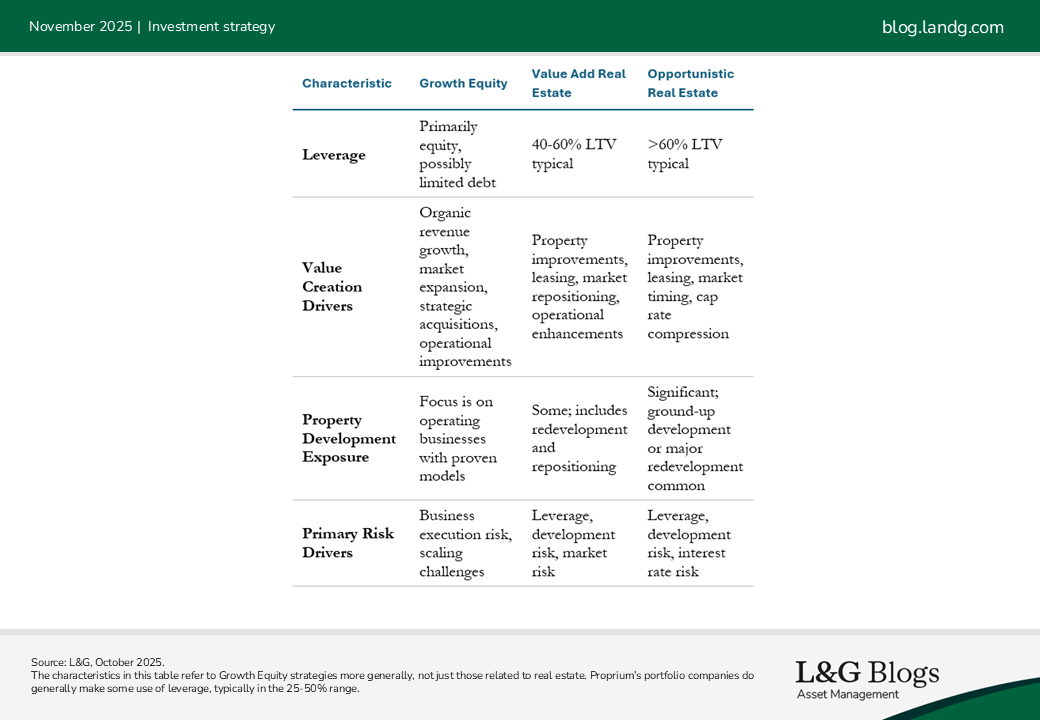

Growth equity and value-add/opportunistic real estate investing share a common thread: Both target outsized returns by embracing higher risk and active value creation.

Their risk-return drivers, however, fundamentally differ. Growth equity investing in real estate operating platforms carries risks tied to execution. Success depends on scaling operations, delivering growing net operating income (NOI) or earnings before interest, tax, depreciation and amoritisation (EBITDA), achieving revenue targets, and navigating sector-specific dynamics.

In contrast, value-add/opportunistic investing is more exposed to asset-level volatility, capital expenditure risk, and market timing. Returns may hinge on cap rate compression, leasing success, and renovation outcomes. Crucially, active asset management is often stapled to significant use of financial leverage.

A question of correlation

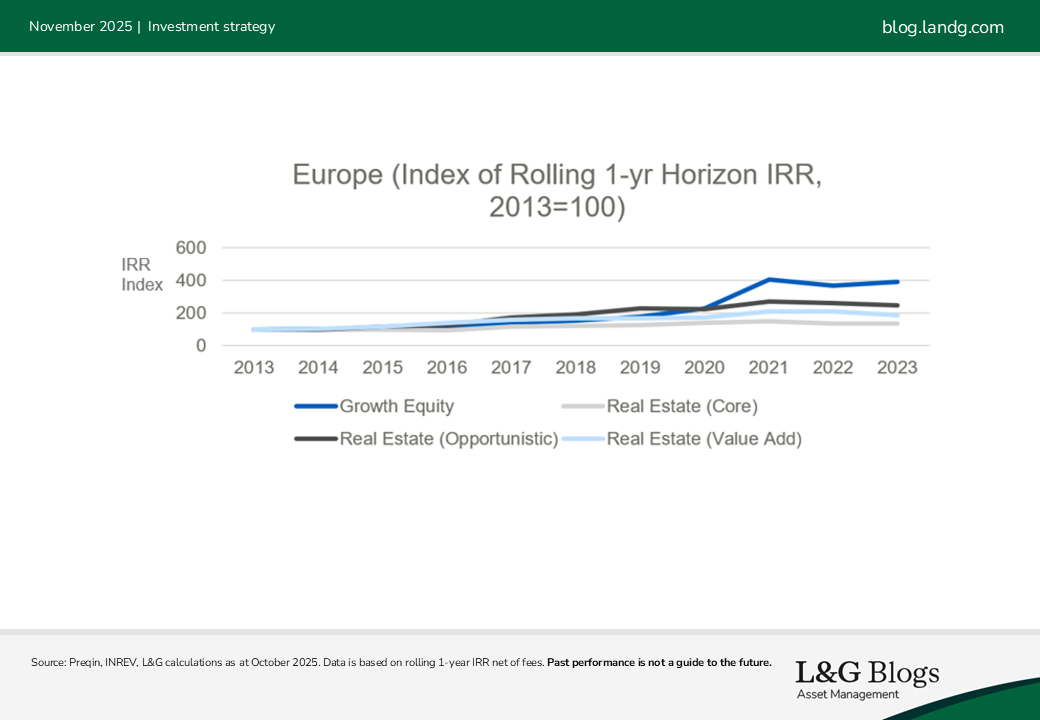

Consequently, we see growth equity returns, even when applied to real estate operating platforms, as only modestly correlated to the real estate valuation cycle. While there isn’t a deep pool of data to fall back on here, we do have several reference points to build a picture.

Preqin data for Europe covering the 10-year period to end-2023 confirm a relatively low correlation between overall growth equity returns to those of core real estate (0.43) as well as a significantly higher return, averaging 15%. In contrast, opportunistic real estate delivered a lower return and showed a higher correlation with the real estate cycle.

In our view, this supports both the return enhancement and diversification benefits of specialist platform investment in the context of a wider real estate allocation, enhancing the contribution of real estate to the overall balance of risk & reward at the total plan level.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts will come to pass. Past performance is not a guide to the future. It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.